When an insurance company writes a repair estimate for a collision claim, most car owners assume the replacement parts will match what came off the assembly line. That assumption is usually wrong. Insurance companies default to aftermarket parts — components made by third-party manufacturers, not your vehicle's maker — as a routine cost-control measure. The difference between OEM and aftermarket can affect fit, finish, resale value, and whether your vehicle's safety systems work correctly after the repair.

Understanding the OEM vs. aftermarket parts insurance claim issue gives car owners the knowledge to push back, ask the right questions, and in some states, demand original parts as a legal right.

This article is part of the auto body insurance claims guide for car owners navigating the full claims process.

What OEM and aftermarket parts actually mean

OEM parts (Original Equipment Manufacturer) are replacement components built by the same manufacturer — or the same approved supplier — that produced the original parts when the vehicle was assembled. An OEM front bumper for a 2023 Toyota RAV4 matches the exact tolerances, material grades, and mounting specifications of the bumper that left the factory. Manufacturer warranty coverage follows OEM parts.

Aftermarket parts are produced by independent third-party companies with no affiliation to the vehicle manufacturer. Quality varies widely — from certified parts that have passed independent testing for fit and finish, to uncertified parts that may need modification to install correctly.

Recycled OEM parts (also called salvage or used OEM) are original manufacturer parts pulled from vehicles written off as total losses. They carry no manufacturer warranty and availability depends on local salvage inventory, but they sit in a middle ground between new OEM and new aftermarket.

Three practical things hinge on this distinction: fit and finish during the repair, safety system performance after the repair, and resale value when the vehicle changes hands.

| Part Type | Source | Typical Cost vs. OEM | Manufacturer Warranty | Best For |

|---|---|---|---|---|

| OEM (new) | Vehicle manufacturer or approved supplier | Baseline | Yes | Newer vehicles, ADAS-equipped, warranty-active |

| Recycled OEM (used) | Salvage yard (original manufacturer parts) | 30–60% less | No | Mid-age vehicles, non-ADAS panels |

| Aftermarket (certified) | Third-party, independently tested | 20–50% less | No | Older vehicles, non-safety-critical panels |

| Aftermarket (uncertified) | Third-party, no independent testing | 20–60% less | No | Generally not recommended for structural or sensor-adjacent parts |

