A car rolls out of the body shop fully repaired. New paint, straight panels, fresh bumper. The work's done correctly. And yet that car is worth less than it was before the accident.

Not because of poor repairs. Because of a four-word entry on a vehicle history report: accident reported on [date].

That loss in resale value — the gap between what a vehicle was worth before the crash and what it's worth after a complete repair — is called diminished value. Filing a diminished value claim is how car owners who weren't at fault recover that loss from the at-fault driver's insurance company. In most U.S. states, that right exists. Most car owners never exercise it, because their insurer doesn't mention it and they don't know the option exists.

This guide covers everything car owners need to know about diminished value claims: what qualifies, the three types of DV, how to calculate an amount, how to file, state-by-state eligibility, and what to do when the insurance company denies or undervalues the claim.

For a full overview of the auto body insurance claims process, see our complete guide to auto body shop insurance claims.

Diminished value laws vary by state. This guide provides general educational information. Consult your specific policy and your state's Department of Insurance for details applicable to your situation.

What is a diminished value claim?

A diminished value claim is a formal request for compensation from an at-fault driver's insurer for the reduction in a vehicle's market value caused by its accident history — even after the vehicle has been fully and professionally repaired. A vehicle with an accident record on Carfax sells for less than a comparable clean-history vehicle; that gap is what a DV claim recovers.

Buyers checking vehicle history reports see the accident disclosure and offer less than they would for a comparable vehicle with a clean history. A rule of thumb puts that stigma loss at 10% to 25% of pre-accident market value, depending on the vehicle's age, mileage, damage severity, and local resale market — though actual amounts vary considerably.

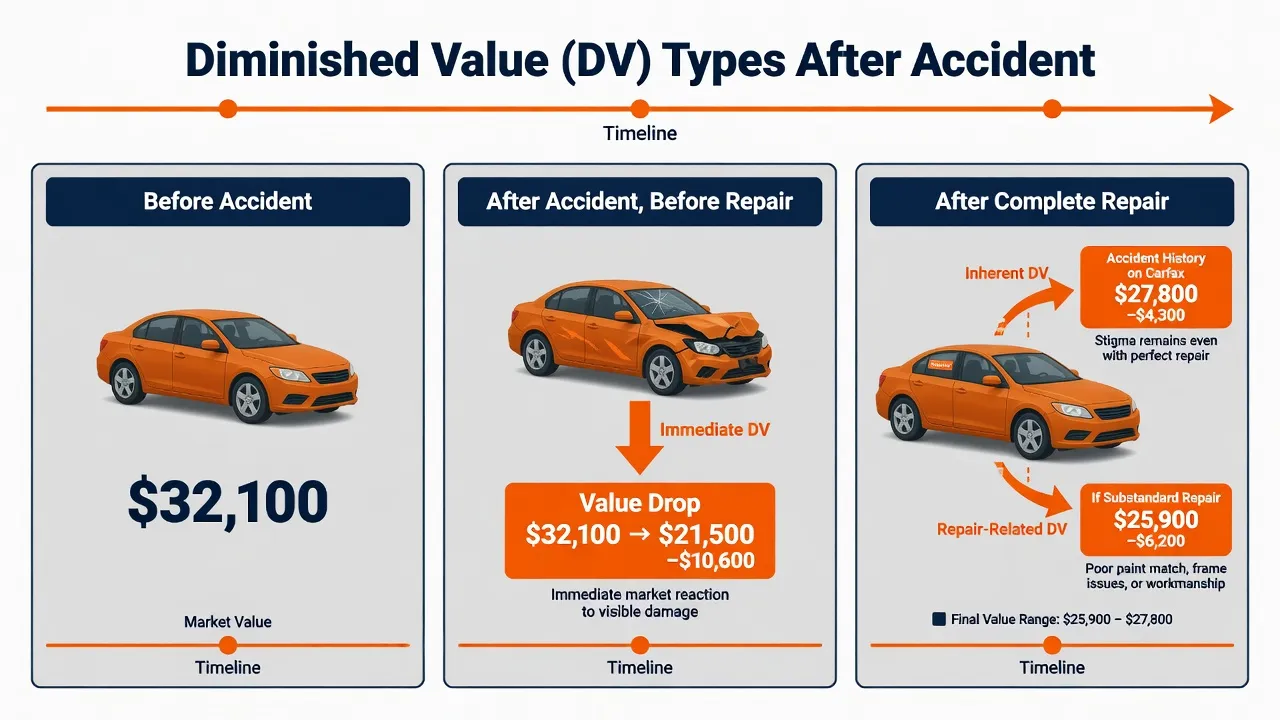

Here's a concrete example: a 2019 Toyota Camry XSE with a pre-loss market value of $32,100 was repaired after a moderate-severity collision at a cost of $6,621. After a complete, quality repair, the post-repair market value dropped to $29,060 — a diminished value loss of roughly $3,040 that the car owner could pursue through a third-party claim against the at-fault driver's insurer.

