After a collision, one of the first decisions a car owner faces is deceptively simple on the surface: whose insurance company do you call? Whether to file a first-party vs. third-party insurance claim — with your own insurer or the other driver's — carries real financial consequences that most car owners don't fully understand until they're already mid-process.

The two options share the same end goal — getting the car repaired — but the paths differ in deductible cost, processing speed, premium impact, and eligibility for diminished value recovery.

Most car owners face this decision only two or three times in their lives, under stress, often within hours of an accident. Understanding whether to file a claim with your own insurance or the at-fault driver's before that moment arrives makes the decision manageable — and prevents costly mistakes.

This guide explains exactly what each claim type means, how the core tradeoffs work, and what factors should drive the decision for any given accident scenario. For a complete walkthrough of the full auto body claims process, see the complete auto body insurance claims guide.

Insurance processes and consumer rights vary by state. Consult your specific policy and your state's Department of Insurance for details.

What is a first-party insurance claim?

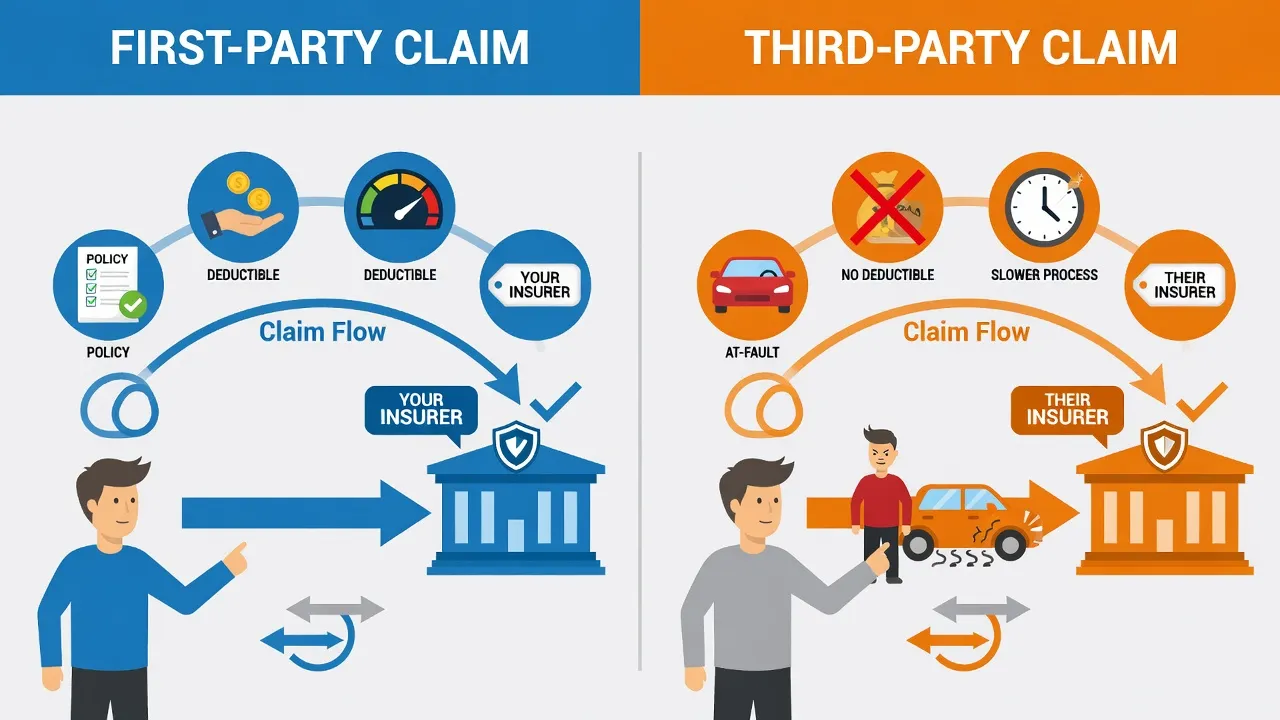

A first-party insurance claim is filed with your own insurance company — the one whose premium you pay — under a policy you already hold. "First party" refers to you, the policyholder. Your insurer is the second party. The term means you're making a claim against your own coverage.