Why insurance companies default to aftermarket parts

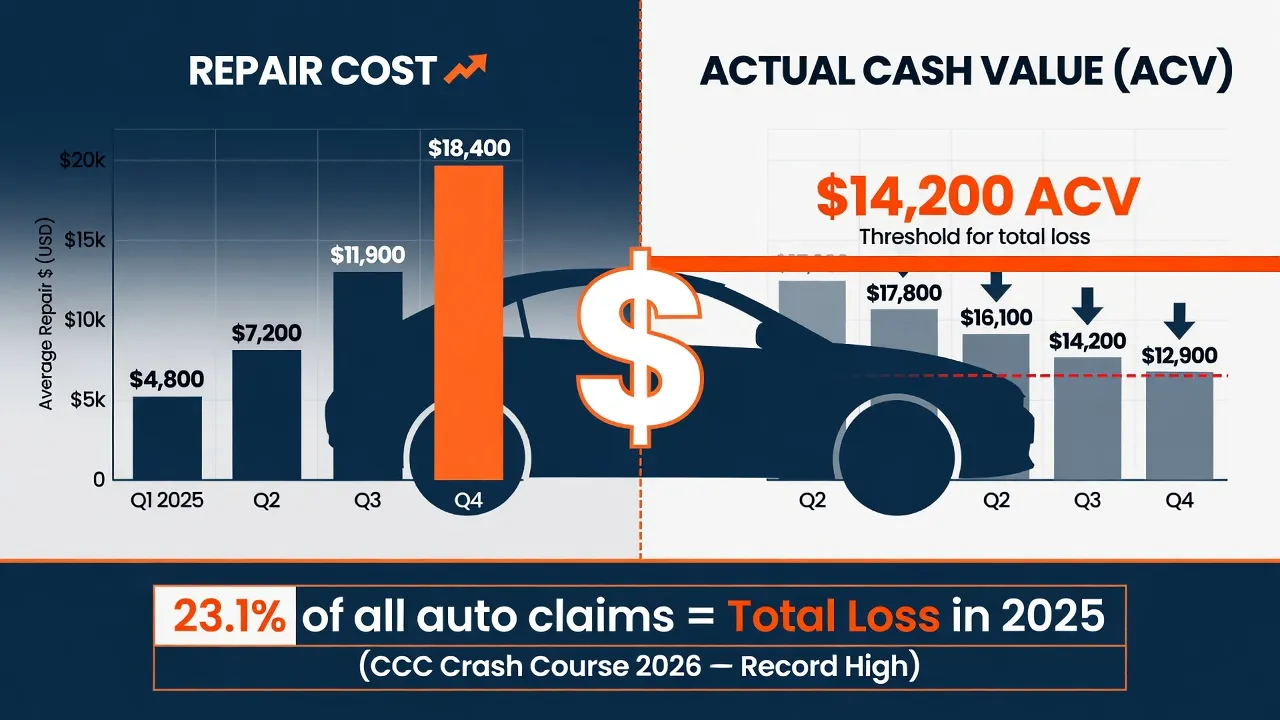

Insurance companies include aftermarket parts in repair estimates as a standard cost-reduction practice. Aftermarket body panels, bumper covers, and structural brackets typically cost 20% to 50% less than OEM equivalents. On a multi-panel repair with a $4,818 national average claim cost (CCC Crash Course 2026), the parts savings are real to the insurer's bottom line.