Diminished value is distinct from the cost of repairs. The insurer already paid for the physical repair. A DV claim addresses the separate, additional financial loss — the market value damage that a perfect repair can't undo.

Three types of diminished value

Not all diminished value is calculated or claimed the same way. There are three recognized types, and the distinction matters because only one of them forms the basis for most DV claims.

Inherent diminished value

Inherent diminished value is the most common type and the standard basis for DV claims. It's the drop in market value that results purely from the vehicle's accident history — regardless of repair quality. Even a flawless repair performed by a certified shop using OEM parts can't eliminate the Carfax entry. Buyers discount the vehicle because an accident happened, full stop.

This is the type of DV that insurers are asked to compensate, and it's what most DV claims are built around.

Repair-related diminished value

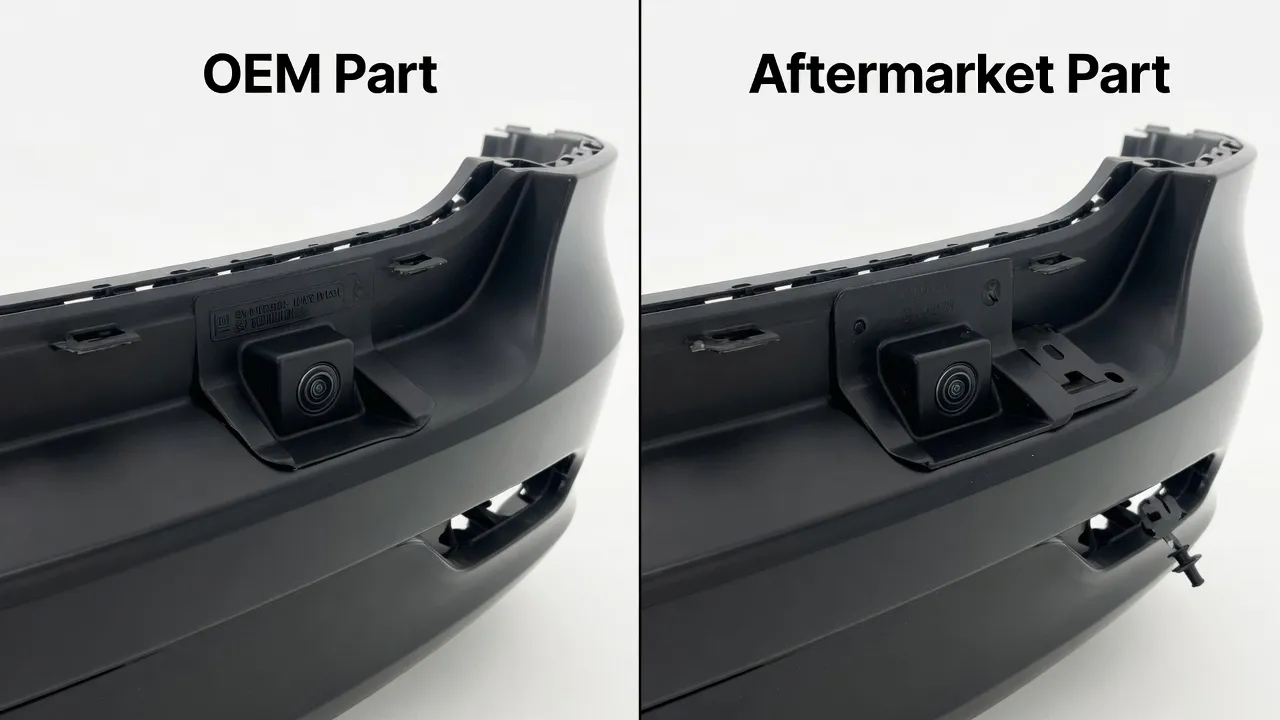

Repair-related diminished value results from substandard repair work that leaves the vehicle in worse-than-pre-accident condition. Examples include mismatched paint, improperly fitted panels, aftermarket parts that don't seat correctly, or unrepaired structural damage. This type of DV comes on top of inherent DV — and it's avoidable with quality repairs.

One reason OEM parts matter: vehicles repaired with aftermarket body panels can experience repair-related diminished value on top of the inherent loss. Research shows vehicles repaired with aftermarket structural panels lose roughly 10% more in resale value compared to OEM-repaired vehicles, above and beyond the accident-history stigma — a finding consistent with CCC Crash Course 2026 parts-quality data. For detail on parts rights, see our guide to OEM vs. aftermarket parts in insurance claims.