First-party claims apply regardless of who caused the accident. A driver who rear-ends another vehicle and files with their own insurer is making a first-party claim. So is a driver whose parked car was hit by an unknown vehicle. Even drivers who weren't at fault at all can choose to file first-party claims.

The most common first-party auto coverage types involved in collision repair are:

- Collision coverage — Pays for damage to your vehicle from a collision with another vehicle or object, regardless of fault

- Comprehensive coverage — Pays for non-collision damage (hail, flooding, fire, vandalism, theft)

- Uninsured/underinsured motorist property damage (UM/UIM) — Covers damage when the at-fault driver has no insurance or insufficient insurance

- Personal Injury Protection (PIP) — Covers medical expenses in no-fault states (more on this below)

Both collision and comprehensive coverage are subject to a deductible, the amount you pay out of pocket before the insurance company covers the remainder.

What is a third-party insurance claim?

A third-party insurance claim is filed against another person's insurance policy — specifically, the at-fault driver's liability coverage. In this scenario, you're the "third party": the person harmed by someone else's actions who is seeking compensation from their insurer.

Third-party claims for property damage work through the at-fault driver's property damage liability (PDL) coverage. That coverage exists to compensate people the policyholder harms. You're filing against their insurer to recover repair costs for your vehicle.

The key distinction: in a third-party claim, you have no direct contractual relationship with the insurer you're filing against. They owe you fair consideration, but their primary obligation runs to their policyholder — not to you.