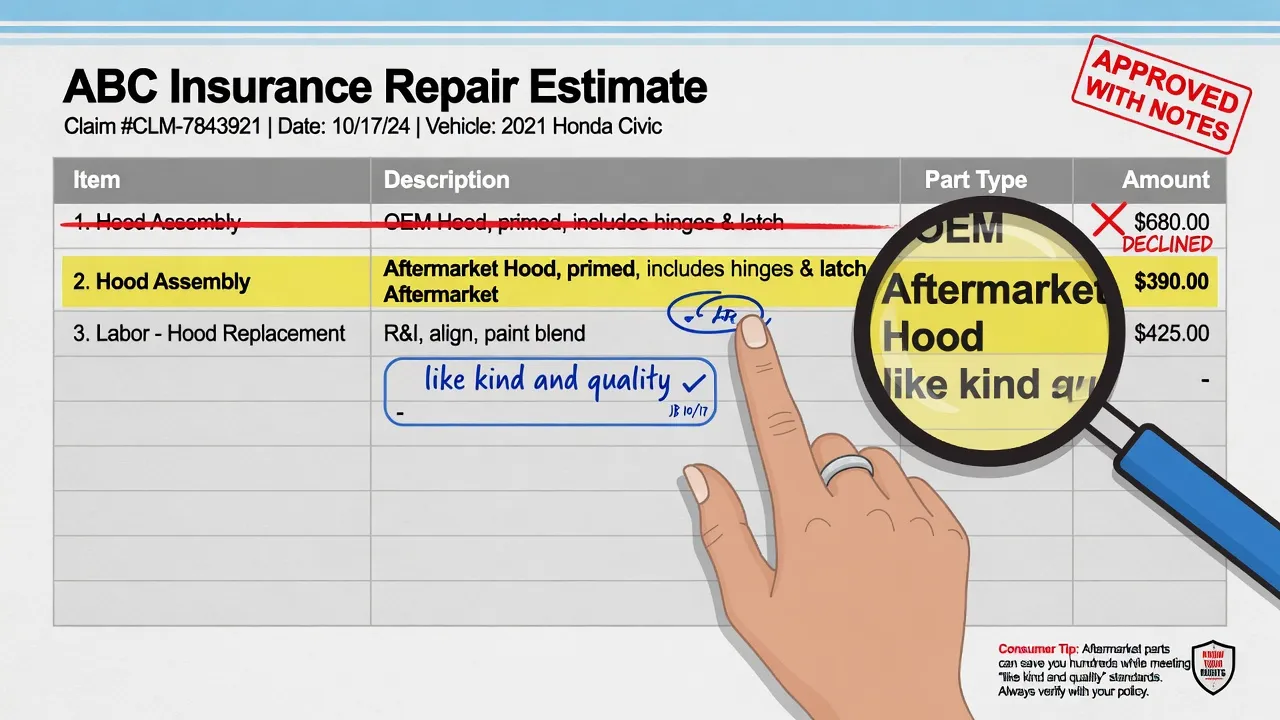

Most auto insurance policies contain language allowing the insurer to use parts of "like kind and quality" — an insurance industry term meaning replacement parts that are functionally equivalent to the originals, though not identical in source or manufacturer. From the insurer's perspective, this language permits aftermarket substitution as long as the repair restores the vehicle to its pre-loss condition. Car owners rarely see this language unless they read their policy carefully before an accident.

The adjuster builds the repair estimate using parts sourcing software (commonly CCC ONE), which automatically populates the parts list with aftermarket or recycled options unless the policy or state law requires otherwise. Unless a car owner or body shop challenges a line item, the estimate stands.

Understanding this default is the first step in any OEM vs. aftermarket parts insurance claim dispute. The system is built to favor insurer cost savings — not the car owner's long-term interests in resale value or safety system performance. This is also one reason why the choice between a Direct Repair Program (DRP) shop and an independent body shop matters: DRP shops vs. independent body shops have different levels of contractual flexibility when it comes to advocating for OEM parts on a claim.