Immediate diminished value

Immediate diminished value is the difference in market value between the vehicle's pre-accident worth and its value immediately after the accident, before any repairs are completed. This type is rarely the basis for a DV claim because it doesn't account for the repair that follows. It's more relevant in situations where a vehicle is totaled and never repaired. For total loss situations, see insurance totaled my car: rights and options.

Who qualifies to file a diminished value claim

Several conditions determine whether a car owner can file a viable DV claim.

Fault: third-party claims are the clearest path

Diminished value claims are most straightforward when the car owner was not at fault and files a third-party claim against the at-fault driver's insurer. In this scenario, the at-fault driver's property damage liability coverage is responsible for making the non-fault driver whole — and "whole" includes compensating for lost resale value, not just the physical repair.

First-party DV claims — filing against your own insurer after an at-fault accident — are a harder path. Most states' courts have held that standard collision coverage doesn't require insurers to pay diminished value to their own policyholders. Four states are notable exceptions: Georgia, Kansas, Louisiana, and North Carolina allow first-party DV claims with varying rules. Georgia is the strongest: the 2001 State Farm Mutual Automobile Insurance Co. v. Mabry ruling established that Georgia insurers must evaluate and compensate for inherent diminished value even in first-party claims. Car owners in Georgia have access to the broadest first-party DV protections in the country — see auto body shops in Georgia for certified shops familiar with documenting DV-supporting repair records.

Vehicle eligibility factors

Not every vehicle produces a viable DV claim. Several factors affect whether a claim is likely to succeed and how much it's worth:

- Vehicle age and mileage: Newer vehicles with lower mileage sustain more meaningful DV loss. A 3-year-old vehicle with 18,000 miles loses a greater percentage of its remaining value from an accident entry than a 10-year-old vehicle already depreciated to a fraction of its original price

- Pre-accident value: Higher-value vehicles produce larger DV amounts in absolute dollar terms. Luxury and near-luxury vehicles (Mercedes, BMW, Lexus) typically see DV losses in the 15–25% range; standard sedans in the 10–15% range

- Damage severity: More extensive damage — especially structural damage requiring frame repair — produces greater DV loss than cosmetic-only damage

- Prior accident history: A vehicle with a pre-existing accident entry on its history report has already lost some DV value. A second entry on a vehicle that already shows prior damage produces less incremental loss

- Repair quality: A well-documented, quality repair using OEM parts reduces repair-related DV, though it can't eliminate inherent DV

