When insurance totals your car, most owners face the same immediate question: are my rights protected here, and is this offer fair? The call itself is jarring — the adjuster declares a total loss, a settlement offer follows, and suddenly the clock is ticking.

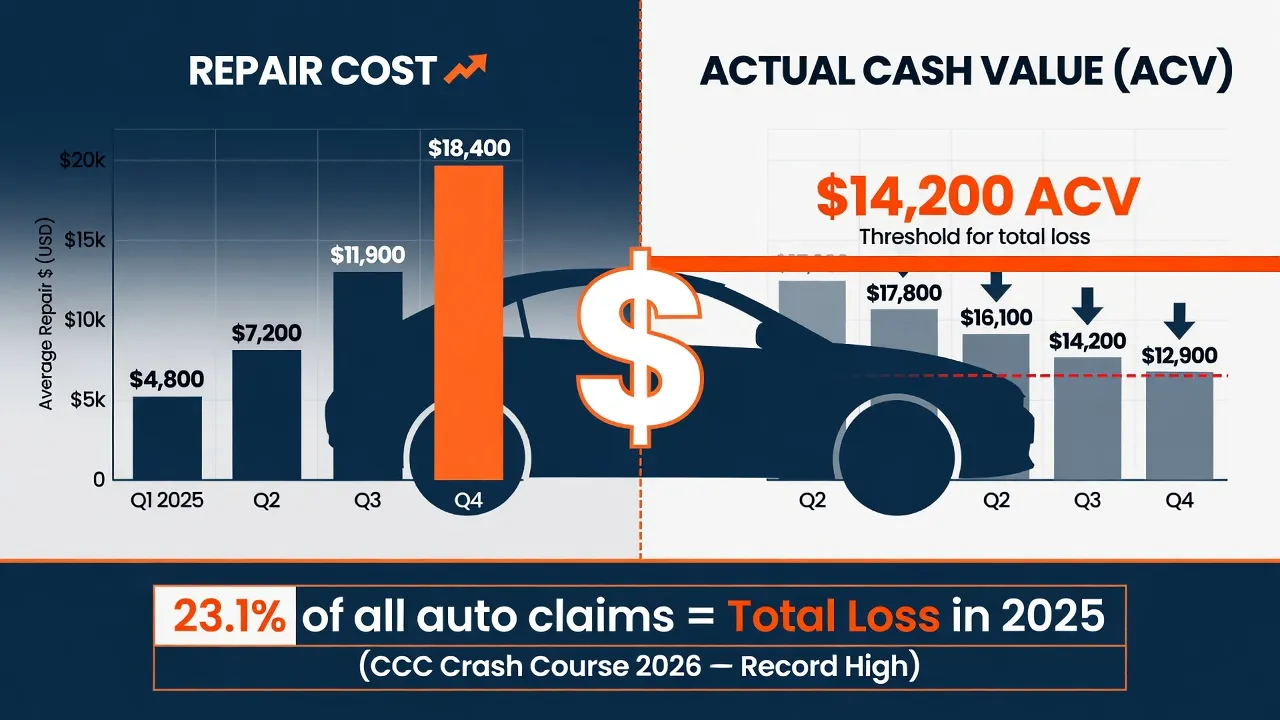

Most car owners accept that first offer without question. Not because it's fair, but because the whole situation feels overwhelming and they don't know they have options. According to CCC Crash Course 2026 data, 23.1% of all auto insurance claims resulted in a total loss in 2025 — a record high. That means roughly one in four collision claims ends with the insurance company writing a check instead of authorizing a repair.

What happens next is more within your control than most owners realize. Understanding total loss car insurance rights — the right to dispute the settlement, keep the vehicle, or invoke a binding appraisal process — is what separates car owners who recover fair value from those who leave money on the table. The settlement offer isn't final. The valuation method isn't infallible.

This guide covers how total loss is determined, how to evaluate and challenge the settlement offer, what gap insurance means for your situation, and what your options are once the total loss decision is made. For a full walkthrough of the insurance claims process, see our complete auto body insurance claims guide for car owners.

