The average auto body insurance claim now costs $4,818 — and getting there is far more complicated than most insurance companies let on. Between adjusters, repair estimates, hidden damage, supplement requests, parts disputes, and your legal rights as a policyholder, the auto body insurance claim process has more moving parts than most car owners expect.

Most drivers go through this fewer than three times in their lives. Insurance companies and body shops handle it every day. That information gap costs car owners money — through underpaid claims, unauthorized aftermarket parts, and rights they never knew they had.

This guide covers the entire auto body insurance claim process from accident scene to repaired vehicle. It explains what to document, how coverage types work, how to choose a body shop, what happens when hidden damage turns up, and how to dispute a low estimate. It also covers the consumer rights that insurers rarely volunteer — including the right to choose any repair facility, the right to OEM parts in many states, and the right to file a diminished value claim after repair.

Insurance processes and consumer rights vary by state. Consult your specific policy and your state's Department of Insurance for details applicable to your situation.

Step 1: Document the damage before anything else

Before calling the insurance company or contacting any body shop, thorough documentation protects the car owner's interests throughout the entire claims process. This step is the foundation everything else builds on — and it costs nothing but a few extra minutes at the scene.

What to photograph at the scene

Take photographs of all visible damage from multiple angles. Include wide shots showing the overall vehicle, medium shots of each damaged area, and close-ups of specific damage points. Photograph the other vehicle or object involved, the surrounding area including road conditions and signage, and any visible injuries.

One step most car owners skip: photograph the undamaged areas of the vehicle before the claims process begins. This establishes a pre-accident baseline and protects against disputes over which damage is pre-existing.

What information to exchange

From any other drivers involved, collect:

- Full name, address, and phone number

- Driver's license number and state

- License plate number

- Insurance company name and policy number

- Vehicle make, model, year, and VIN

Note the date, exact time, and precise location of the incident, weather and road conditions, and the names and badge numbers of any responding police officers.

Why a police report matters

For any collision involving another vehicle, a police report creates an official record that insurance companies rely on throughout the claims process. In a fault dispute, the police report carries real weight. Even for minor collisions where police don't respond to the scene, filing a report online or at the local precinct within 24 to 48 hours is advisable.

Step 2: Know your coverage before filing an auto body insurance claim

Not all auto insurance coverage works the same way, and the type of coverage that applies determines how the claim process unfolds — including who pays the deductible, who you file with, and what rights apply.

Collision vs. comprehensive coverage: which applies

Collision coverage pays for damage to the insured vehicle from a collision with another vehicle or object, regardless of fault. If you were at fault in the accident, collision coverage is typically what applies.

Comprehensive coverage pays for damage from non-collision causes: hail, flooding, falling objects, fire, theft, and vandalism. Hail damage claims, for example, always fall under comprehensive coverage.

Both coverage types are subject to a deductible — the amount you pay out of pocket before the insurance company pays the remainder.

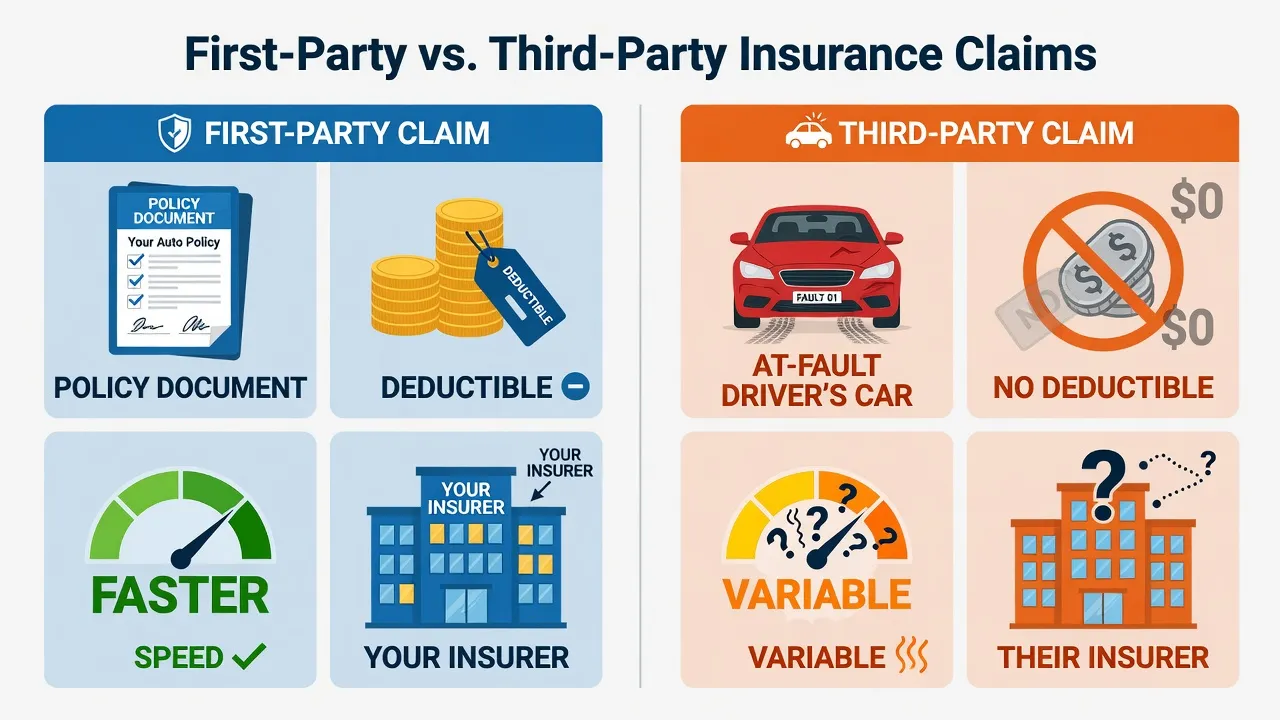

First-party vs. third-party claims: who do you file with?

This distinction is one of the most important decisions post-accident, yet one of the least explained by insurers.

A first-party claim means filing with your own insurance company, regardless of who caused the accident. Your insurer handles the claim and, if another party was at fault, may pursue them for reimbursement through subrogation.