The real-world impact on your vehicle

Fit and finish problems

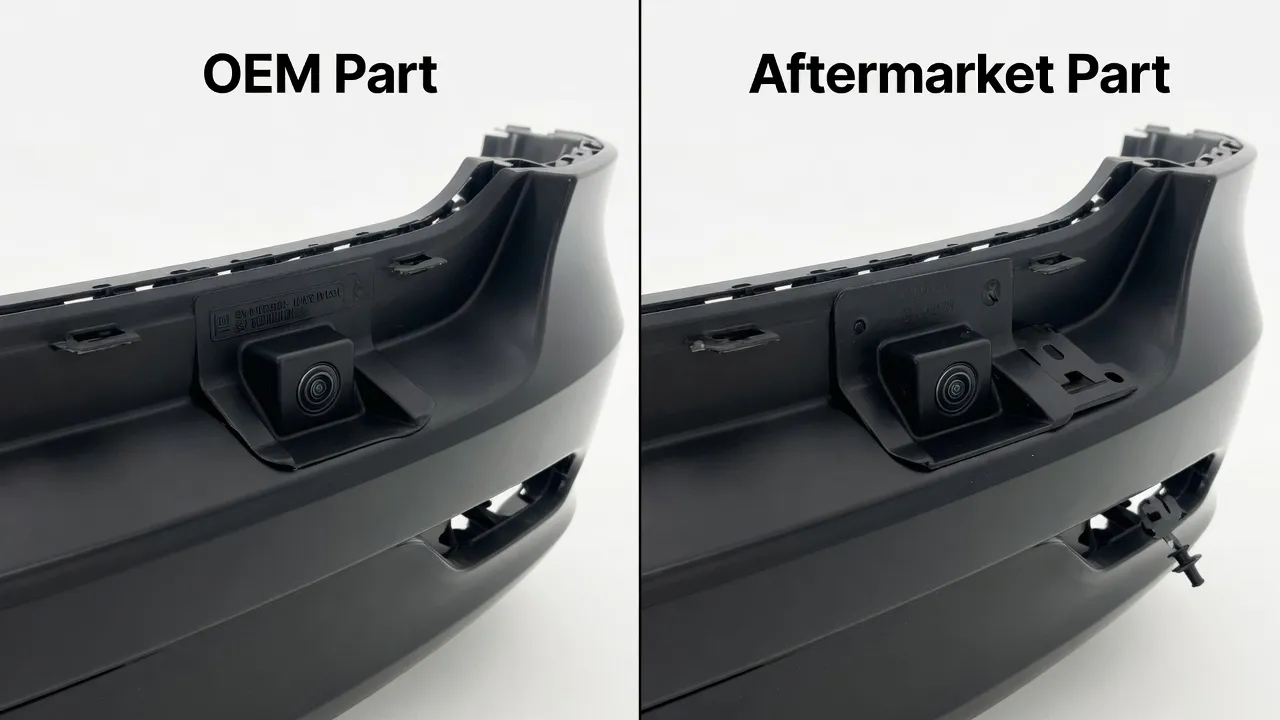

Aftermarket body parts vary in how precisely they match OEM dimensions. In blind testing conducted by a major insurer's body shop program, independent observers found that 75% to 80% of non-OEM hoods and fenders needed metal adjustment — technicians had to "massage" the panels to fit correctly. That adjustment adds labor time and, in some cases, leaves visible panel gaps or misaligned body lines that reduce the repair's cosmetic quality.

For car owners, this often surfaces at vehicle pickup. A fender that sits slightly proud of the door. A bumper cover with an uneven gap at the headlight. A hood with a crease that doesn't quite follow the vehicle's body line. These are all signs that aftermarket fit tolerances weren't tight enough for the specific vehicle.

ADAS safety system risks

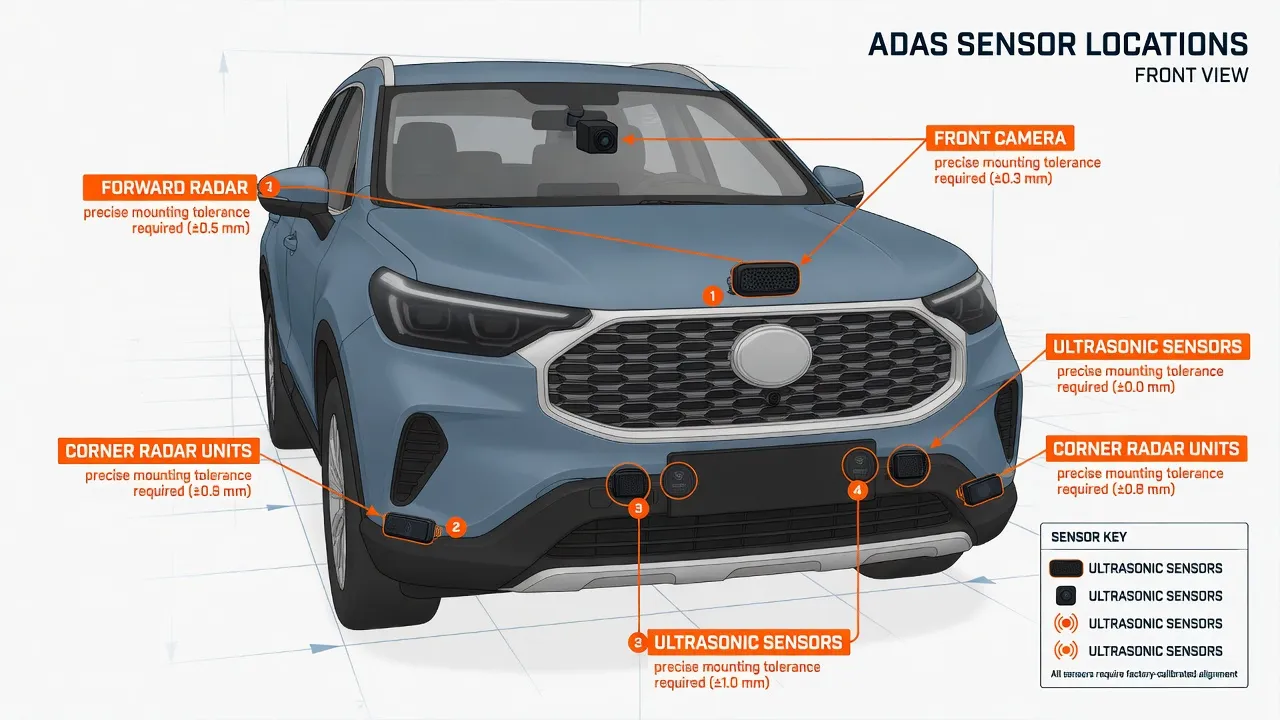

This is where the OEM vs. aftermarket parts insurance claim debate has shifted in recent years. Modern vehicles — 2019 and newer models especially — integrate radar sensors, forward-facing cameras, ultrasonic sensors, and lidar units directly into body panels, bumpers, and grille assemblies. According to CCC Crash Course 2026 data, 28.3% of repairable collision estimates now include at least one ADAS calibration line item.