Insurance regulations and total loss thresholds vary by state. This guide provides general information. Consult your state's Department of Insurance or a licensed professional for advice specific to your situation.

How insurance decides your car is a total loss — and when it's wrong

A total loss declaration is an economic decision, not a mechanical one. The vehicle doesn't have to be destroyed beyond recognition. It just has to cross the financial threshold where repair costs stop making sense relative to what the car is worth.

Insurance companies use one of two calculation methods, and which one applies depends on the state where the vehicle is registered.

Total Loss Threshold (TLT)

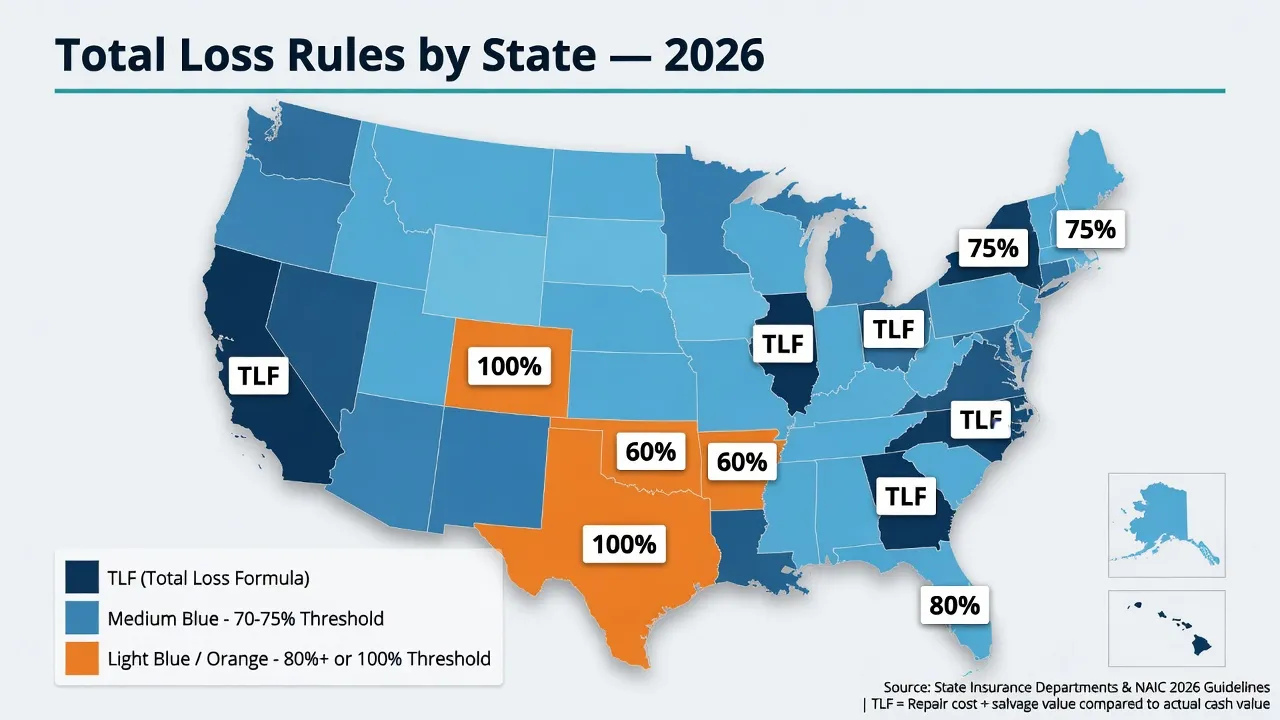

Most states use a percentage threshold. If the estimated repair cost equals or exceeds a set percentage of the vehicle's pre-accident Actual Cash Value (ACV), the vehicle is declared a total loss. These thresholds vary considerably by state — from 60% in Oklahoma to 100% in Texas, Colorado, and several other states.