A third-party claim means filing directly with the at-fault driver's insurance company when you weren't at fault. Their insurer handles the claim.

| Factor | First-Party Claim | Third-Party Claim |

|---|---|---|

| Filed with | Your own insurer | At-fault driver's insurer |

| Deductible | You pay your deductible | No deductible required |

| Processing speed | Typically faster — insurer knows your history | Can be slower — their insurer has no duty to you |

| Control level | Higher — your insurer has contractual obligation to you | Lower — their insurer's obligation is to their policyholder |

| Diminished value eligibility | Harder to claim (first-party) | Clearer path (third-party) |

| Premium impact | May affect future premiums | Does not affect your premiums |

For more detail on the tradeoffs between these two paths, see our guide to first-party vs. third-party insurance claims.

What a deductible means and who you pay it to

According to CCC Crash Course 2026 data, 26% of insured drivers now carry deductibles of $1,000 or more — up 3.5 percentage points year-over-year. Knowing when and how to pay the deductible prevents confusion when the repair is done.

The deductible is paid to the body shop, not to the insurance company. When the repair is complete, you pay the body shop the deductible amount; the insurance company pays the shop the remainder of the approved repair cost directly.

If you weren't at fault and filed a third-party claim with the at-fault driver's insurer, no deductible should be required. If the at-fault insurer asks for one, that's a red flag worth questioning.

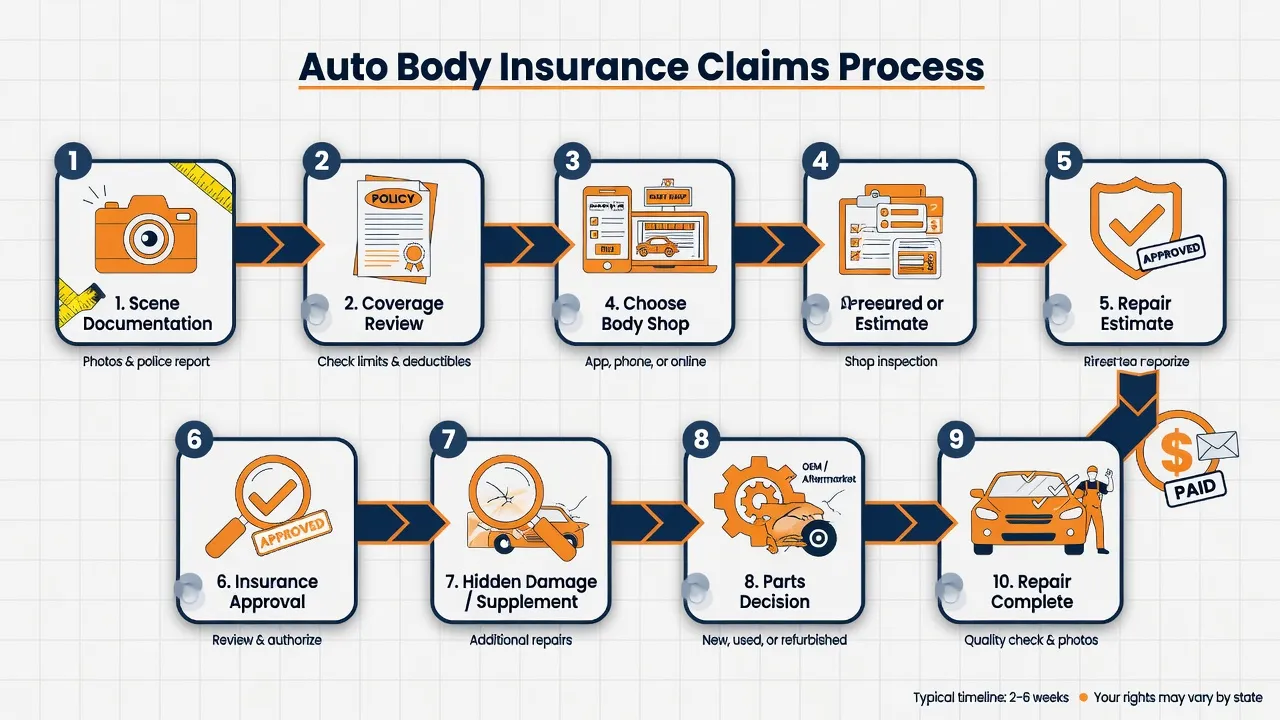

Step 3: File the claim and understand the adjuster's role

Once documentation is complete and coverage type is determined, report the claim to the appropriate insurance company. Most insurers offer three channels: online portal, mobile app, or phone.

When to file — and whether filing always makes sense

Filing a claim isn't always the right financial call. For very minor damage where the repair cost is close to or below the deductible, paying out of pocket may be more cost-effective when you factor in potential premium increases. A working rule: if the repair cost is less than the deductible plus the expected premium increase over two to three years, paying out of pocket may make more sense.

For damage above $1,500 to $2,000, filing a claim is typically the right financial decision for most policyholders.

What the insurer needs from you

When filing, insurers will request:

- The date, time, and location of the incident

- A description of how the damage occurred

- Photos of the damage and the scene

- Police report number, if applicable

- Contact information and insurance details of any other parties involved

- Any witness contact information

The insurer will provide a claim number and assign an adjuster. Keep that claim number handy — every call or communication after that should reference it.

What an insurance adjuster does — and doesn't do

An insurance adjuster is the insurer's representative who assesses vehicle damage and determines what the insurer will pay toward repair. Adjusters are trained professionals, but they represent the insurance company's financial interests — not yours.

Most adjusters today use estimating software — mainly CCC ONE, the industry-standard platform used for roughly 70% of U.S. collision repair estimates, according to CCC Intelligent Solutions. This software generates repair cost estimates based on time standards and parts pricing, but it works from photos or a visual inspection rather than a full disassembly. That matters: hidden structural damage, electronics, and safety systems are often invisible until the vehicle is taken apart at the body shop.

The result: there's typically a gap between the insurer's initial estimate and the final approved repair cost of $1,200 to $1,800, according to CCC Crash Course 2026 data. This gap is normal. It doesn't mean the initial estimate was wrong — it means disassembly reveals what photos can't. Knowing this upfront prevents confusion when the supplement process begins.

For a deeper look at what adjusters do and how to spot tactics that may not serve your interests, see our guide to insurance adjuster tactics to watch for.

Step 4: Choose your body shop — you have the right to decide

This is one of the most important and most misunderstood consumer rights in the auto body shop insurance claim process. In every U.S. state, car owners have the legal right to have their vehicle repaired at any licensed body shop of their choosing.

Your legal right to choose any licensed shop

More than 40 U.S. states have enacted anti-steering statutes that explicitly prohibit insurance companies from requiring policyholders to use a specific repair facility. Even in states without specific statutes, the right to choose is established through insurance regulations and case law.