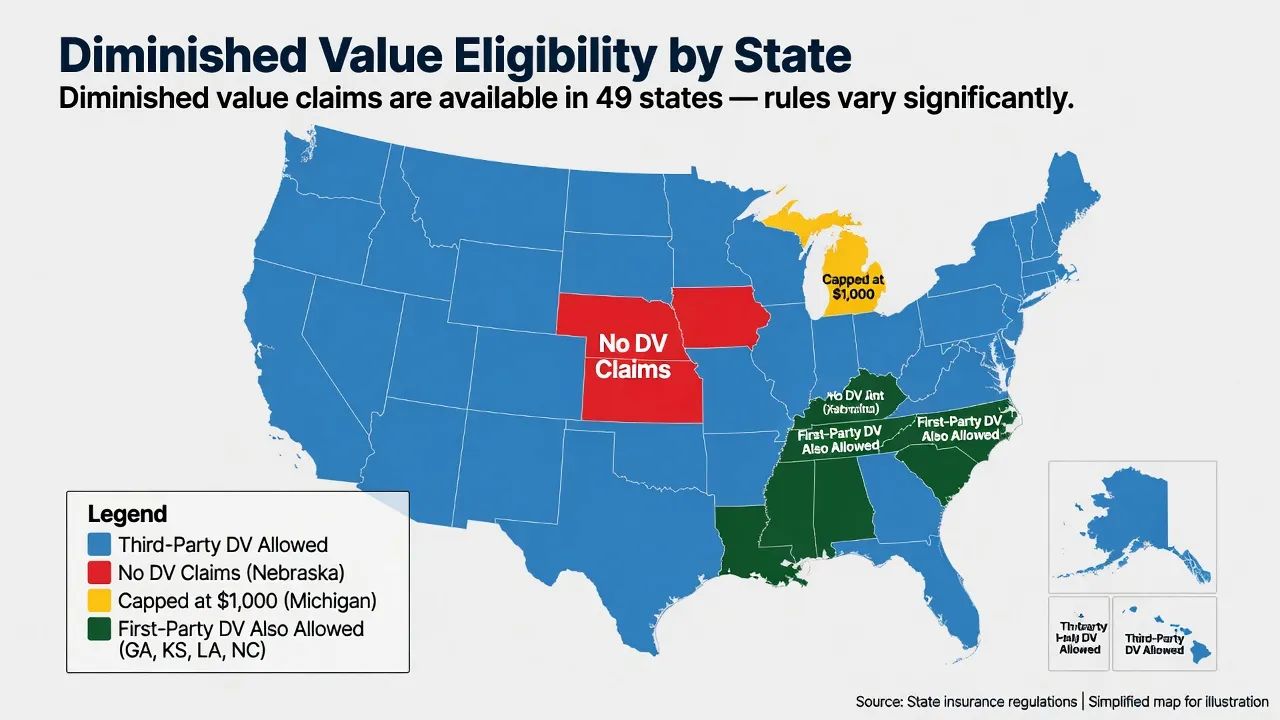

State eligibility

Diminished value claim rights vary by state. The table below summarizes the eligibility landscape.

| Eligibility | States / Notes |

|---|---|

| Third-party DV claims (all forms) | All 50 states except Nebraska |

| Nebraska | Does not recognize DV claims |

| Michigan | DV recovery capped at $1,000 under mini-tort statute |

| First-party DV claims allowed | Georgia, Kansas, Louisiana, North Carolina |

| Georgia (strongest first-party state) | Mabry ruling requires insurers to proactively offer DV evaluation |

| UM/UIM coverage extends DV eligibility | California, Georgia, Illinois, Indiana, TX, and others |

| Shortest statute of limitations | Louisiana — 1 year |

| Longest statute of limitations | Rhode Island — 10 years |

| Typical statute of limitations | 2–4 years (most states) |

Always verify current state laws with your state's Department of Insurance, as statutes evolve. A detailed state-by-state eligibility reference is available at crashrepairinfo.com. For state-specific body shop and insurance resources, browse auto body shops by state.

How diminished value is calculated: the 17c formula and its limits

Insurance companies have a standard tool for calculating diminished value: a formula known as 17c, originally developed during State Farm litigation in Georgia. Knowing how it works — and why it often underestimates real-world losses — is essential before filing a claim.

How the 17c formula works

The 17c formula uses four variables:

Step 1 — Base loss of value: Multiply the vehicle's pre-accident market value by 10%. This 10% is the formula's structural ceiling — the maximum possible DV under the formula regardless of how severe the damage was.

Step 2 — Damage severity multiplier: Multiply the base loss by a damage multiplier based on the extent of damage:

| Damage Level | Multiplier |

|---|---|

| No structural damage, minor cosmetic | 0.00 |

| Minor cosmetic issues (small dents, chips, scrapes) | 0.25 |

| Moderate damage (panels, paint, some structure) | 0.50 |

| Major damage to structure, airbag deployment | 0.75 |

| Severe structural damage, multiple systems affected | 1.00 |

Step 3 — Mileage multiplier: Multiply again by a mileage-based adjustment:

| Mileage | Multiplier |

|---|---|

| 0–19,999 miles | 1.00 |

| 20,000–39,999 miles | 0.80 |

| 40,000–59,999 miles | 0.60 |

| 60,000–79,999 miles | 0.40 |

| 80,000–99,999 miles | 0.20 |

| 100,000+ miles | 0.00 |

The formula: Pre-accident value × 10% × Damage multiplier × Mileage multiplier = Estimated DV