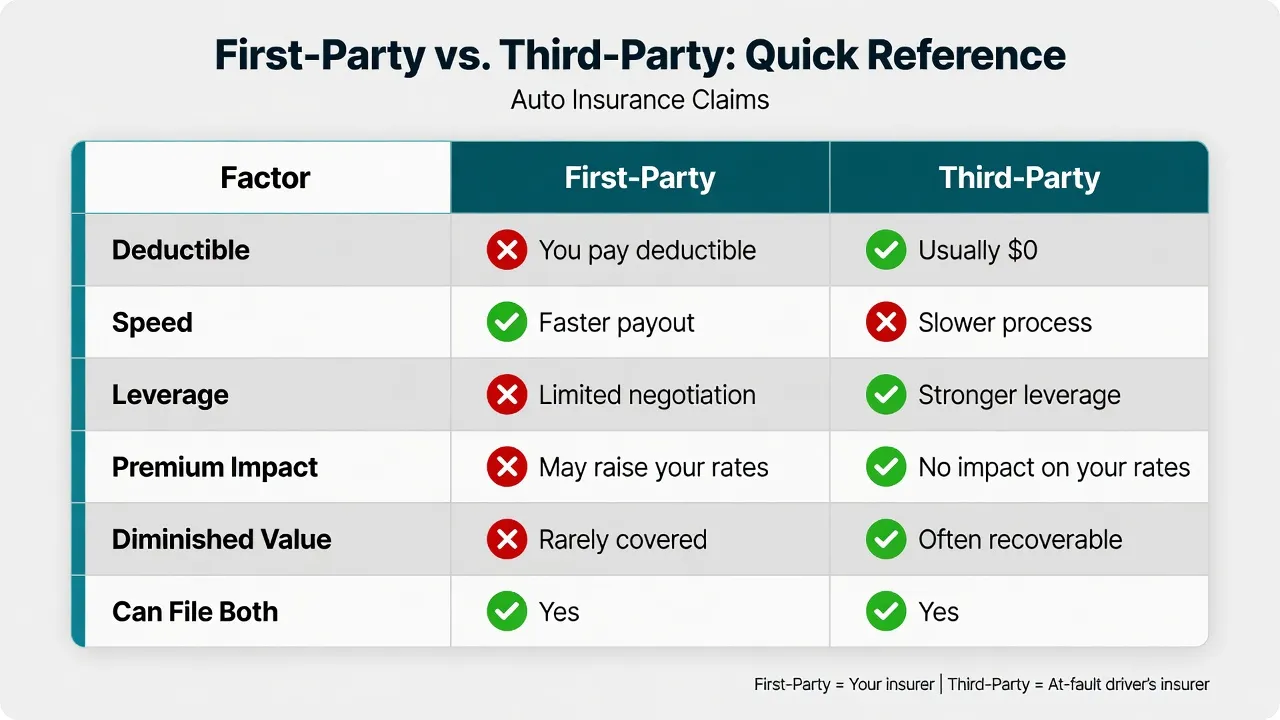

Key differences: first-party vs. third-party claims

The choice between these two paths has real financial and practical consequences once collision repair gets underway. Here are the six factors that matter most:

1. Deductible

This is often the deciding factor for cost-conscious car owners.

First-party claim: The deductible applies. If the collision coverage has a $500 deductible and the repair costs $3,000, the car owner pays $500 and the insurer pays $2,500. The deductible is paid to the body shop upon completion of repairs, not to the insurance company.

Third-party claim: No deductible. When the at-fault driver's insurer accepts liability, they cover the full approved repair cost. The car owner pays nothing out of pocket (assuming the repair stays within approved amounts).

For drivers with high deductibles — CCC Crash Course 2026 data shows 26% of insured drivers now carry deductibles of $1,000 or more — this single factor often tips the decision toward pursuing a third-party claim when another driver was clearly at fault.

2. Processing speed

First-party claim: Generally faster. The insurance company already has the policyholder's vehicle information, driving history, and policy details on file. The insurer also carries a legal duty under contract law and state insurance regulations to process the claim promptly. Most first-party claims receive initial approval within three to five business days.

Third-party claim: Can be slower. The at-fault driver's insurer needs to investigate the accident, confirm liability, and often conduct their own inspection before approving repairs. This process can take days, weeks, or longer if liability is disputed. If the at-fault driver contests fault, the car owner's repairs may be delayed for the duration of the dispute.

When a car owner needs transportation quickly and can't afford to wait, first-party processing speed is a real advantage. Rental car coverage also interacts with claim type — third-party claims entitle the car owner to a rental from the at-fault driver's insurer, while first-party rental depends on whether rental reimbursement coverage is included in the policy. See our rental car coverage after an accident guide for a full breakdown of limits and gaps.

3. Control and leverage

First-party claim: The insurer has a contractual obligation to the policyholder. State insurance regulations require prompt, fair handling. If the insurer acts unreasonably — denying a valid claim, delaying without justification, or failing to investigate properly — the car owner has legal recourse through a bad faith claim. This legal protection doesn't exist in third-party claims.

Third-party claim: The at-fault driver's insurer owes nothing contractually to the car owner who's been harmed. They have every financial incentive to delay, dispute liability, or minimize the payout. Car owners have fewer immediate enforcement tools when dealing with another driver's insurer.

4. Premium impact

First-party claim: May affect future insurance premiums, depending on the carrier, the state, and the number of prior claims. Even when a car owner wasn't at fault in an accident, some insurers increase premiums after first-party claim filings. State laws vary on this — some prohibit premium increases for not-at-fault claims.

Third-party claim: Filing a claim against the at-fault driver's insurer doesn't affect the car owner's own premium. The claim is against the other policy, not the car owner's.

5. Diminished value eligibility

Diminished value (DV) refers to the reduction in a vehicle's resale market value after an accident, even when the car has been fully repaired. This is a real financial loss that car owners can often recover.

Third-party claim: The clearest path to a diminished value claim. When another driver was at fault, the car owner can file a DV claim against the at-fault driver's insurer to recover lost resale value. Most states support this for third-party claims.

