A collision drops the car off at a body shop on a Monday. A week passes. Then two. The repair turns out to be more involved than anyone expected — there's hidden damage behind the bumper, an ADAS calibration is required, and a part is on backorder. The car comes back on day 31.

The rental car bill arrives: $1,240. The insurance policy covers $900 maximum. The remaining $340 belongs to the car owner — a surprise that a ten-minute policy review before the repair began would have prevented.

Rental car coverage after an accident is one of the most misunderstood parts of the insurance claims process. Most car owners assume it comes with their policy automatically. Many don't know their daily limits until they've exceeded them. And almost none know what to do when the repair runs longer than the coverage allows.

This guide covers how rental reimbursement coverage works, what it pays for, when the at-fault driver's insurer owes the rental instead of yours, and how to protect yourself when repairs drag on. For a complete walkthrough of the full claims process, see our auto body insurance claims: complete consumer guide.

Rental reimbursement is not automatic — it's a separate add-on

What is rental reimbursement coverage? Rental reimbursement coverage, also called transportation expense coverage, is an optional add-on to an auto insurance policy that pays for a rental vehicle while a damaged car is being repaired after a covered claim. It's not included in standard collision or comprehensive coverage. Common limits range from $30 to $50 per day with a per-claim maximum of $900 to $1,500.

Here's the most important thing to understand upfront: rental reimbursement coverage is optional. It doesn't come standard with a basic auto insurance policy, even one that includes collision and comprehensive coverage.

Rental reimbursement — sometimes called "transportation expense coverage" — is an endorsement that must be specifically added to a policy. It covers the cost of a rental vehicle while a damaged car is being repaired after a covered insurance claim. The word "covered" matters: the repair must stem from a claim the policy recognizes, such as a collision or a comprehensive-covered event like hail damage or vandalism. Mechanical breakdowns, routine maintenance, and wear-and-tear repairs don't qualify.

Before filing a claim and arranging a rental, car owners should confirm three things by checking their policy declarations page or calling the insurer directly:

- Is rental reimbursement coverage included on the policy?

- What is the daily limit?

- What is the per-claim maximum?

If the answers are "yes, $40/day, and $1,200 maximum," the math is simple: coverage lasts 30 days at the daily rate. Costs above either limit — the daily cap or the total cap — become the car owner's responsibility.

What rental reimbursement typically covers (and what it doesn't)

What is covered

Rental reimbursement covers the base daily rate for a standard rental vehicle — typically a compact, midsize sedan, or similar — while the insured vehicle is undergoing repairs from a covered claim. Coverage begins the day repairs start and continues until the car is returned, up to the policy limits.

Some policies extend rental reimbursement to alternative transportation: rideshare fares, public transit costs, or taxi rides. This broader framing is why many insurers call the coverage "transportation expense coverage" rather than rental reimbursement specifically. Car owners who don't need or want a rental vehicle can sometimes apply the reimbursement allowance to alternative transport instead.

What is not covered

The following are almost universally excluded from rental reimbursement:

- Fuel costs: Car owners pay for gas themselves

- Rental company damage waivers: The collision damage waiver (CDW) or loss damage waiver (LDW) offered at the rental counter is the car owner's decision and expense

- Luxury or full-size SUV upgrades: Most policies cover only standard rental rates; upgrading to a larger or premium vehicle creates a daily cost gap

- Mechanical breakdown repairs: If the car is in the shop for a non-covered repair, rental reimbursement doesn't apply

- Costs after the policy limit is reached: Whether by daily or total limit, expenses above the cap are out-of-pocket

How daily and total rental car coverage limits work in practice

Most rental reimbursement policies set two limits: a daily rate and a per-claim maximum. Common tiers as of 2026 include:

| Daily Limit | Per-Claim Maximum | Days Covered |

|---|---|---|

| $30/day | $900 total | 30 days |

| $40/day | $1,200 total | 30 days |

| $50/day | $1,500 total | 30 days |

Actual rental costs for a midsize vehicle vary widely by market. In major metro areas — Los Angeles, New York, Miami, Chicago — daily rates frequently run $60 to $100 or more during peak periods. A policy with a $30/day limit in a high-cost market leaves a car owner paying $30 to $70 per day out of pocket from day one.