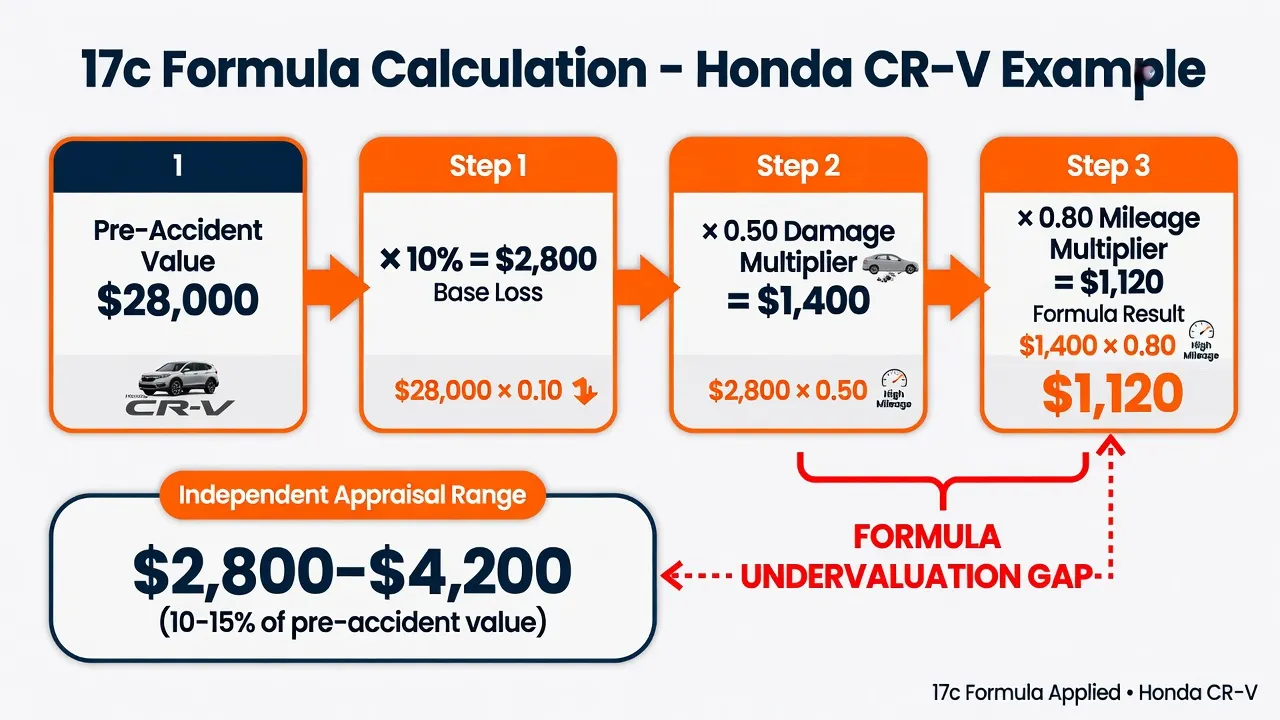

A worked example

A 2021 Honda CR-V EX with a pre-accident market value of $28,000. Mileage: 34,000. Damage: moderate (panels and paint, some structural).

- Base loss: $28,000 × 10% = $2,800

- Damage multiplier (moderate = 0.50): $2,800 × 0.50 = $1,400

- Mileage multiplier (34,000 miles = 0.80): $1,400 × 0.80 = $1,120

The 17c formula produces $1,120 in estimated diminished value.

An independent appraiser evaluating actual market comparables for the same vehicle — comparing what a clean-history 2021 CR-V EX sells for versus accident-history examples — might find a real-world DV loss closer to $2,800 to $4,200, which is 10% to 15% of the pre-accident value.

That gap is significant. Consumer advocates consistently describe the 17c formula as a tool designed to contain insurer payouts, not accurately represent market reality.

Why the 17c formula undervalues most claims

The formula has two built-in constraints that systematically cap payouts below actual market loss:

The 10% ceiling is arbitrary: Real-world market data shows that accident-history vehicles frequently lose 15% to 25% of their pre-accident value in resale pricing, particularly luxury vehicles, late-model vehicles, and vehicles with structural damage involving airbag deployment. The 17c cap of 10% doesn't reflect this.

The damage multiplier is subjective: There's no universal standard for classifying damage as 0.25 versus 0.50 versus 0.75. Insurance adjusters applying the formula often classify damage at the lower severity level, producing lower multiplier values.

The 100,000-mile cutoff is blunt: The formula produces zero DV for any vehicle with more than 100,000 miles, regardless of the vehicle's actual value or the severity of its damage. A well-maintained 102,000-mile truck worth $22,000 produces no DV under the formula.

The 17c formula is a starting point for negotiation, not the final word on what a DV claim is worth. Many car owners searching for a diminished value calculator end up running the 17c formula manually — it's the most widely referenced method — but independent appraisers use market-comparable analysis that routinely produces higher figures.