First-party claim: Diminished value is much harder to recover from your own insurer. Most states don't allow first-party DV claims, or insurers deny them as a matter of policy. Michigan doesn't allow third-party DV claims at all; in all other states, third-party DV claims are legally available.

For a vehicle with real value — newer cars, low-mileage vehicles — the diminished value recovery potential can be substantial. Our guide to diminished value claims covers how to calculate and file a DV claim.

6. What happens when both claims are possible

Car owners are often surprised to learn they can file first-party and third-party claims simultaneously, or file first-party initially and pursue the third-party route later. Filing with your own insurer doesn't forfeit third-party rights.

This approach — file first-party to get the car repaired quickly, then pursue the at-fault driver's insurer for the deductible and diminished value — is common when the other driver's liability isn't immediately clear or is being contested.

The comparison table

First-party vs. third-party insurance claim — quick summary: A first-party claim is filed with your own insurer under your own policy; a deductible applies but processing is faster. A third-party claim is filed against the at-fault driver's insurer; no deductible is required, but processing is slower and your leverage is weaker.

| Factor | First-Party Claim | Third-Party Claim |

|---|---|---|

| Filed with | Your own insurer | At-fault driver's insurer |

| Deductible | Yes — you pay it | No deductible |

| Processing speed | Faster (3–5 days typical) | Slower (can take weeks) |

| Your leverage | Strong — contractual duty + bad faith law | Weaker — no contract with their insurer |

| Premium impact | Possible increase | No impact on your premiums |

| Diminished value | Difficult (most states deny) | Clearer path (all states except MI) |