Car owners in high-cost markets, or those driving newer vehicles with complex ADAS systems, should consider higher daily limits. The premium difference between a $30/day and a $50/day endorsement is typically just $2 to $5 per month.

When the at-fault driver's insurer covers the rental instead

Not every rental during a repair gets billed to the car owner's own policy. When another driver caused the accident, a third-party claim applies, and the at-fault driver's liability coverage typically includes compensation for the other party's loss of vehicle use.

Insurers don't always volunteer this distinction:

- In a first-party claim (filing with your own insurer), rental coverage comes from your rental reimbursement endorsement. If you don't have it, you pay out of pocket.

- In a third-party claim (filing with the at-fault driver's insurer), the at-fault driver's liability coverage typically owes you compensation for transportation while your vehicle is being repaired — even if your own policy has no rental reimbursement at all.

This third-party rental right exists because liability coverage is designed to make the injured party "whole" — restored to roughly the same position they were in before the accident. Being without a vehicle while it's in the shop is a direct, compensable consequence of the collision. Car owners can review their state-specific rights at crashrepairinfo.com.

For a detailed comparison of how first-party and third-party claims differ, see our guide to first-party vs. third-party insurance claims.

Loss of use: what it means and when it applies

"Loss of use" is the legal concept behind the third-party rental entitlement. It refers to the compensation owed for not being able to use the vehicle during the repair period. In a third-party claim, loss of use is typically calculated as the fair rental value of a comparable vehicle for the number of days the repair reasonably takes.

One detail that catches car owners off guard: loss of use compensation doesn't require actually renting a vehicle. A car owner who borrows a friend's car or uses public transit can still be entitled to loss-of-use compensation from the at-fault driver's insurer, since the loss occurred regardless of how they got around. The compensation reflects what a comparable rental would have cost for that period.