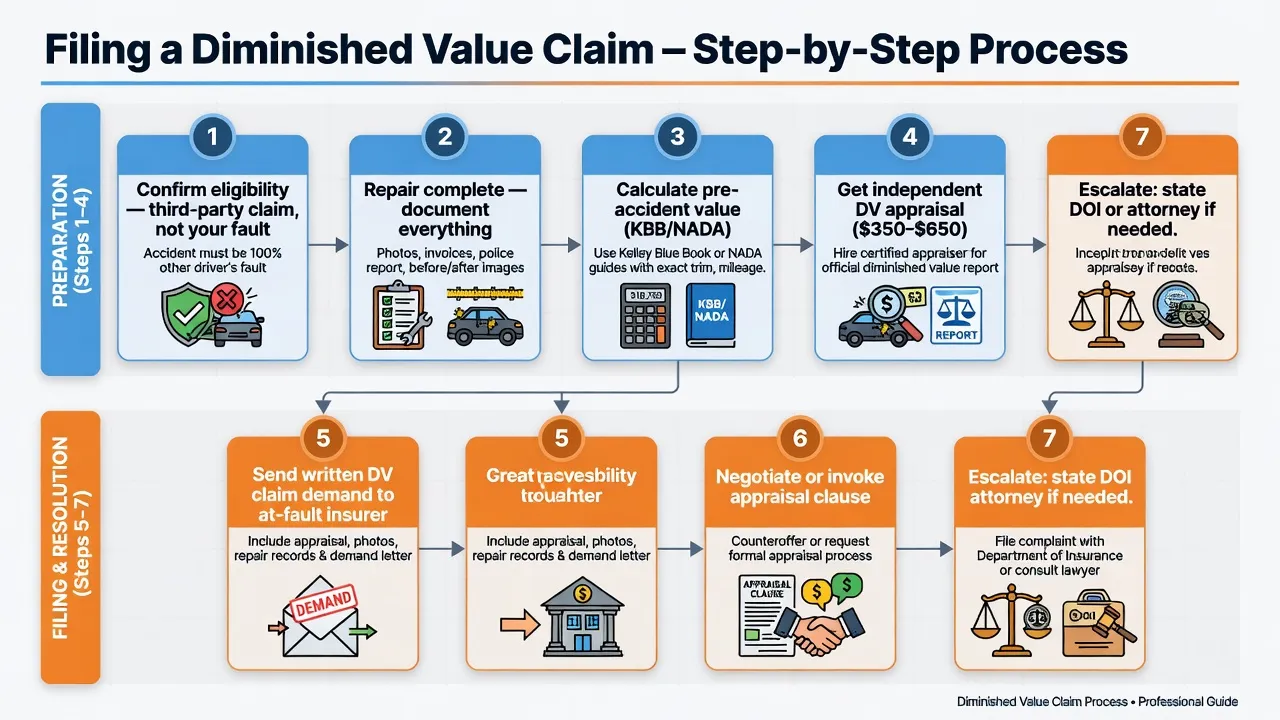

How to file a diminished value claim: step-by-step process

Filing a diminished value claim follows a distinct process from the standard repair claim. Here's the complete sequence.

Step 1: Confirm eligibility and claim type

Verify that the accident was the other party's fault and that state law allows DV claims. If filing a third-party claim, the at-fault driver must have active liability insurance (or the car owner must have Uninsured Motorist/Underinsured Motorist coverage, which extends DV eligibility in many states).

Note the statute of limitations in the state where the accident occurred. Most states give two to four years, but Louisiana allows only one year. Filing before the deadline is non-negotiable.

Step 2: Ensure the repair is complete

A diminished value claim is typically filed after repairs are complete, not before. The post-repair vehicle condition is the baseline for calculating how much inherent value remains lost. Confirm that the repair was done correctly — quality repairs using OEM parts reduce repair-related DV but can't eliminate inherent DV. Request a copy of the final repair order with itemized parts and operations.

Filing before repair completion is possible in some states but complicates valuation. After-repair is the cleaner path.

Step 3: Establish the pre-accident market value

Gather documentation of the vehicle's pre-accident fair market value. The most widely accepted sources are:

- Kelley Blue Book (kbb.com) — trade-in and private party values

- NADA Guides (nadaguides.com) — used widely by insurers and courts

- Comparable active listings from Autotrader, Cars.com, and local dealer sites — filtered for same year, make, model, trim, mileage, and geographic region

Document the vehicle's condition before the accident: maintenance records, recent service, any upgrades. A well-documented pre-accident condition supports a higher base value.

Step 4: Get an independent diminished value appraisal

This is the step most car owners skip — and the most important one. An independent DV appraisal from a qualified appraiser produces a report that:

- Calculates the actual market-based DV (not just the 17c formula result)

- Documents the methodology and comparable sales used

- Provides a defensible, written opinion of value that carries weight in negotiations, arbitration, and court

What appraisals cost: Independent DV appraisals typically run $350 to $650 for standard vehicles; higher for luxury and exotic vehicles. Some appraisers charge a percentage of the claim.

What to look for in an appraiser: Credentials that matter include certification under the Uniform Standards of Professional Appraisal Practice (USPAP), membership in the International Automobile Appraisers Association (IAAA), and documented experience producing DV reports accepted by insurers and courts. Appraisers who are also ASE or I-CAR certified in collision damage assessment bring additional credibility.

If the expected DV amount is less than $500, a formal appraisal may cost more than the recovery warrants. In those cases, self-calculating with documented comparable sales and submitting a demand letter may be the practical approach.

Step 5: Send a written DV claim demand to the at-fault insurer

Contact the at-fault driver's insurance company — not your own insurer — and state the intent to file a diminished value claim. Submit the claim in writing with supporting documentation:

- The final repair order from the body shop

- Documentation of pre-accident market value (KBB/NADA printouts and comparable listings)

- The independent DV appraisal report

- The claim amount requested

Keep all written correspondence. Verbal discussions aren't documentation.