The calibration process requires that sensors sit within manufacturer-specified tolerances for angle, height, and lateral position. Even a 0.6-degree deviation in camera angle can reduce the effectiveness of automatic emergency braking, according to Insurance Institute for Highway Safety (IIHS) research. A 2025 industry study found that an aftermarket windshield used without proper recalibration caused lane departure warning inconsistency and full automatic emergency braking failure during testing.

Aftermarket bumpers, grilles, and mirror housings may not position sensor mounting points within the tolerances needed for reliable calibration. In those cases, the body shop may complete the calibration with compromised results or flag the part as incompatible — which triggers a supplement claim. Either outcome costs time and, potentially, safety performance. For a full explanation of how supplement claims work and how long they take, see what is an insurance supplement in auto body repair. This issue is particularly acute for windshield replacements, where the camera mounted at the base of the glass requires OEM-grade glass thickness and clarity — see auto glass repair and ADAS recalibration for a deeper look at windshield-specific considerations.

Resale value reduction

Car buyers, used car dealers, and trade-in evaluators check repair history and flag aftermarket body panels. Vehicles repaired with aftermarket structural components can fetch 5% to 10% less on trade-in compared to equivalent vehicles repaired with OEM parts, according to trade-in valuation surveys. On a vehicle worth $30,000, that gap is $1,500 to $3,000 — a cost that materializes years after the claim, and one insurers never mention when writing the estimate.

This resale value reduction is also connected to diminished value claims. Aftermarket repairs can deepen the inherent diminished value of a repaired vehicle, since buyers perceive the repair quality as lower. For more on this, see the diminished value claim guide.