Insurance companies can recommend a shop. They can't require one. If an insurance representative implies that coverage will be reduced, claims will be delayed, or repairs won't be guaranteed if you choose a non-preferred shop, that's likely inaccurate — and in many states, illegal.

What is insurance steering — and why it matters

Insurance steering is the practice of directing car owners toward an insurer's preferred shop — called a Direct Repair Program (DRP) shop — through pressure, misleading language, or implied consequences for going elsewhere.

Common steering tactics include:

- Repeatedly suggesting a specific shop, sometimes multiple times in a single call

- Using language like "approved shop" or "our shop" in ways that imply other shops aren't acceptable

- Implying that using a non-DRP shop will mean slower claims processing or less thorough warranty coverage

- Suggesting the insurer can't "guarantee" work done at a non-preferred shop

None of these implications is accurate. The insurance company must pay reasonable repair costs at any licensed facility you choose.

DRP shops vs. independent body shops: understanding the tradeoffs

Direct Repair Program (DRP) shops have contractual agreements with one or more insurance companies. In exchange for a steady volume of referrals, DRP shops agree to certain terms — including target labor times, preferred parts sourcing, and administrative procedures that speed up the insurer's process.

Independent body shops have no such agreement with insurers. They work for the vehicle owner, not the insurance company's workflow.

| Factor | DRP Shop | Independent Shop |

|---|---|---|

| Authorization speed | Faster — pre-approved workflow | May take slightly longer |

| Parts sourcing | May default to insurer-preferred parts | More likely to advocate for OEM |

| Primary client | Insurance company's process | Vehicle owner |

| Estimate advocacy | May align with insurer's first estimate | More likely to supplement aggressively |

| Warranty | Typically backed by insurer | Backed by shop |

Neither DRP nor independent shops are inherently better or worse. The right choice depends on the situation, the specific shop's reputation, and your priorities. For a full comparison, see our detailed guide to DRP shops vs. independent body shops.

When evaluating any shop — DRP or independent — consider:

1. I-CAR Gold Class certification (indicates ongoing technician training)

2. OEM certifications for your vehicle's make

3. Written warranty on all workmanship

4. Willingness to explain the repair process in plain language

5. Reviews that specifically mention collision repair quality

To find certified auto body shops near you for collision repair, search by location.

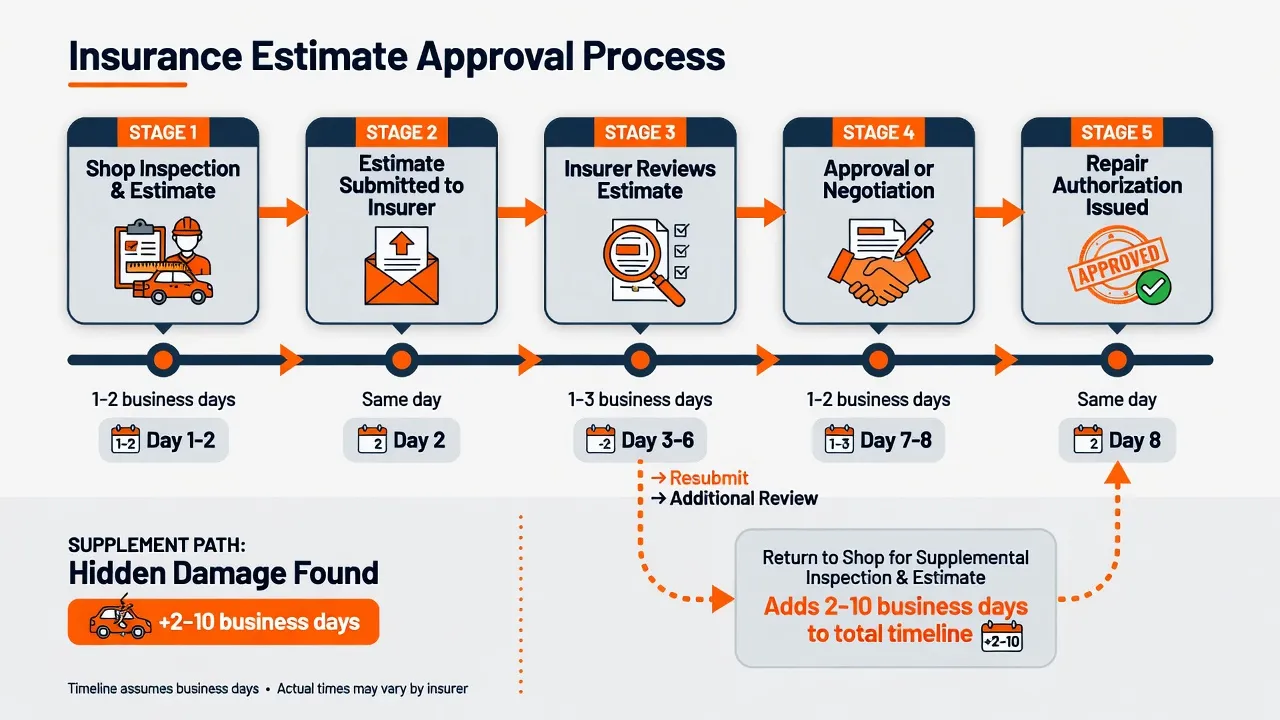

Step 5: The repair estimate and insurance approval process

Once you've chosen a body shop, the shop performs a damage assessment and creates a repair estimate. This estimate goes to the insurance company for review and approval before work begins.

How shops estimate damage

Body shops use the same CCC ONE estimating platform that insurers use, plus their own inspection process. A trained estimator writes out each repair operation in line-item detail: panel replacement or repair, labor time, paint materials, parts pricing, and sublet operations like wheel alignment or mechanical repair.

The body shop's estimate covers the full cost of returning the vehicle to its pre-accident condition. This number may be higher than the insurer's initial estimate — and that gap is normal, because the shop has physically inspected the vehicle while the adjuster may have worked from photos.

How insurers review estimates

The insurance company reviews the shop's estimate line by line and either approves it, negotiates specific line items, or requests additional documentation. This review process typically takes one to three business days for standard collision repairs.

Typical approval timeline by stage

| Stage | Typical Timeline |

|---|---|

| Initial claim filing | Same day to 24 hours |

| Adjuster inspection or photo review | 1–3 business days |

| Initial estimate approval | 3–5 business days from filing |

| Supplement review (when needed) | 2–10 additional business days |

| Parts ordering (after approval) | 1–7 business days depending on parts |

| Actual repair | Varies by damage — 1 day to 3+ weeks |

Step 6: What happens when hidden damage is found in your auto body insurance claim

The supplement process is one of the most common and least understood parts of the auto body insurance claim process — yet most car owners have never heard the term before they're in the middle of a claim.