| Works when at fault? | Yes | No |

| Works when not at fault? | Yes | Yes |

| Can you file both? | Yes | Yes |

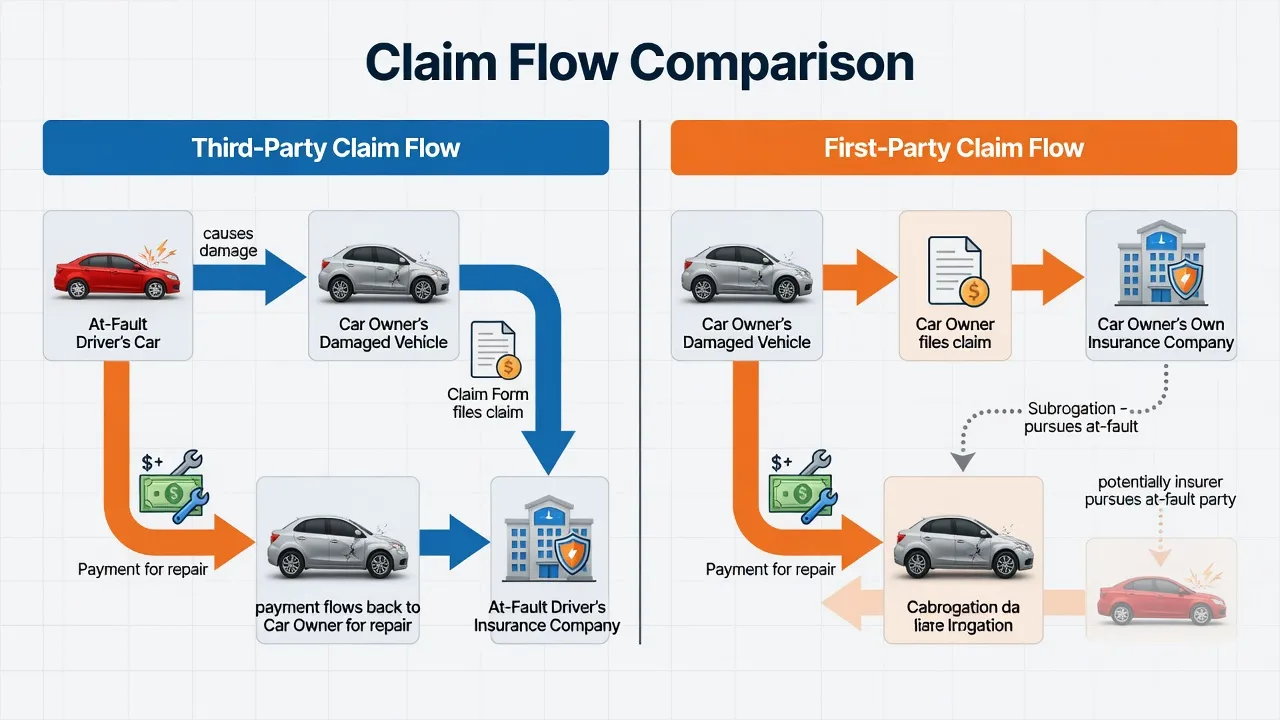

Subrogation: what happens after a first-party claim

Subrogation is the process by which your insurance company recovers the money it paid you from the party responsible for the accident. Understanding subrogation explains why filing a first-party claim doesn't mean permanently absorbing the loss when someone else was at fault.

Here's how it works in practice:

- Car owner files a first-party collision claim after being hit by an at-fault driver.

- The car owner's insurer pays for the repair (minus deductible).

- The car owner's insurer then pursues the at-fault driver's insurer directly to recover the amount paid.

- When subrogation succeeds, the car owner typically receives reimbursement of the deductible paid — sometimes months after the original repair.

Subrogation is handled insurer-to-insurer, without the car owner's active involvement in most cases. The timeline varies — from weeks to a year or more, depending on how readily the at-fault insurer accepts liability.

The upshot: first-party filing followed by subrogation can end up in the same financial outcome as a successful third-party claim — full repair coverage, deductible refunded — but with faster initial access to repairs.