Total Loss Formula (TLF)

About 16 states use a formula instead of a fixed percentage. Under the TLF approach: if repair cost + salvage value ≥ ACV, the vehicle is totaled. States using the TLF include California, Georgia, Illinois, New Jersey, Ohio, Pennsylvania, and Washington, among others.

The practical difference: TLF states may total a vehicle at a lower repair-cost threshold than TLT states if the salvage value is high, because salvage value counts in the equation.

Total loss threshold by state — 2026 reference table

The total loss threshold by state ranges from 60% to 100% of ACV. States using the Total Loss Formula (TLF) don't publish a fixed percentage — instead, the salvage value determines when the threshold is crossed. The table below covers the ten highest-traffic states.

| State | Method | Threshold |

|---|---|---|

| California | TLF | Repair + salvage ≥ ACV |

| Florida | Percentage | 80% of ACV |

| Texas | Percentage | 100% of ACV |

| New York | Percentage | 75% of ACV |

| Illinois | TLF | Repair + salvage ≥ ACV |

| Georgia | TLF | Repair + salvage ≥ ACV |

| Pennsylvania | TLF | Repair + salvage ≥ ACV |

| Oklahoma | Percentage | 60% of ACV |

| Colorado | Percentage | 100% of ACV |

| Ohio | TLF | Repair + salvage ≥ ACV |

Note: Total loss thresholds are subject to legislative change. Verify current rules with your state's Department of Insurance. A full list of total loss thresholds by state is available from SoFi's consumer research database.

Why 23.1% of claims are now total losses

The record total loss rate in 2025 reflects two converging trends. Repair costs have climbed sharply — the average collision repair now costs $4,818 according to the CCC Crash Course 2026 industry report, driven by ADAS sensor calibrations, advanced materials, and supply chain pressure on parts pricing. At the same time, used vehicle values have fluctuated, with some models losing value faster than expected. When repair costs are high and vehicle values are moderate, more claims cross the total loss threshold.

How actual cash value (ACV) is calculated in a total loss claim

Actual Cash Value (ACV) is the insurer's determination of what the vehicle was worth immediately before the accident. It's not the purchase price, not the loan balance, not the replacement cost of a new vehicle. It's the market value of the specific car, in its specific condition, in its specific geographic market, the day before the damage happened.

Insurers calculate ACV using proprietary valuation software — tools from companies like Mitchell, CCC ONE, and Audatex — that pull comparable vehicle sales data from the local market and apply condition adjustments. The valuation report considers:

- Year, make, model, and trim level

- Mileage at the time of the accident

- Pre-accident condition (exterior, interior, mechanical)

- Recent comparable vehicles listed or sold in the local market

- Geographic adjustments for regional market differences

Why the ACV often feels low

Valuation software tools aren't perfect, and insurers' primary financial interest is in settling claims at the lowest defensible number. Common issues that cause ACV underestimation include:

- Condition adjustments that don't reflect reality: Software may apply standard condition deductions that don't account for a well-maintained vehicle's actual state

- Stale or mismatched comparables: The system may pull comparables from vehicles with higher mileage, lower trim, or different options

- Recent maintenance and upgrades ignored: New tires, a recent transmission service, or a new battery add to market value but often won't appear in the initial valuation

- Regional market timing: In markets with strong demand for specific models, software may lag current pricing

The insurer is required to provide a total loss valuation report explaining how they calculated the ACV. Request this document before deciding whether to accept or dispute the offer.

Your total loss car insurance rights: how to dispute the ACV settlement

The first settlement offer is a starting point, not a final number. Car owners who push back with documented evidence frequently recover additional compensation. Successful ACV disputes — based on insurance negotiation data — run from $500 to $2,500 or more, depending on the vehicle's value and how well the dispute is documented.