What a supplement is and why it happens

An insurance supplement is an addition to the original repair estimate for damage discovered after the vehicle is taken apart. When technicians remove panels, bumper covers, and trim pieces to start the repair, they regularly find damage that wasn't visible from the outside — damage the initial estimate couldn't account for because it was based on photos or a surface inspection.

According to CCC Crash Course 2026 data, 63% of collision repairs require at least one supplement, with an average estimate gap of $1,200 to $1,800 between the initial adjuster figure and the final approved repair cost.

Common supplement-triggering discoveries include:

- Damaged frame rails or structural members behind a bumper assembly

- Cracked or shattered mounting brackets for cameras, sensors, and ADAS components

- Bent suspension components hidden by a wheel and tire

- Electrical damage to wiring harnesses

- Water intrusion damage behind door panels

A supplement isn't a red flag or a sign of a dishonest shop. In most collision repairs, it's the expected result of disassembly revealing what the initial inspection couldn't.

How the supplement process works

- The body shop technician finds additional damage during teardown

- The shop documents the damage with photographs and an updated estimate

- The shop submits the supplement to the insurance company

- The insurer reviews the supplement — either approving it, requesting an adjuster reinspection, or negotiating specific items

- Once approved, the shop continues or completes the repair

The supplement approval process typically adds 2 to 10 business days to the repair timeline, depending on whether the insurer accepts the shop's documentation or sends a reinspector.

A real-world supplement scenario

A driver's car is towed in after a rear-end collision. The initial adjuster estimate is $2,400, covering the rear bumper cover, tailgate, and paint. During disassembly, the technician finds a cracked frame rail on the driver's side and a damaged mount for the rear backup camera and parking sensors. The shop submits two supplements over the course of the repair. The final insurer-approved total: $5,900.

The car owner's out-of-pocket cost stayed the same — their deductible. The supplements covered the hidden structural and electronic damage. That's exactly how the process is supposed to work.

What to do if the insurer denies a supplement

If the insurer denies a legitimate supplement, the shop will typically negotiate directly. Your role is to stay informed and make sure the shop advocates for the full repair scope. If the dispute can't be resolved, escalation options include an independent appraisal and the appraisal clause in the policy. See Step 10 for the full dispute process.

For a detailed walkthrough, see what is an insurance supplement in auto body repair.