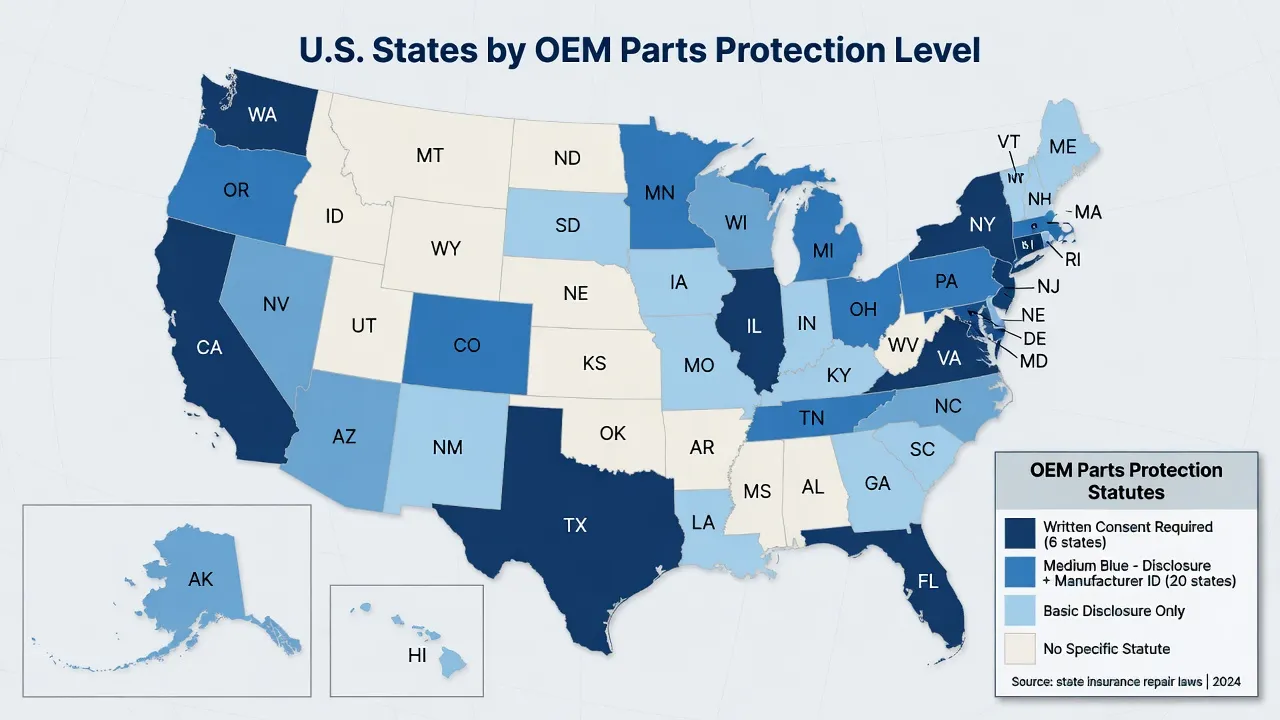

State laws: what your insurer is required to tell you

Thirty-five states have statutes or regulations addressing insurer obligations around non-OEM aftermarket parts, according to consumer rights resources maintained by crashrepairinfo.com. The protections vary widely:

31 states require that repair estimates include a disclosure statement when non-OEM parts are specified. Car owners in these states should see language on the estimate identifying aftermarket components.

20 states require the estimate to identify the manufacturer of each non-OEM part — not just note that aftermarket parts are used generally.

Six states require the consumer's written consent before non-OEM parts can be installed:

- Arkansas — written notice required

- Indiana — written consent required for vehicles within five model years

- Kansas — estimate must identify non-OEM parts

- Rhode Island — written consent required for vehicles within 30 months of model year

- West Virginia — written notice required before use

- Additional state requirements are being adopted: Louisiana introduced legislation in 2026 requiring written consent before any non-OEM installation on first-party and third-party claims

California requires that car owners receive an Auto Body Repair Consumer Bill of Rights disclosing their options. Aftermarket part manufacturers must be identified in writing when their parts are used in California repairs. Car owners looking for shops in California that work with OEM parts can find them through the auto body shops in California directory.

Even in states without consent requirements, the "pre-loss condition" standard in most policies creates a path for disputing aftermarket parts that demonstrably don't restore the vehicle to original quality — particularly for ADAS-equipped components.

Important: Regardless of state law, car owners always have the right to request OEM parts and pay the cost difference out of pocket. The insurer controls what the policy covers — not what parts the body shop installs. That distinction gives every car owner leverage, in every state.

How to request OEM parts on an insurance claim

Requesting OEM parts doesn't require legal action or confrontation. Most car owners who ask, in writing, during the claim process get their requests accommodated — either by the insurer or with a modest out-of-pocket payment for the cost difference.

Step 1: Review your policy for OEM language. Some policies include an OEM endorsement or OEM amendment that covers original parts at no additional cost per claim. Check the declarations page and any endorsements attached to the policy. An OEM endorsement typically adds $20 to $50 per year to the annual premium.

Step 2: Submit a written request to the adjuster. At the time the repair estimate is being prepared — before repairs begin — send written communication stating that OEM parts are requested for the claim. Reference the vehicle's age (if it's within the manufacturer warranty period, this strengthens the request), any state law consent requirements, and any ADAS components involved.

Step 3: Confirm which parts are OEM-eligible under the policy. Insurers apply OEM parts to vehicles within five to seven model years. For vehicles older than this threshold, full OEM coverage is less common, though safety-critical components (sensor brackets, structural mounts) often warrant individual negotiation.

Step 4: Ask the body shop to advocate on your behalf. Body shops that are OEM-certified or familiar with supplement processes can document why specific components need OEM parts — for ADAS-related brackets and sensor housings especially. That documentation strengthens a supplement request to the insurer. When selecting a shop for a collision repair involving ADAS-equipped components, confirming OEM certification status upfront is worth the extra step.

Step 5: If denied, pay the difference or dispute. If the insurer won't authorize OEM parts under the policy, car owners have two options: pay the cost difference out of pocket (often $100 to $300 per major panel), or dispute the estimate by requesting that the body shop document why the aftermarket part doesn't restore the vehicle to pre-loss condition. In that case, the supplement process — covered in what to do when the insurance estimate is too low — applies.