Step 6: Negotiate or invoke the appraisal clause

The insurer's first offer is frequently lower than the appraisal report value. Negotiation at this stage is standard. Counter with the independent appraisal report as your evidence base.

If negotiation stalls, most auto insurance policies include an appraisal clause — a binding dispute resolution mechanism that allows either party to demand independent appraisals. Each party selects an appraiser; if they can't agree, an umpire makes the final determination. Invoking the appraisal clause bypasses the standard claim negotiation process and often produces faster resolution.

Step 7: Escalate if the claim is denied or undervalued

If the insurer denies the DV claim outright or the offered amount is unreasonably low, several escalation paths exist:

- File a complaint with the state Department of Insurance: Free, no attorney required. State DOI agencies have regulatory authority over insurer conduct, and a formal complaint often prompts reconsideration

- Small claims court: For claims under the state's small claims limit (typically $5,000 to $10,000), small claims court is accessible without an attorney

- Hire an attorney specializing in insurance disputes or personal injury: Attorneys typically work on contingency for DV claims, meaning no upfront cost. The potential recovery justifies attorney involvement for claims above $2,000 to $3,000

For related dispute strategies, see insurance adjuster tactics to watch for and what to do when your insurance estimate is too low.

How much is a diminished value claim worth?

The amount of diminished value after an accident depends on several interconnected factors. DV amounts vary widely — here are the variables that matter most:

Vehicle market value before the accident: This is the dominant factor. A $15,000 vehicle losing 12% of its value produces a $1,800 DV claim. A $55,000 vehicle losing 15% produces an $8,250 claim.

Damage severity: Structural damage involving the frame, ADAS sensor mounts, or airbag deployment produces higher DV. Cosmetic-only damage — surface scratches, a single panel — produces lower DV.

Vehicle type and brand: Luxury vehicles (BMW, Mercedes-Benz, Audi, Lexus) typically see higher percentage DV losses — in the 15–25% range — because their buyers are more selective about vehicle history. Research shows average DV loss by vehicle segment: luxury vehicles approximately 23%, trucks approximately 21%, SUVs approximately 20%, standard sedans approximately 10–15%.

Vehicle age and mileage: Newer vehicles with lower mileage sustain larger percentage losses. A 1-year-old vehicle loses a greater fraction of its remaining value to an accident entry than a 7-year-old vehicle.

Local resale market: Markets with higher used-car demand and pricing (major metros, states with higher new-car prices) produce larger absolute DV amounts.

Repair quality and parts: OEM parts and documented quality repair cut repair-related DV and support a higher post-repair value, narrowing the gap to inherent DV only.

As a practical range: minor damage on a standard vehicle typically produces DV of $500 to $1,500. Moderate-to-major damage on a newer, higher-value vehicle can produce DV of $2,000 to $8,000 or more. Vehicle-history-based DV losses are real losses — not speculative — and are reflected in actual resale pricing on the open market.

Vehicle history reports and the DV claim connection

The mechanism behind inherent DV is the vehicle history report. Carfax, AutoCheck, and similar services pull accident disclosures from police reports, insurer submissions, and DMV records. Any significant collision — any event reported to an insurer — is likely to appear.

A prospective private buyer reviewing a Carfax report for a vehicle with a prior accident will:

1. Use the accident history as leverage to negotiate a lower price

2. Walk away from the purchase if the accident was severe or if the seller won't discount

3. Factor the accident into a trade-in or dealer purchase price (dealers discount accident-history vehicles at auction)

This isn't theoretical. Dealerships applying trade-in valuations routinely apply a $500 to $2,500 discount for a prior accident entry, depending on severity and the vehicle's overall profile. Private buyers do the same.

A DV claim exists to compensate for this permanent market reality. A complete professional repair can't make a Carfax entry disappear. The at-fault driver's insurer is responsible for the full cost of making the non-fault party whole — and "whole" means the pre-accident value of the vehicle, not just the cost of the physical repairs.

Common reasons insurers deny diminished value claims — and how to respond

Insurance companies have financial incentive to pay as little as possible on DV claims. Knowing the most common denial tactics helps car owners respond effectively.

"Your policy doesn't cover diminished value": This is often true for first-party claims in most states — but it has no bearing on a third-party claim against the at-fault driver's insurer. The at-fault driver's liability coverage owes property damage compensation to the non-fault party, and that includes DV in virtually every state except Nebraska.

"The damage was minor / no diminished value occurred": Request documentation of how they calculated zero DV. If the vehicle had a repair of any meaningful scope, some inherent DV exists. Counter with the independent appraisal report.

"We use the 17c formula and that's the final number": The 17c formula is an internal insurer tool, not a legal standard. No statute requires its use. Counter with independent appraisal evidence showing actual market impact.