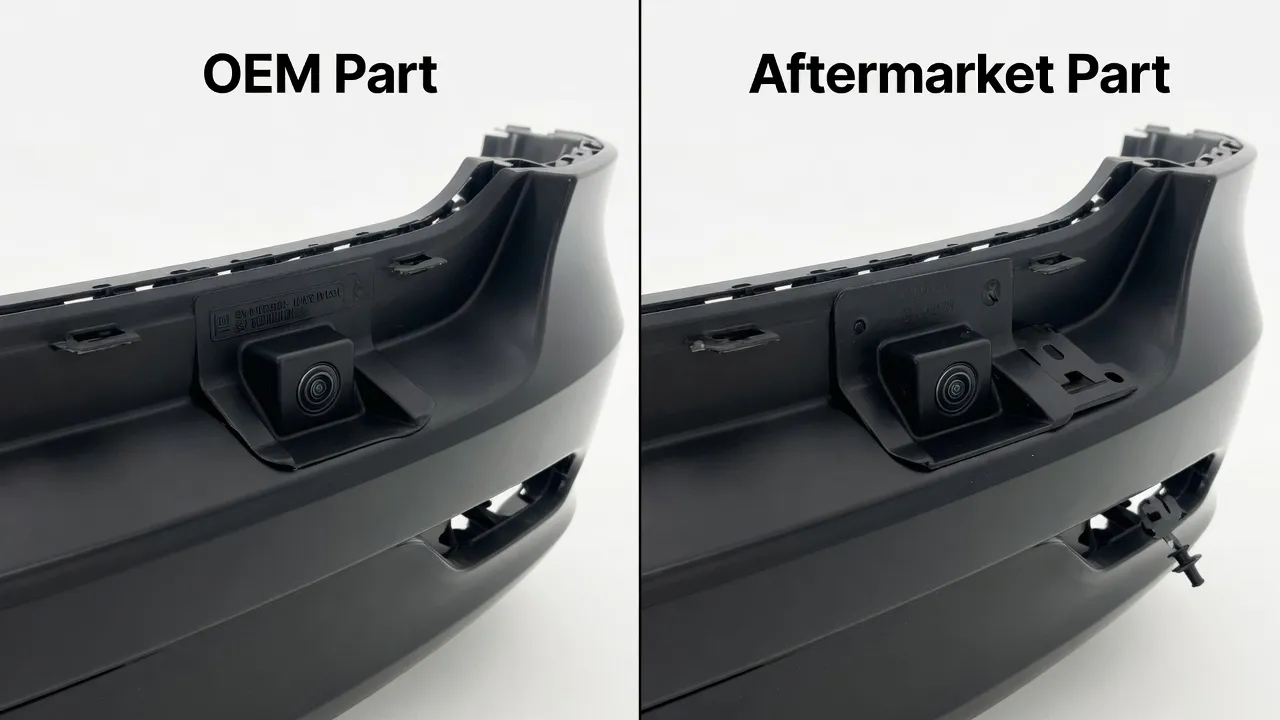

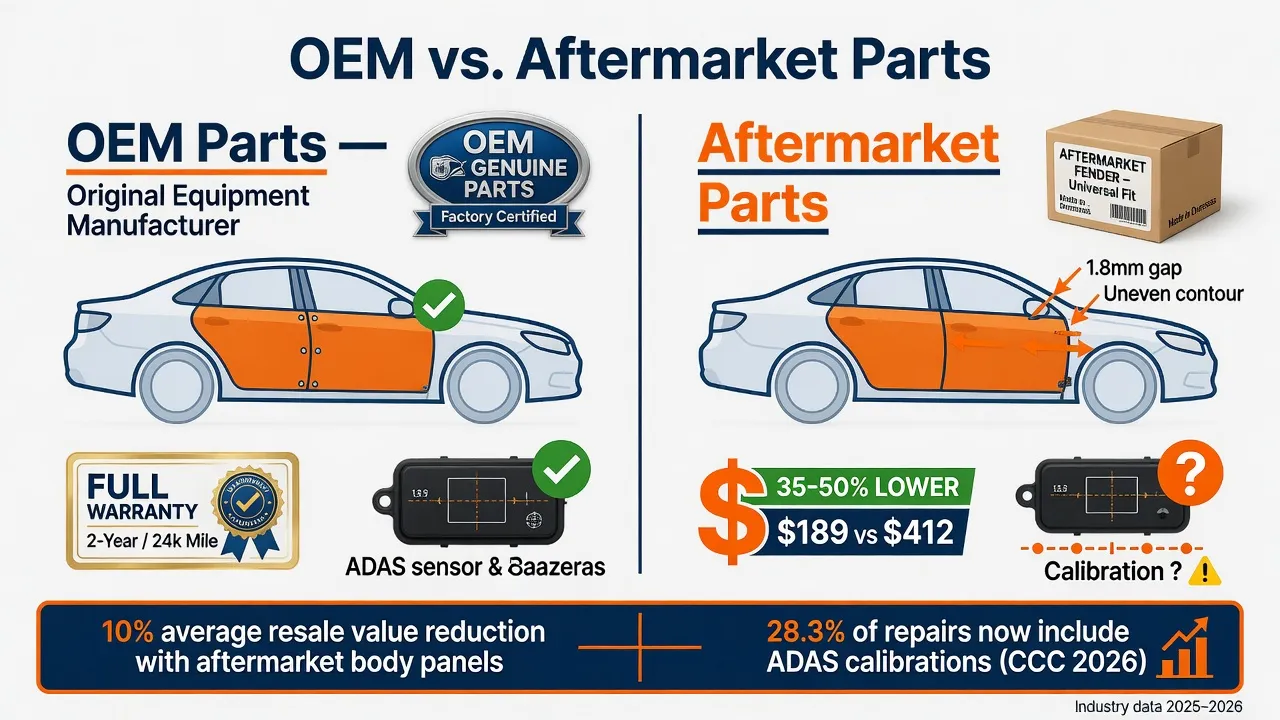

Step 7: OEM vs. aftermarket parts in a collision repair insurance claim

When the insurance company approves a repair, it also specifies what type of parts will be used. This is one of the most consequential decisions in the claims process — and one the insurer often makes without telling the car owner.

OEM parts vs. aftermarket parts vs. recycled parts

OEM (Original Equipment Manufacturer) parts are made by or for the vehicle's manufacturer to the same specifications as the original components. They're guaranteed to fit correctly and match the vehicle's existing systems — including ADAS sensors, cameras, and radar modules.

Aftermarket parts are produced by third-party manufacturers, not the original vehicle maker. They're typically less expensive but vary in quality, and their fit and finish may not match OEM specifications exactly.

Recycled (used OEM) parts are original manufacturer parts salvaged from other vehicles. They're OEM quality but pre-owned, and their condition depends on the donor vehicle.

Why aftermarket parts matter more in modern vehicles

According to CCC Crash Course 2026 data, 28.3% of all repairable repair estimates now include Advanced Driver Assistance Systems (ADAS) calibrations — up from 21.8% the prior year. The average calibration fee is $485.56 per repair.

This matters because bumpers, hoods, side panels, and windshields house the cameras, radar units, and ultrasonic sensors that power modern safety systems — lane departure warning, automatic emergency braking, blind spot monitoring, and adaptive cruise control. When aftermarket parts with slightly different mounting positions or material composition replace these components, ADAS calibration becomes more complicated and less reliable.

What insurance companies default to — and what car owners can do

Insurers typically default to aftermarket parts because they cost less. But several states have enacted laws protecting car owners' rights on parts choices:

- California requires written disclosure when non-OEM parts are used and gives car owners the right to request OEM parts

- Six states require owner consent before non-OEM parts can be used in a repair

- Many states have regulations requiring that non-OEM parts meet OEM quality standards

Independent of state law, you can request OEM parts in writing. For newer vehicles still under manufacturer warranty, using non-OEM structural parts may affect warranty coverage — a concern worth raising with both the shop and the insurer.

The resale value impact is real: research from trade-in surveys shows that vehicles repaired with aftermarket body panels lose roughly 10% more in resale value compared to vehicles repaired with OEM parts.

For a complete guide to this issue, see OEM vs. aftermarket parts in insurance claims.

Step 8: Rental car coverage during repairs

Most car owners assume their auto insurance automatically covers a rental vehicle while their car is being repaired. It doesn't — unless rental reimbursement coverage was specifically added to the policy.

Rental reimbursement coverage: a separate add-on

Rental reimbursement is typically an optional endorsement on a standard auto insurance policy, not a default inclusion. It usually provides coverage of $30 to $50 per day, with a total claim limit of $900 to $1,500. Costs above those limits are the car owner's responsibility.

Before assuming rental coverage exists, verify it in the policy declarations page. When filing a claim, ask the insurer specifically: "Does my policy include rental reimbursement, and what are the daily and total limits?"

Third-party claims and rental coverage

If you're filing a third-party claim against the at-fault driver's insurer, the at-fault driver's liability coverage typically includes compensation for your loss of use of the vehicle while it's being repaired. This means you may be entitled to rental coverage from the at-fault driver's insurer even if your own policy doesn't include rental reimbursement.

What happens when repairs run long

Repair timelines for complex collision repairs can run several weeks. ADAS calibrations, parts delays, and supplement approvals all add time. If the repair runs past the rental reimbursement limit, your options include:

- Requesting a rental extension through the insurance company with documentation of the delay cause

- Negotiating with the at-fault insurer for extended loss-of-use compensation

- Checking whether a credit card used to reserve the rental provides supplemental rental coverage

For a full guide on what rental coverage covers and where the gaps are, see rental car coverage after an accident.