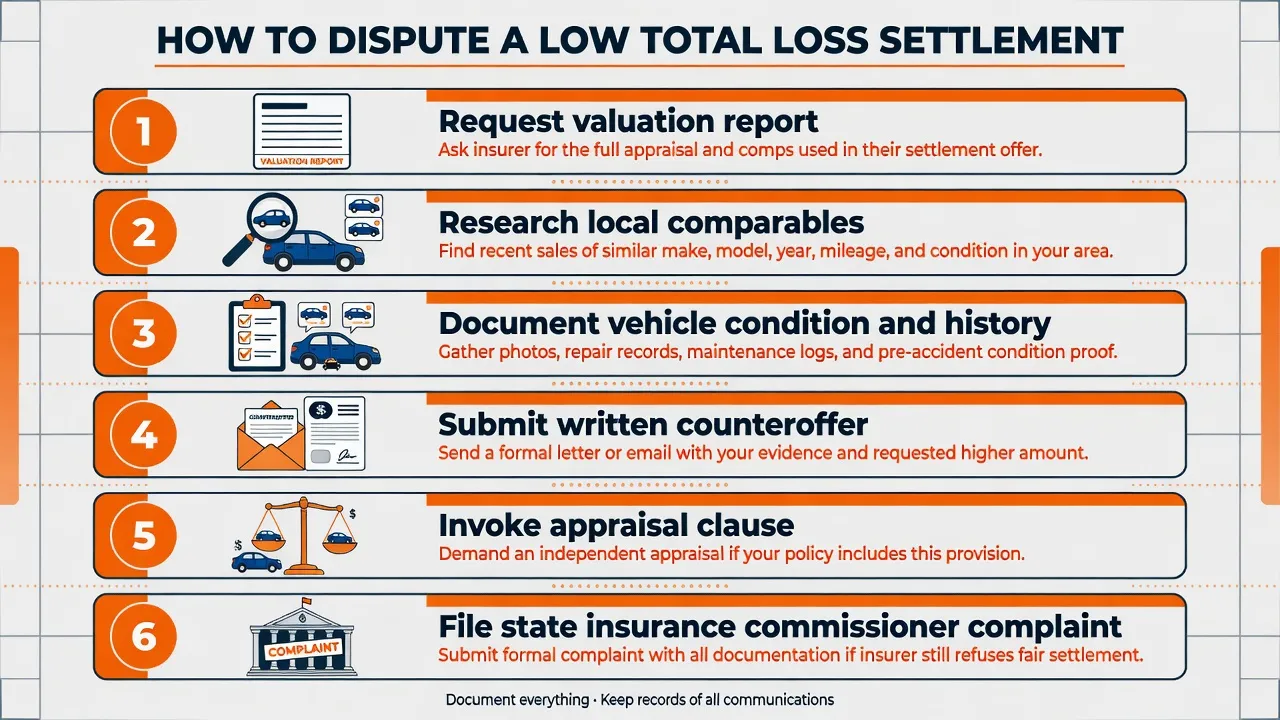

How to dispute a total loss settlement: (1) Request the insurer's valuation report. (2) Research local comparable listings on AutoTrader, Cars.com, and KBB. (3) Document vehicle condition and maintenance history. (4) Submit a written counteroffer with evidence. (5) Invoke the appraisal clause if negotiations stall. (6) File a complaint with the state insurance commissioner.

Step 1: Request the total loss valuation report

Before anything else, ask the insurer for the valuation report in writing. This document shows the specific comparables used, the condition adjustments applied, and the formula that produced the ACV figure. Errors in this report are the basis for a successful dispute.

Step 2: Research comparable vehicles yourself

Search for vehicles matching your year, make, model, trim level, mileage range, and condition on AutoTrader, Cars.com, and KBB. Focus on listings in your local market — within 50 to 100 miles if possible. Print or screenshot at least five to seven listings showing asking prices.

Find comparables the insurer's software missed or underweighted. If current listings consistently show higher prices than the insurer's figure, that's your evidence.

Step 3: Document your vehicle's condition and history

Gather records that support a higher valuation: service records showing consistent maintenance, receipts for recent repairs or upgrades (new tires, battery, brakes, audio system), pre-accident photos showing condition, and documentation of low-mileage use or garage storage.