"The statute of limitations has passed": This is a legitimate defense if true. It underscores the importance of filing before the deadline — check the state's statute of limitations at the time of the accident.

Delaying without decision: Keep dated records of all communications. Unreasonable delay in responding to a filed claim may itself constitute bad faith in some states, providing grounds for a complaint to the state DOI.

For patterns in adjuster behavior across the claims process, see our guide to 7 insurance adjuster tactics to watch for.

Is a diminished value claim worth it?

For many car owners, yes — with qualifications.

Strong DV claim candidates: A vehicle less than 7 years old with under 80,000 miles, moderate to major damage, and a pre-accident market value above $15,000 is a strong candidate. Expected recovery in the $1,500 to $5,000+ range easily justifies the cost of an independent appraisal and the effort of filing.

Weaker candidates: A 2011 vehicle with 115,000 miles and $200 in cosmetic damage produces little or no meaningful DV and probably won't justify the filing effort, particularly if the expected recovery doesn't exceed the cost of an appraisal.

The cost-benefit calculation:

- Independent appraisal: $350–$650

- Filing and correspondence: several hours of the car owner's time

- Expected recovery: 10–25% of pre-accident value for strong candidates

- No attorney fee upfront (contingency arrangements typical)

Most car owners who file DV claims with proper documentation recover meaningful compensation. The ones who walk away with nothing are typically those who filed without documentation, filed against their own insurer in a state that doesn't allow first-party claims, or missed the statute of limitations.

The claim most car owners leave on the table is a legitimate one. It simply requires knowing it exists, documenting it properly, and not accepting the first number an insurer offers.

To understand how DV connects to the broader insurance claims process, including first-party vs. third-party claim distinctions that affect DV eligibility, see our guide to first-party vs. third-party insurance claims.

Key takeaways

- Diminished value is a real, recoverable financial loss — the reduction in a vehicle's market value from its accident history, permanent even after a complete professional repair

- Third-party DV claims are available in 49 states — only Nebraska and (practically) Michigan are exceptions; first-party claims are available in GA, KS, LA, and NC

- The 17c formula is an insurer tool, not a legal ceiling — independent appraisals consistently produce higher values and carry weight in negotiations and court

- An independent appraisal ($350–$650) is the single most important step — it provides documented evidence that transforms a DV claim from a number the insurer can dismiss to one they have to address

- Statute of limitations matters — most states give two to four years, but Louisiana allows only one year; file before the deadline

- Insurers frequently deny or undervalue DV claims — knowing the denial tactics and having documented counter-arguments changes the outcome

To find certified collision repair shops that document repairs properly — which directly supports a stronger DV claim — browse auto body shops near you or search collision repair services for shops with OEM certifications and documented repair quality.

Last updated: June 2026. Diminished value laws vary by state and are subject to change. This article provides general educational information, not legal advice. Consult your state's Department of Insurance or a licensed attorney for guidance specific to your situation.

Frequently asked questions about diminished value claims

What is a diminished value claim?

A diminished value claim is a request for compensation for the reduction in a vehicle's market value caused by its accident history, even after the vehicle has been fully repaired. A vehicle with an accident on its Carfax report sells for less than a comparable clean-history vehicle — that gap is recoverable through a DV claim in most states.

How much is my diminished value claim worth?

Typical DV amounts range from 10% to 25% of the vehicle's pre-accident market value, depending on vehicle age, mileage, damage severity, and the make/model. A $30,000 vehicle with moderate damage might produce a DV claim of $3,000 to $7,500. An independent appraisal provides the most accurate estimate.

Can I file a diminished value claim in my state?

Third-party diminished value claims — against the at-fault driver's insurer — are available in all states except Nebraska. Michigan limits recovery to $1,000 under mini-tort rules. First-party claims (against your own insurer) are available in Georgia, Kansas, Louisiana, and North Carolina.

How long do I have to file a diminished value claim?

Statutes of limitations vary by state. Most states allow two to four years from the accident date. Louisiana allows only one year. Georgia allows four years. Rhode Island allows up to ten years. Check the specific state law where the accident occurred.

Do I need a lawyer to file a diminished value claim?

Not necessarily. Many car owners successfully file DV claims without legal representation, particularly when they have an independent appraisal report. For larger claims (above $3,000 to $5,000) or when an insurer refuses to negotiate, an attorney specializing in insurance disputes can improve outcomes and typically works on contingency.

What is the 17c formula for diminished value?

The 17c formula is an insurance industry calculation method: pre-accident value × 10% × damage severity multiplier × mileage multiplier. It frequently undervalues real-world DV losses because it caps the base at 10% of vehicle value regardless of actual damage. An independent appraisal using market comparables typically produces a more accurate and higher figure.