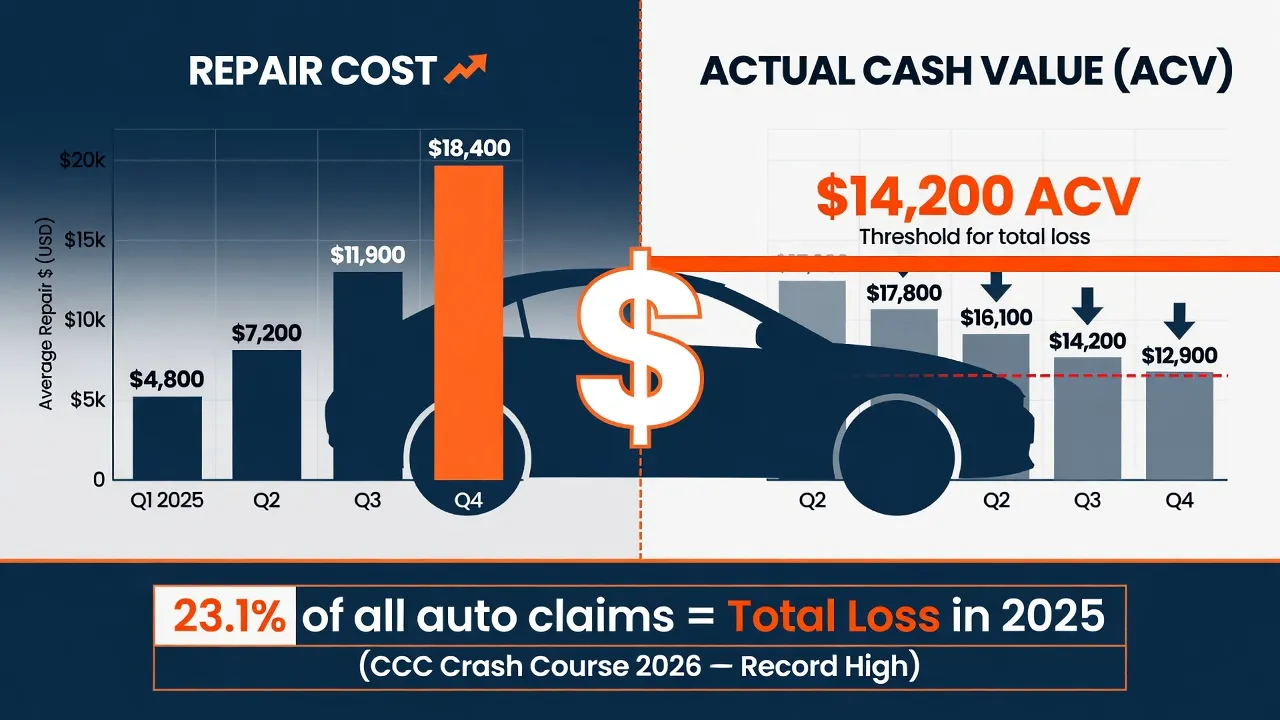

Step 9: When insurance wants to total your car

According to CCC Crash Course 2026 data, 23.1% of all auto insurance claims resulted in a total loss in 2025 — a record high. With average repair costs rising and vehicle values fluctuating, more cars are crossing the total loss threshold than in any previous year.

Knowing how total loss is determined — and what rights apply — can change the outcome.

How total loss is determined

Insurance companies use one of two methods:

Total Loss Threshold (TLT): A fixed percentage of the vehicle's pre-accident Actual Cash Value (ACV). If repair costs exceed that percentage, the vehicle is declared a total loss. Most states set this threshold between 70% and 80% of ACV.

Total Loss Formula (TLF): Compares repair cost plus salvage value to the vehicle's ACV. If repair cost + salvage value ≥ ACV, the vehicle is totaled. This formula is used in states without a fixed threshold.

How ACV is calculated — and how to challenge it

Actual Cash Value (ACV) is the insurer's determination of what the vehicle was worth immediately before the accident. Insurers typically use proprietary valuation software that factors in the vehicle's year, make, model, mileage, condition, and comparable sales in the local market.

You have the right to challenge the ACV determination. Steps to dispute include:

1. Research comparable vehicles actively listed for sale in the local market

2. Document the vehicle's condition, recent maintenance, and any upgrades

3. Request an explanation of the specific comparables the insurer used

4. Submit evidence of higher comparable sales prices in writing

Rights when disagreeing with a total loss determination

Car owners who believe the ACV is too low can invoke the appraisal clause in their policy — a binding dispute resolution mechanism where independent appraisers from each party agree on value. If the appraisers can't agree, an umpire makes the final determination.

Keeping a totaled vehicle

You can sometimes choose to keep a vehicle declared a total loss. In that case, the insurer deducts the salvage value from the ACV settlement, and the vehicle receives a salvage title. A salvage title vehicle requires a DMV inspection and gets a "rebuilt" title before it can legally be driven on public roads. Financing and insuring a salvage-title vehicle is harder and typically more expensive.

For a complete guide to total loss rights, options, and the ACV dispute process, see insurance totaled my car: your rights and options.