Step 4: Submit a written counteroffer

A phone call isn't enough. Submit your dispute in writing — email or certified letter — with your evidence attached. Specify the ACV you believe is accurate and explain the basis. A written record signals seriousness and creates documentation if the dispute needs to escalate.

Step 5: Invoke the appraisal clause

Every standard auto insurance policy includes an appraisal clause — a binding dispute resolution mechanism. Each party retains an independent appraiser. The two appraisers attempt to agree on value. If they can't, they appoint a neutral umpire whose decision is binding on both parties.

Invoking the appraisal clause is more formal and slower, but it bypasses the negotiation process entirely when adjuster conversations stall.

Step 6: File a complaint with the state insurance commissioner

State Departments of Insurance handle complaints against insurers and carry regulatory authority. Filing a formal complaint — free, no attorney required — often prompts an insurer to reconsider a disputed valuation rather than face regulatory review. Find your state's complaint process through the National Association of Insurance Commissioners (NAIC) consumer complaint portal.

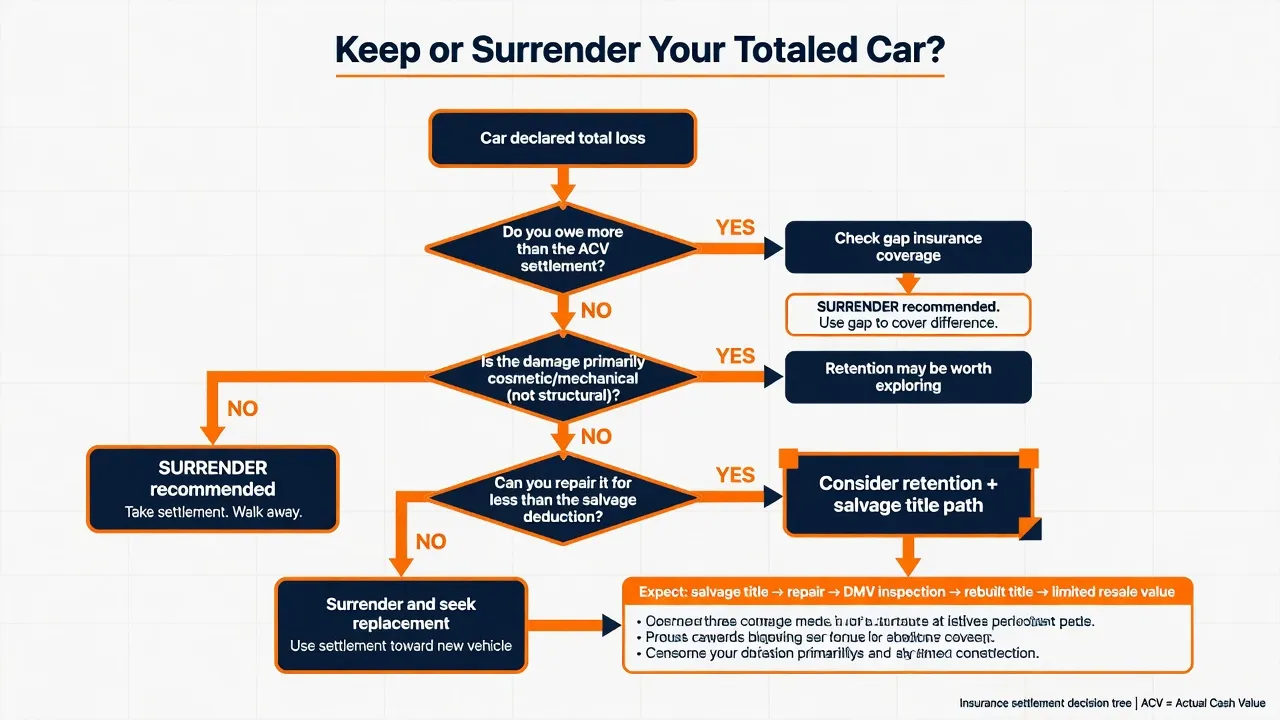

Gap insurance and total loss: when the settlement doesn't cover what you owe

If the vehicle was financed or leased and was purchased within the last two to three years, there's a real chance the ACV settlement is less than the remaining loan balance. This situation — called being "upside down" or "underwater" on the loan — leaves the car owner responsible for paying the difference out of pocket.