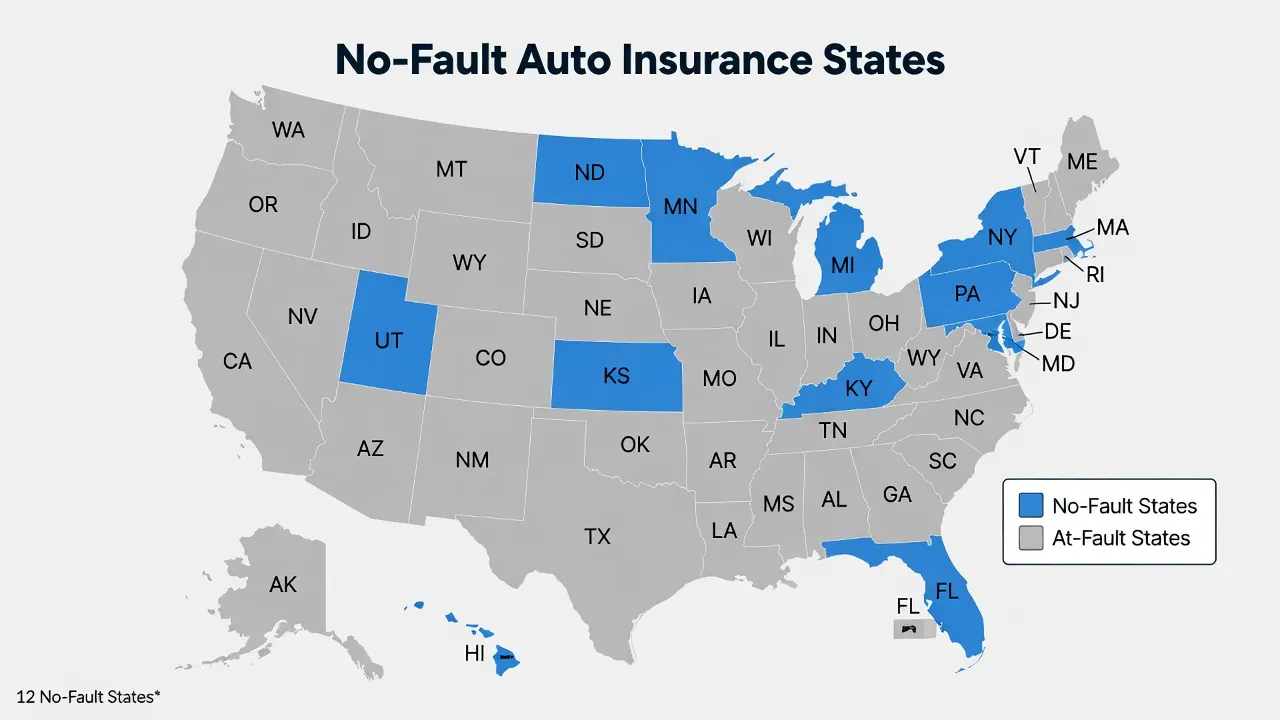

No-fault states: how the calculus changes

In 12 states, auto insurance operates under a no-fault system for medical claims:

- Florida

- Hawaii

- Kansas

- Kentucky

- Massachusetts

- Michigan

- Minnesota

- New Jersey

- New York

- North Dakota

- Pennsylvania

- Utah

In no-fault states, each driver files a claim with their own insurer regardless of who caused the accident. Personal Injury Protection (PIP) coverage pays for medical expenses and sometimes lost wages without requiring a fault determination first. This is a first-party claim by design.

One important point: "no-fault" applies to the medical/injury claim process. For property damage — the car repair itself — no-fault states still assess fault and still allow third-party property damage claims. Car owners in no-fault states can still choose between filing with their own collision coverage (first-party) or the at-fault driver's property damage liability (third-party) for repair costs. Drivers in Florida auto body shops, for example, deal with no-fault PIP for injuries but still use fault-based claims for vehicle repairs.

Kentucky, New Jersey, and Pennsylvania are "choice" no-fault states, where drivers can opt out of the no-fault system for injury claims when purchasing a policy.