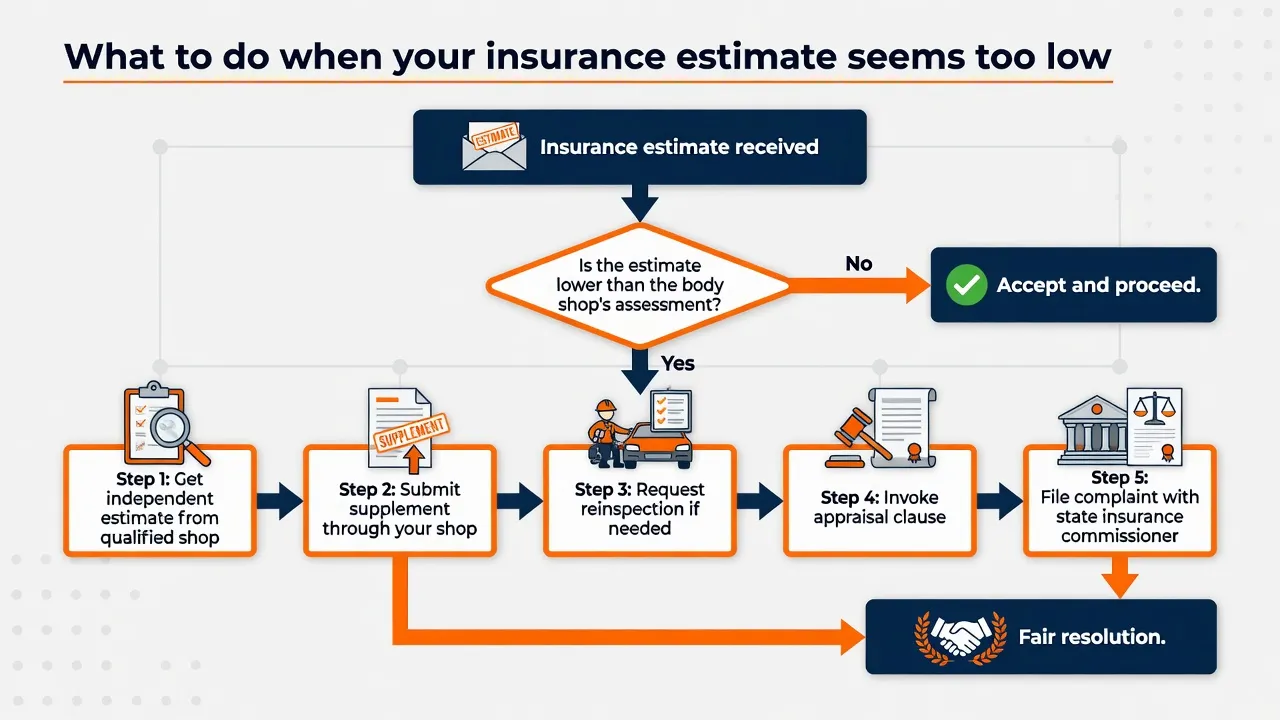

Step 10: What to do if the insurance estimate is too low

Getting an estimate that seems insufficient to cover the full repair is one of the most common mid-claims friction points. Knowing why estimates are sometimes low — and what to do about it — is key to getting a fair outcome.

Why initial estimates are often lower than actual repair cost

Initial insurance estimates are frequently conservative for several reasons:

- Photo-based assessments miss hidden damage — adjusters working from photos can't see structural components, electronics, or mounting hardware behind exterior panels

- Software defaults to lower labor times — estimating software uses average time standards that may not reflect the specific complexity of a repair

- Parts defaults to aftermarket — the estimate may price aftermarket parts where OEM is appropriate or required

- Not all operations are included initially — standard repair operations like corrosion protection or ADAS calibration may be left out of an initial estimate

How to dispute a low insurance estimate

Step 1: Get a second estimate from a qualified body shop

If the shop you've chosen disagrees with the insurer's estimate, the shop's written counter-estimate is the first piece of documentation for a dispute.

Step 2: Request a reinspection

Ask the insurer to send a reinspector to the shop — where they can physically inspect the vehicle rather than rely on photos. Physical reinspections often result in higher approved amounts.

Step 3: File a supplement through the body shop

The most common path to resolution is through the supplement process. The shop documents the difference, submits it as a supplement, and negotiates with the adjuster. You don't typically need to manage this directly — a good shop will handle it.

Step 4: Invoke the appraisal clause

Every standard auto insurance policy includes an appraisal clause that allows either party to demand a binding appraisal by independent appraisers when there's a dispute over the claim amount. It's a formal but effective tool that bypasses the standard negotiation process.

Step 5: Contact the state insurance commissioner

State Departments of Insurance handle consumer complaints against insurers. Filing a formal complaint often prompts an insurer to revisit a disputed estimate. The complaint process is free and doesn't require an attorney.

Step 6: Consult a public adjuster or attorney

For large disputes — particularly involving structural damage or total loss — a licensed public adjuster or an attorney specializing in insurance disputes can negotiate on your behalf.

For a step-by-step dispute roadmap, see our guide to what to do when your insurance estimate is too low.

Diminished value: the claim most car owners don't know about

Even after a complete, professionally executed repair, a vehicle's market value is typically lower than it was before the accident. A prospective buyer looking at vehicle history will see the accident on the Carfax or AutoCheck report — and will offer less. This loss in value is called diminished value, and in most states, car owners can file a claim to recover it.

What diminished value is

Diminished value is the difference between a vehicle's market value before an accident and its market value after repair. There are three types:

Inherent diminished value is the most common and most claimed: the drop in market value that results from the vehicle's accident history alone, regardless of repair quality.

Repair-related diminished value results from poor-quality repairs that leave the vehicle in below-standard condition — mismatched paint, ill-fitting panels, or unrepaired structural damage.

Immediate diminished value is the difference in value immediately after the accident, before any repairs are made. This is typically not the basis for a claim.

Who can file a diminished value claim

Diminished value claims are most clearly available when filing a third-party claim against the at-fault driver's insurer. All U.S. states except Michigan recognize third-party diminished value claims for injury to personal property.

First-party diminished value claims — filing against your own insurer after an at-fault accident — are harder, as most state courts have found that insurers don't owe diminished value to their own policyholders unless the policy specifically includes it. Georgia is a notable exception.

How diminished value amounts are calculated

Insurers often use a formula called the 17c formula to calculate DV amounts. Consumer advocates widely criticize this formula as significantly undervaluing actual losses. An independent appraisal from a qualified diminished value expert typically yields a higher figure and is useful documentation if the insurer's offer is challenged.

Average diminished value amounts vary by damage severity: roughly $500 to $1,500 for minor accidents and $2,100 or more for major structural repairs, though the vehicle's original market value is the biggest factor.

For a complete guide to calculating and filing a diminished value claim, see how to file a diminished value claim.