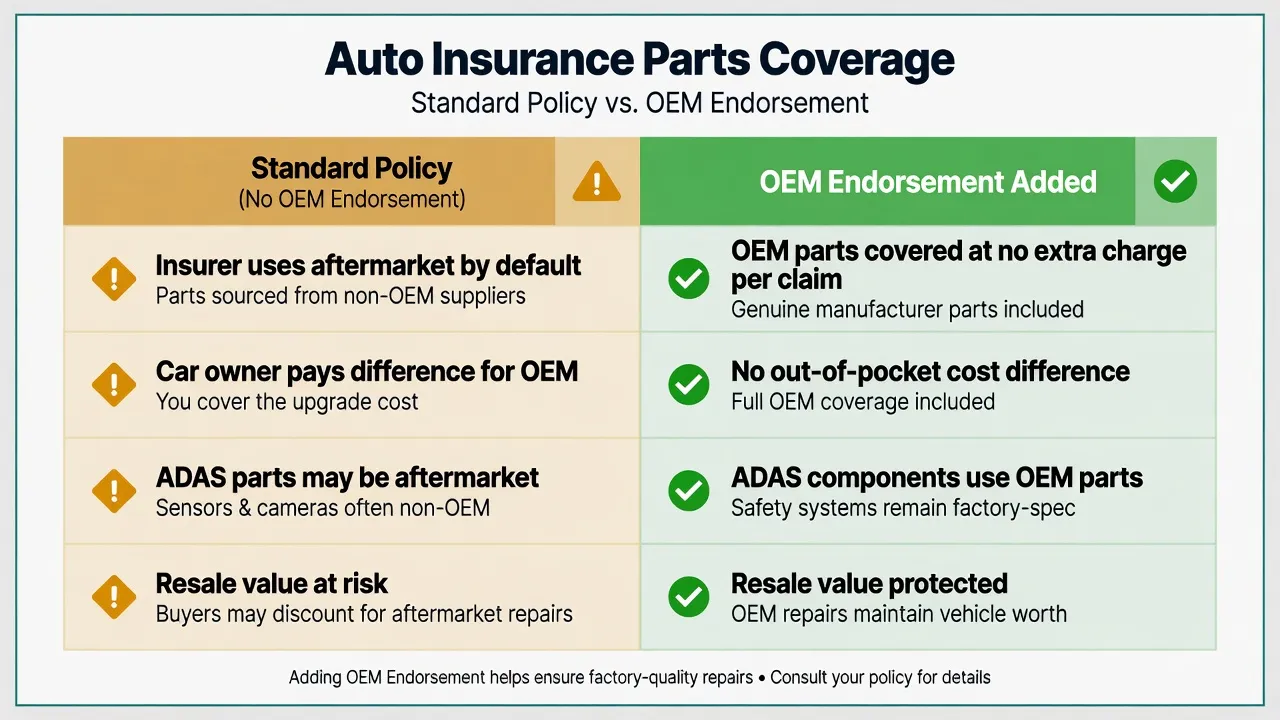

OEM endorsements: adding protection before the next claim

An OEM parts endorsement is a policy add-on that obligates the insurer to cover original manufacturer parts, regardless of their default parts policy. Not all insurers offer this endorsement, and it applies only to vehicles within a certain age window (commonly five to ten model years).

Some insurers offer OEM parts endorsements as a named add-on to the policy, while others allow policyholders to request OEM parts at claim time with the cost difference paid out of pocket — without a formal endorsement requirement. Coverage varies by carrier, and not all insurers offer an OEM endorsement for passenger cars at all. Reviewing the policy declarations page, or calling the insurer directly before a claim occurs, is the most reliable way to understand what OEM coverage is available.

Cost for an OEM endorsement is $20 to $50 per year added to the annual premium — a modest amount relative to the $1,500 to $3,000 resale value protection it can preserve.

If a vehicle is newer, financed, or leased, an OEM endorsement deserves serious consideration. Many lease agreements and manufacturer warranties include language that could be affected by aftermarket repair parts.

New vehicles, warranties, and the Magnuson-Moss Warranty Act

Car owners with vehicles still under the manufacturer's original warranty should know how aftermarket parts interact with warranty coverage. The Magnuson-Moss Warranty Act (15 U.S.C. § 2302) prohibits manufacturers from voiding a vehicle warranty solely because an aftermarket part was used — unless the manufacturer can show that the aftermarket part caused the defect or failure at issue.