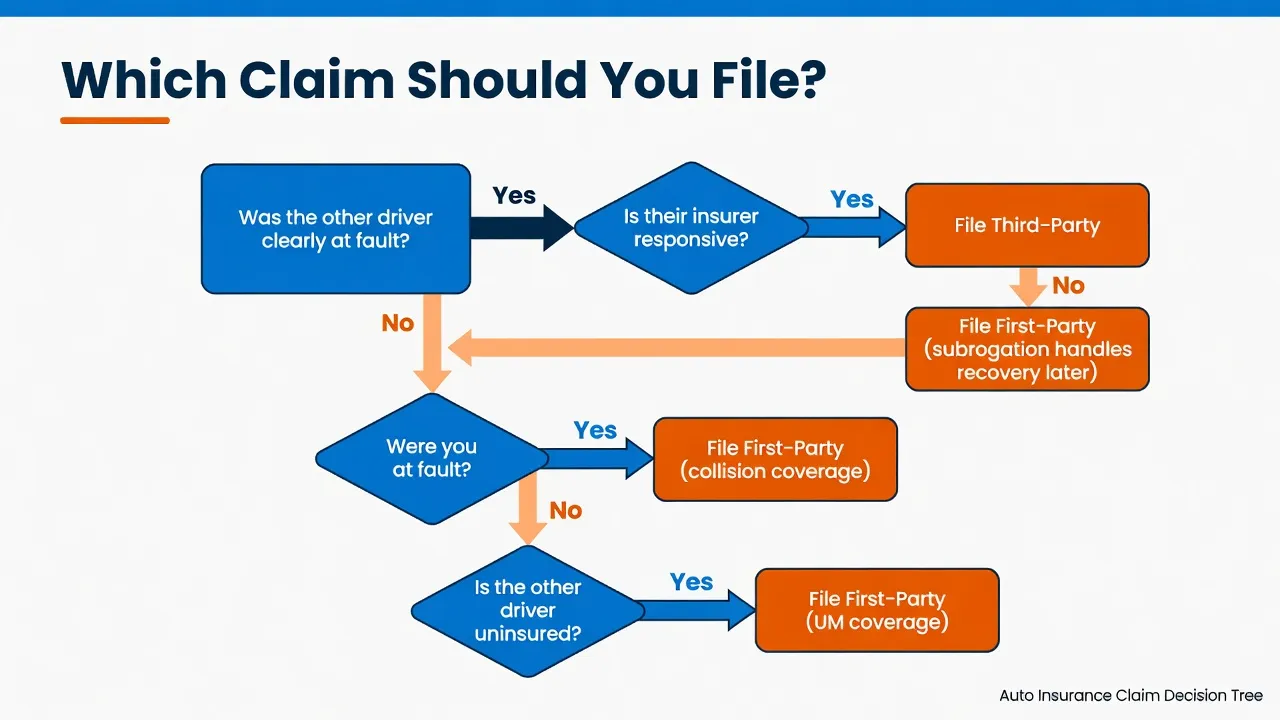

How to decide: should you file with your insurance or theirs?

The right choice depends on three factors specific to each accident: fault clarity, time urgency, and deductible amount.

When to file third-party (against their insurer)

- The other driver is clearly and undisputedly at fault

- There's a police report confirming fault

- The repair estimate is well above the deductible amount, making deductible avoidance worthwhile

- The vehicle has real resale value and a diminished value claim makes sense

- Time urgency is moderate (a few days to a week of processing time is acceptable)

When to file first-party (with your own insurer)

- Fault is unclear, shared, or disputed

- The other driver is uninsured or underinsured (UM/UIM coverage applies)

- The other driver's insurer is stonewalling or disputing liability

- The repair is urgently needed (rental car coverage running out, work transportation, etc.)

- The repair cost is close to the deductible anyway (making deductible avoidance less financially worthwhile)

- The car owner is at fault

When to file both

- Liability is uncertain and the car owner needs the vehicle repaired promptly

- The at-fault insurer is slow or unresponsive and first-party processing speeds things up

- The car owner wants the first-party insurer to handle subrogation on their behalf

Common scenarios explained

Scenario 1: Not at fault, clear liability, significant damage

A car owner is stopped at a red light and rear-ended. The other driver admits fault at the scene. Damage is estimated at $4,500. The car owner has a $500 deductible.

Best path: Third-party claim with the at-fault driver's insurer. No deductible, no premium impact, and a stronger diminished value claim if the vehicle has resale value. The risk is slower processing — if the at-fault insurer delays, file first-party and let the subrogation process run.

Scenario 2: Fault disputed, both drivers damaged

Two drivers have conflicting accounts. Both file with their respective insurers. Each insurer conducts an investigation. The final fault determination affects how subrogation resolves between the two carriers.

Best path: File first-party immediately to get the car repaired. Let insurers handle the fault investigation while repairs proceed.

Scenario 3: At fault, damage to own vehicle

The car owner backs into a pole. No other party involved.

Best path: First-party collision claim — it's the only option. Only the car owner's collision coverage applies.

Scenario 4: Uninsured at-fault driver

The other driver has no insurance.

Best path: Uninsured motorist property damage (UMPD) coverage under the car owner's own policy, if it's included. This is a first-party claim against the UM coverage. Some states require UMPD; others make it optional.

What to do when the at-fault driver's insurer delays

Dealing with an unresponsive third-party insurer is one of the most frustrating parts of the claims process. Unlike the car owner's own insurer, the at-fault driver's insurance company faces no direct contractual duty to the car owner. Delays are common.