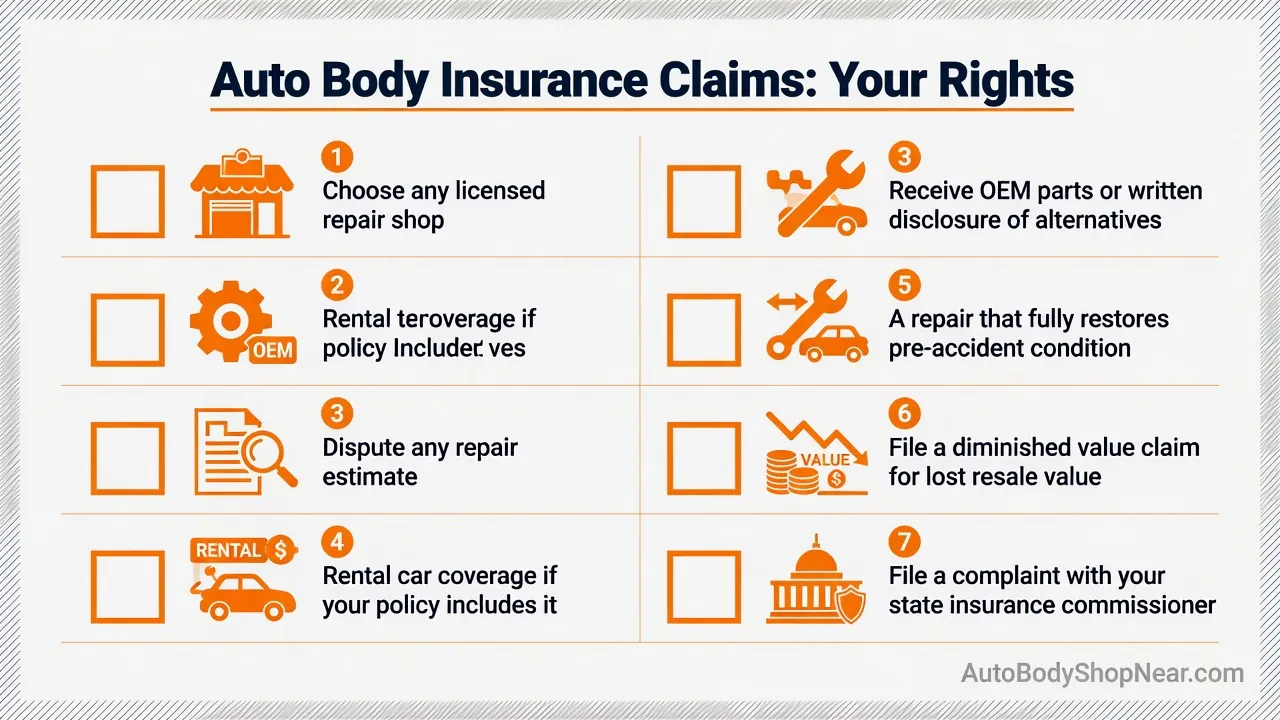

Consumer rights summary: what every car owner should know

The auto body insurance claims process is complex, but car owners have substantial legal protections most insurers won't proactively explain.

The right to choose your repair shop: In all 50 states, car owners can choose any licensed body shop for their repair. Insurers can recommend shops but can't require them. More than 40 states have anti-steering statutes that explicitly prohibit steering pressure.

The right to OEM parts or written disclosure: Several states require insurers to disclose when non-OEM parts will be used and give car owners the option to request OEM parts — sometimes at the car owner's cost above the aftermarket price.

The right to dispute the repair estimate: Car owners can dispute an estimate through the supplement process, an independent appraisal, and the policy's appraisal clause. No car owner is required to accept the first estimate offered.

The right to rental coverage: If rental reimbursement is included in the policy, the insurer must provide it. If filing third-party, the at-fault driver's insurer owes loss-of-use compensation.

The right to a complete repair: Insurance companies must pay to restore the vehicle to its pre-accident condition. Partial repairs that leave the vehicle below pre-accident standard aren't acceptable.

The right to file a diminished value claim: In almost every state, car owners not at fault can file a third-party claim for the reduction in vehicle value from the accident history.

The right to file a complaint: State Departments of Insurance handle complaints against insurers. These agencies have regulatory authority and can mandate reconsideration of denied or underpaid claims.

For a deeper look at the legal protections around shop choice and anti-steering, see your right to choose your own body shop.

Conclusion: handling the auto body insurance claim with confidence

Filing an auto body insurance claim is rarely as straightforward as insurers describe. Hidden damage supplements, parts disputes, rental coverage gaps, and total loss disagreements aren't exceptions — they're common occurrences that affect a large share of all collision claims.

The data speaks for itself: average repair costs have reached $4,818, 23.1% of claims now result in total loss, and 63% require at least one supplement. These numbers reflect real complexity in the claims process — complexity that car owners who know the process can handle far more effectively.

The most important takeaways:

- Document everything at the scene — photographs and written records protect your interests throughout the entire process

- Know your coverage before filing — collision vs. comprehensive, first-party vs. third-party, and deductible responsibility all affect the outcome

- Exercise the right to choose any licensed shop — the insurer can recommend; it can't require

- Expect the supplement process — 63% of collision repairs need one; it's normal and doesn't increase out-of-pocket costs

- Know OEM parts rights — for newer vehicles with ADAS systems, parts choice affects both safety system performance and resale value

- Dispute low estimates through the proper channels — the supplement process, appraisal clause, and state insurance commissioner all exist to protect car owners

- File a diminished value claim when eligible — it's money most car owners leave unclaimed

Finding a qualified auto body shop with experience handling insurance claims is the single most valuable step in this process. A shop that communicates clearly with insurers, handles the supplement process well, and advocates for complete repairs takes most of the burden off the car owner.

To find certified collision repair shops in your area, browse auto body shops near you or explore collision repair services for shops with the certifications and equipment to handle insurance claims effectively.

Last updated: June 2026. Insurance regulations and consumer rights vary by state. Consult your state's Department of Insurance or a licensed professional for advice specific to your situation.

Frequently asked questions about auto body shop insurance claims

How long does an auto body insurance claim take?

A standard collision repair insurance claim typically takes 1 to 2 weeks from filing to completed repair for minor to moderate damage. Complex repairs involving structural damage, ADAS calibration, or supplements can take 3 to 6 weeks. Initial insurer approval typically takes 3 to 5 business days; supplement reviews add 2 to 10 business days.

Do I pay the deductible to my insurance company or to the body shop?

The deductible is paid to the body shop at vehicle pickup, not to the insurance company. The insurance company pays the shop directly for the remainder of the approved repair amount. If you're filing a third-party claim against an at-fault driver's insurer, no deductible should be required.

Can the insurance company force me to use a specific body shop?

No. In all 50 U.S. states, car owners have the legal right to choose any licensed body shop. Insurers can recommend preferred shops, but they can't require them. More than 40 states have anti-steering laws that specifically prohibit pressure tactics designed to direct car owners to insurer-preferred facilities.

What is an insurance supplement in auto body repair?

An insurance supplement is an update to the original repair estimate for damage discovered during vehicle disassembly that wasn't visible in the initial inspection. According to CCC Crash Course 2026 data, 63% of collision repairs require at least one supplement. Supplement costs are paid by the insurer; the car owner's deductible doesn't increase.

What happens if the insurance company totals my car?

When repair costs exceed the state's total loss threshold (typically 70–80% of Actual Cash Value), the insurer may declare the vehicle a total loss. The insurer pays the car owner the ACV minus the deductible. Car owners can dispute the ACV determination using comparable vehicle sales data or by invoking the appraisal clause. The option to keep the totaled vehicle (with a salvage title) is available in most states.

Can I file a diminished value claim after my car is repaired?

Yes, in most states. Diminished value is the reduction in resale value that results from a vehicle's accident history, even after a complete repair. Third-party diminished value claims — filed against the at-fault driver's insurer — are recognized in all U.S. states except Michigan. The claim must typically be filed separately from the repair claim.