What happens when repairs run longer than the rental allowance

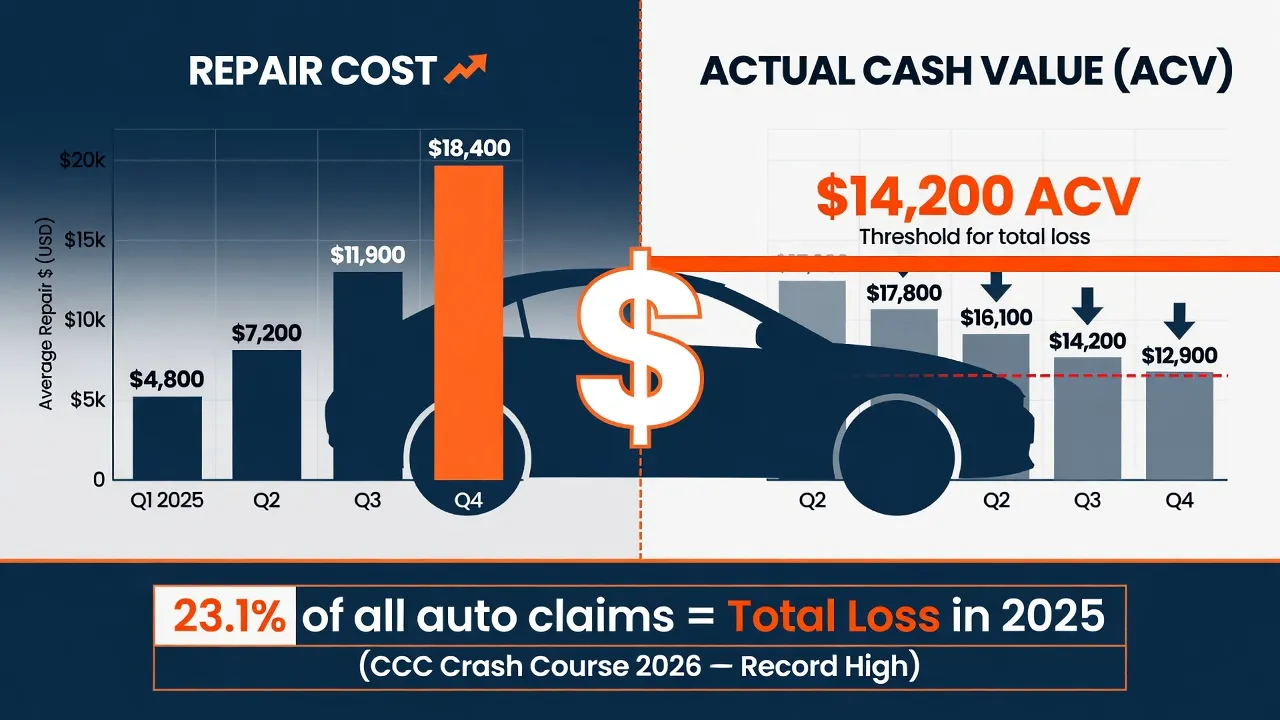

This is the scenario that blindsides most car owners. A complex collision repair — particularly one involving structural damage, parts on backorder, or Advanced Driver Assistance Systems (ADAS) recalibration — can extend well beyond the 30-day typical maximum.

According to data from Enterprise's Q2 2025 repair cycle report, the national average repair time is 15 to 17 days. But that average hides how wide the range actually is:

- Minor cosmetic repairs: 3 to 7 days

- Moderate collision damage: 10 to 20 days

- Major structural repairs: 20 to 45+ days

Then there's the ADAS factor. According to CCC Crash Course 2026 data, 28.3% of all repairable collision estimates now include at least one ADAS calibration requirement. Many shops sublet calibration work to specialty vendors, adding days to the timeline. Parts shortages for newer vehicles — particularly EVs and luxury brands — can add weeks.

When a repair runs past the rental coverage limit, car owners have several options.

Option 1: Request a rental extension from the insurer

If the repair is taking longer due to factors outside the car owner's control — parts delays, supplement approval delays, or ADAS calibration — documenting the cause and requesting an extension is the first step. Insurers aren't required to extend coverage past the policy limit, but adjusters can authorize extensions in documented cases. The body shop can provide written documentation of the delay cause to support the request.

Option 2: Negotiate with the at-fault insurer (third-party claims)

In a third-party claim, the at-fault driver's insurer is responsible for the full, reasonable repair period — not just the limit on the injured party's own policy. If the repair genuinely takes 45 days, the at-fault insurer owes 45 days of loss-of-use compensation. Document all delay causes, get written confirmation from the body shop, and request that the at-fault insurer extend the rental period accordingly.

Option 3: Check credit card rental coverage

Many major credit cards — Visa Signature, World Mastercard, and premium travel cards in particular — provide collision damage coverage for rental vehicles when the rental is charged to that card. This coverage typically applies to the damage risk of the rental vehicle itself, not the rental period cost. That said, some premium cards offer secondary rental coverage that can supplement an insurance policy. Check the card's benefits guide for specifics.

Option 4: Ask the body shop

Some body shops — particularly those with established insurance relationships — keep loaner vehicles available for customers whose repairs are running long. This isn't universal and typically not guaranteed, but it's worth asking, especially at shops with Direct Repair Program (DRP) relationships where the insurer may have pre-arranged loaner provisions.

Rental coverage when the car is declared a total loss

When an insurer determines that the repair cost exceeds the vehicle's value — a total loss — the rental situation changes. The repair period is over, but the car owner still doesn't have a vehicle.

Most policies and state-standard insurance practices extend rental coverage through the total loss settlement process, not just the repair period. Rental coverage typically continues until the insurance company has:

- Made a formal settlement offer on the total loss value

- Issued payment for the vehicle

The car owner shouldn't be left without transportation just because the vehicle was declared a total loss before a settlement is reached. If an adjuster suggests rental coverage ends immediately at total loss declaration, that position is often wrong — and worth pushing back on with a written request citing the "reasonable period" standard.