Gap insurance (Guaranteed Asset Protection) bridges the difference between the ACV settlement and the outstanding loan or lease balance. If a car was purchased for $32,000, the loan balance is $24,000, and the ACV settlement is $19,500 — gap insurance covers the $4,500 shortfall.

Gap coverage is offered by the financing dealer or lender at purchase, but it can also be added through some auto insurance policies as an endorsement. Before accepting any total loss settlement, check whether gap insurance is active on the vehicle.

Gap insurance doesn't cover the deductible, which the car owner is still responsible for.

Can you keep a totaled car? Salvage title, rebuilt title, and what to expect

Yes, in most states, car owners can retain a vehicle declared a total loss. Here's how it works:

- Notify the insurer that you want to retain the vehicle

- The insurer deducts the salvage value from the ACV settlement

- You receive the reduced payout (ACV minus deductible minus salvage value)

- The vehicle receives a salvage title from the state DMV

A salvage title means the vehicle was declared a total loss and hasn't been inspected for roadworthiness after the damage. A salvage-titled vehicle can't be legally driven on public roads until it passes a state inspection and receives a rebuilt title (also called a reconstructed title).

When retaining makes sense — and when it doesn't

Keeping a totaled vehicle can make financial sense when:

- The owner has the skill and resources to repair it at a lower cost than the salvage deduction

- The vehicle has sentimental value

- The owner plans to use it for parts

- The repair cost is close to the total loss threshold and the vehicle can be restored to operational condition

Retaining makes less sense when:

- The vehicle has significant structural or frame damage — costs to restore a unibody or frame to safe operating condition often exceed the salvage value benefit

- The owner needs financing to repair it — salvage-titled vehicles are hard to finance

- The vehicle has ADAS systems that require calibration — salvage and rebuilt-title inspection requirements vary by state

- Future resale is a priority — rebuilt-title vehicles carry a permanent disclosure requirement and sell for 20–40% less than clean-title equivalents

The diminished value connection

One area many car owners overlook after a total loss decision is diminished value — specifically as it relates to the ACV dispute. If the total loss determination hinges on whether the car should have been repaired instead of totaled, the diminished value of a repaired vehicle is relevant context for the dispute.

For car owners whose vehicle is repaired (not totaled) and who want to recover the resale value loss from the accident history, a separate diminished value claim may apply. For a full guide on this topic, see our article on how to file a diminished value claim.

If the total loss determination is being contested and the accident was another driver's fault, the right to file a third-party claim against the at-fault driver's insurer affects your options — including the path to a diminished value claim. See first-party vs. third-party insurance claims for how these distinctions affect total loss and diminished value rights.

When to accept the total loss settlement vs. when to dispute it

Not every total loss dispute is worth pursuing. Whether to push back on the settlement depends on several practical factors.

Signs the offer warrants a dispute:

- The ACV is more than 10–15% below comparable vehicles currently listed in the local market

- The valuation report contains errors — wrong trim level, incorrect mileage, outdated or mismatched comparables

- Recent maintenance, upgrades, or documented above-average condition weren't accounted for

- The vehicle is a high-demand model with premiums above typical book value in the local market

Signs the offer is reasonable:

- Comparable listings align with the insurer's ACV figure

- The valuation report accurately reflects the vehicle's trim, mileage, and condition

- The gap between the offer and market value is small relative to the time and effort to dispute

A counter-offer adds 7 to 21 days to the settlement timeline. For most disputes, the outcome lands between $500 and $2,500 in additional payout — worth a few hours of documentation work for most car owners.