When third-party processing stalls:

- File first-party simultaneously — get the repair started under the car owner's own collision coverage; subrogation handles recovery from the at-fault insurer later

- Document all communication — timestamps of calls, names of representatives, and written summaries of what was said

- Request a liability decision in writing — a written denial or acceptance forces the insurer's hand

- Contact the state insurance commissioner — third-party claim handling is regulated; unreasonable delays or bad faith tactics can be reported

- Consult an attorney — for large disputes, an attorney who handles insurance claims can communicate directly with the insurer

Our guide to insurance adjuster tactics covers the specific pressure tactics adjusters use in third-party claims — and the counter-moves that protect car owners.

Frequently asked questions

Does filing a first-party claim with my own insurer raise my rates even if I wasn't at fault?

Filing a first-party claim may raise rates depending on the state and the insurer — it's not guaranteed. Some states prohibit premium increases for not-at-fault claims; others allow it. Carriers vary as well — some increase premiums after any claim regardless of fault; others only after at-fault incidents. Before filing, ask the insurer directly whether a not-at-fault first-party claim affects the rate.

Can I get my deductible back if someone else was at fault?

Yes, through subrogation. When the car owner's insurer pays a collision claim and later establishes that another driver was at fault, the insurer pursues the at-fault driver's insurer for reimbursement. When subrogation succeeds, the car owner typically receives the deductible back. The timeline varies from a few weeks to over a year.

What if the at-fault driver's insurance coverage isn't enough to cover the repairs?

If the repair cost exceeds the at-fault driver's property damage liability limits, the car owner can pursue the remaining amount through underinsured motorist property damage (UIMPD) coverage on their own policy, small claims court against the at-fault driver personally, or negotiation with the at-fault driver. The right approach depends on the coverage limits, the repair cost, and the at-fault driver's financial situation.

Does choosing a body shop affect which type of claim I file?

No. Car owners have the legal right to choose any licensed repair facility regardless of which insurer handles the claim. The insurer — first-party or third-party — can't require the car owner to use a specific body shop. For more on this, see our complete auto body insurance claims guide.

How does a diminished value claim work with a first-party vs. third-party claim?

Third-party diminished value claims (against the at-fault driver's insurer) are available in all states except Michigan and are the cleaner path for recovering lost resale value. First-party DV claims — filed against your own insurer — are rarely approved and not recognized in most states. If recovering diminished value matters, pursuing a third-party claim or preserving the third-party option is important. Learn more about the process in our guide to diminished value claims.

Key takeaways

The first-party vs. third-party decision comes down to a few core tradeoffs: deductible cost, processing speed, and diminished value eligibility.

Five things worth knowing:

-

Third-party means no deductible — When the other driver was clearly at fault and their insurer accepts liability, there's no deductible to pay. That's a real cost difference for drivers carrying $500 or $1,000 deductibles.

-

First-party means faster repairs — The car owner's own insurer has a contractual duty to process promptly. When the vehicle needs to move quickly into repair, first-party is usually the faster route.

-

Diminished value favors third-party — For vehicles with real resale value, the ability to file a diminished value claim against the at-fault driver's insurer is a financial consideration worth taking seriously — and third-party is the cleaner legal path.

-

Both options can run simultaneously — Filing first-party doesn't surrender third-party rights. Subrogation often achieves the same financial outcome as a successful third-party claim, with the benefit of faster initial resolution.

-

No-fault states don't change the property damage equation — Even in no-fault states, car owners can still choose between first-party collision coverage and a third-party property damage claim for the vehicle repair itself.

When the full claims process is unfamiliar territory, understanding these fundamentals protects car owners from making decisions that cost money they didn't have to spend. For the complete step-by-step walkthrough — from accident documentation through final vehicle pickup — the auto body insurance claims guide for car owners covers every stage of the process.

Insurance requirements, PIP mandates, and consumer rights vary by state. Review your specific policy and consult your state Department of Insurance for details applicable to your situation.

Last updated: June 2026

Sources:

- CCC Information Services — CCC Crash Course 2026

- National Association of Public Insurance Adjusters — Consumer Resources

- Insurance Information Institute — No-Fault Auto Insurance

- crashrepairinfo.com — Your Rights as a Consumer