For a full explanation of total loss rights and how to respond if the settlement offer is too low, see our guide to what happens when insurance totals your car.

How to coordinate the rental: a practical checklist

Once coverage is confirmed, coordinating the rental involves a few practical steps that can prevent cost surprises:

Before the repair begins:

- Confirm rental reimbursement is on the policy and note the daily and total limits

- Ask the body shop for a repair timeline estimate in writing

- If the repair is complex, ask specifically whether ADAS calibration is required and whether the shop handles it in-house or sublets it

When setting up the rental:

- Choose a vehicle class at or below the policy's daily reimbursement rate to avoid out-of-pocket daily gaps

- If the insurer has a preferred rental company (Enterprise, Hertz, or similar), using it often enables direct billing — the insurer pays the rental company directly rather than reimbursing the car owner after the fact

- Decline the rental company's collision damage waiver if the car is covered under the insurer's liability and the policy explicitly covers rental vehicles; check the policy first

If the repair runs long:

- Get written documentation from the body shop explaining the delay cause

- Contact the insurer with that documentation before the policy limit is reached, not after

- In a third-party claim, contact the at-fault insurer separately with the same documentation

Frequently asked questions about rental car coverage after an accident

Does rental reimbursement have a deductible?

Typically, no. Rental reimbursement coverage doesn't carry its own deductible. The deductible on the underlying claim (collision or comprehensive) applies to the vehicle repair, not to the rental coverage itself.

Does filing for a rental affect my insurance rates?

The rental reimbursement claim itself generally doesn't trigger a premium increase on its own. If the underlying collision or comprehensive claim affects the premium, the rental reimbursement used in connection with that claim is part of the same claim event.

What if I don't want to rent a car — can I get a cash payment instead?

In a third-party loss-of-use situation, compensation is typically owed for the reasonable rental value of a comparable vehicle regardless of whether a rental was obtained. In a first-party claim using the car owner's own rental reimbursement coverage, the insurer generally pays only actual rental costs incurred — not a cash equivalent for days the car was in the shop without a rental.

Does rental reimbursement cover rideshare services like Uber or Lyft?

Some policies extend transportation expense coverage to rideshare fares, public transit, or taxis as alternatives to a rental vehicle. Check the specific policy language, as this varies by insurer and endorsement type.

Can I add rental reimbursement coverage after an accident?

No. Rental reimbursement coverage added after an accident applies only to future losses, not the current claim. Coverage must be in place before the incident occurs to apply to it.

How long will insurance cover a rental car during repairs?

Coverage duration depends on the policy's per-claim maximum divided by the daily rate. With a $30/day limit and $900 maximum, coverage lasts 30 days. With a $50/day limit and $1,500 maximum, coverage also lasts 30 days. For third-party claims, the at-fault driver's insurer owes coverage for the full, reasonable repair period regardless of these limits.

Key takeaways

Rental car coverage after an accident comes with more conditions and limits than most car owners expect. A few things worth remembering:

- Rental reimbursement is an optional add-on, not standard. Verify it's on the policy before the repair starts.

- Know both limits: the daily cap and the per-claim maximum. In high-cost markets, daily limits may fall short of actual rental rates from day one.

- Third-party claims carry separate rental rights: if the other driver was at fault, their liability coverage typically owes compensation for the rental period — even if the car owner has no rental reimbursement coverage of their own.

- ADAS calibrations and parts delays are extending repair timelines. With 28.3% of collision repairs now requiring calibration, plan for repairs that may run longer than traditional timelines suggest.

- Document everything: written delay documentation from the body shop supports extension requests and loss-of-use negotiations.

Car owners navigating a collision repair should review their insurance coverage before arranging a rental, confirm the full claims timeline with the body shop, and understand which insurer — their own or the at-fault driver's — is responsible for the rental cost.

For more on how the full insurance claims process works, including what happens with supplements, OEM parts disputes, and low estimates, see our auto body insurance claims: complete consumer guide.

Insurance processes and coverage terms vary by state and carrier. Consult your specific policy and your state's Department of Insurance for details applicable to your situation.

Last updated: June 2026