Total loss ACV disputes are one of several areas where adjusters apply pressure tactics. For a full breakdown of how adjusters structure these negotiations — and specific counter-moves for each tactic — see our guide to insurance adjuster tactics to watch for.

State total loss thresholds also affect how much leverage car owners have. Texas uses a 100% ACV threshold, meaning the insurer can only total a vehicle if repair costs equal or exceed its full pre-accident value. Car owners in Texas who believe their vehicle was improperly totaled have a strong basis for dispute. Find auto body shops in Texas to locate shops experienced with the state's total loss rules.

Key takeaways: insurance totaled my car — your rights at every step

The total loss process feels final when the adjuster delivers the decision. It isn't. Car owners have real rights and options at every step.

- The settlement offer is a starting point: The first ACV figure isn't final. Documented evidence of higher comparable values frequently results in a revised offer.

- Request the valuation report: The insurer is required to show how the ACV was calculated. Errors in comparables, condition, or trim are the basis for successful disputes.

- Know your state's total loss method: Whether your state uses a percentage threshold or the Total Loss Formula affects when and how total loss is calculated.

- Check gap insurance before accepting: If the loan balance exceeds the settlement offer, gap insurance coverage is critical to check before signing anything.

- Retention is an option with real tradeoffs: Keeping a totaled vehicle is possible in most states, but salvage and rebuilt title implications affect future insurance, financing, and resale value.

- The appraisal clause exists for disputed valuations: If adjuster negotiations stall, the policy's appraisal clause provides a binding resolution path that cuts through back-and-forth.

For a full guide to the insurance claims process from accident through final payout, see the complete auto body insurance claims guide for car owners. If the low settlement reflects a broader pattern of adjuster pressure tactics, see insurance adjuster tactics to watch for for a full breakdown.

To find experienced collision repair shops near you — shops that understand total loss documentation, supplement disputes, and how to advocate for the vehicle owner — browse by location.

Last updated: June 2026. Total loss thresholds and consumer protections vary by state and are subject to legislative change. Consult your state's Department of Insurance or a licensed insurance professional for advice specific to your situation.

Frequently asked questions about total loss car insurance rights

When is a car considered totaled?

A car is considered totaled when repair costs exceed the insurer's threshold — either a fixed percentage of the vehicle's Actual Cash Value (ACV), around 70–80% in most states, or the Total Loss Formula (repair cost + salvage value ≥ ACV). Thresholds range from 60% in Oklahoma to 100% in Texas and Colorado. The determination is economic, not mechanical — the vehicle doesn't need to be destroyed.

How is actual cash value calculated for a total loss?

Insurers calculate ACV using valuation software that pulls comparable vehicle sales in the local market, then adjusts for the vehicle's year, make, model, trim, mileage, and pre-accident condition. The result represents what the vehicle was worth immediately before the accident — not its purchase price or replacement cost.

Can I dispute the insurance company's total loss settlement?

Yes. Car owners can dispute the ACV determination by requesting the insurer's valuation report, researching comparable local listings, submitting a written counteroffer with documentation, and invoking the policy's appraisal clause for a binding independent appraisal if negotiations stall.

What happens if my loan balance is more than the total loss settlement?

If the ACV settlement is less than the outstanding loan balance, the car owner is responsible for the difference unless gap insurance is active. Gap insurance covers the shortfall between the ACV payout and the loan balance. Check financing documents or the insurance policy declarations page to confirm gap coverage.

Can I keep my totaled car?

Yes, in most states. The insurer deducts the salvage value from the ACV settlement and the vehicle gets a salvage title. To legally drive the car again, it must be repaired, pass a DMV inspection, and receive a rebuilt title. Salvage- and rebuilt-title vehicles are harder to insure for full coverage and sell at a discount to clean-title equivalents.

Sources: CCC Crash Course 2026 (cccis.com); Washington State Office of the Insurance Commissioner (insurance.wa.gov); SoFi — Total Loss Thresholds by State (sofi.com); National Association of Insurance Commissioners (naic.org); Insurance Information Institute (iii.org)