In practice, a manufacturer can't void the entire powertrain warranty because an aftermarket bumper cover was installed after a collision. But if an aftermarket sensor bracket leads to a calibration failure that damages the vehicle's ADAS control module, the manufacturer may deny warranty coverage for that specific system failure on the grounds that the aftermarket part caused the damage.

For vehicles under warranty, requesting OEM parts — for any component near a sensor, camera, or structural weld point — reduces this risk.

Frequently asked questions

Can an insurance company force me to use aftermarket parts?

No — an insurance company can't force a car owner to accept aftermarket parts. However, most policies allow the insurer to limit payment to the cost of aftermarket equivalents. Car owners can always insist on OEM parts and pay the cost difference themselves. In six states with written consent requirements — Arkansas, Indiana, Kansas, Rhode Island, West Virginia, and states passing new legislation in 2026 — the insurer must obtain the car owner's written consent before using non-OEM parts at all. In all states, the repair must restore the vehicle to pre-loss condition; documented fit or safety failures provide grounds for a supplement dispute.

Do I have to pay extra for OEM parts on an insurance claim?

Whether the insurer covers the full cost of OEM parts depends on the policy and state. If an OEM endorsement is in place, OEM parts are covered at no extra charge. Without an endorsement, car owners pay the difference between the aftermarket cost the insurer approved and the OEM cost — often $100 to $300 per major panel. Confirm this cost in writing before repairs begin.

Does using aftermarket parts affect my car's resale value?

Yes. Trade-in valuation surveys indicate that vehicles repaired with aftermarket body panels may receive offers 5% to 10% lower than comparable vehicles repaired with OEM parts. Informed buyers and dealer appraisers identify aftermarket parts through visible panel gap inconsistencies, missing OEM part stamps, and CARFAX repair records. This resale value reduction is separate from — and in addition to — any inherent diminished value the vehicle carries as a result of the accident itself.

What parts should I always request OEM on?

For vehicles with ADAS systems, request OEM parts on any component housing or adjacent to a sensor, camera, or radar unit — including front and rear bumper assemblies, grille structures, mirror housings, A-pillar trim, and windshield frames. Structural components at weld points and high-crumple-zone areas also benefit from OEM replacement, given manufacturing specification requirements for crash energy management.

Does the adjuster tactic of specifying aftermarket parts constitute insurance steering?

Specifying aftermarket parts in an estimate is a standard and generally legal insurer practice, distinct from shop-steering (directing a car owner to a specific repair facility). Authorizing aftermarket parts without disclosure in a state with consent requirements may violate state insurance regulations. Car owners who believe they're being pressured into accepting aftermarket parts without proper disclosure should document the communication and contact their state's Department of Insurance. For more context on adjuster practices, see the insurance adjuster tactics guide.

Key takeaways for car owners

The OEM vs. aftermarket parts insurance claim question isn't academic. It affects whether sensors calibrate correctly after repair, whether the vehicle fetches a fair price at trade-in, and whether the manufacturer warranty holds on adjacent systems. Insurers make the aftermarket default because it saves them money — not because it serves the car owner's interests.

Quick reference: what every car owner should know

- Insurers default to aftermarket using "like kind and quality" policy language — this is standard and expected

- Car owners can always request OEM parts and pay the cost difference, in every state

- Six states require written consent before any non-OEM parts can be installed

- OEM parts matter most for ADAS components — sensor brackets, bumper assemblies, mirror housings, windshields

- An OEM endorsement eliminates out-of-pocket cost differences for original parts on covered claims

- Aftermarket repairs can reduce resale value by 5% to 10% — a cost that materializes years after the claim

Car owners who ask in writing, know their state's disclosure or consent requirements, and understand the cost of OEM alternatives are in a much stronger position to get the repair they're entitled to. An OEM endorsement added before the next claim costs less per year than a single tank of gas for most vehicles.

For the full picture of how insurance claims work — from filing through supplement disputes, total loss decisions, and beyond — see the complete auto body insurance claim guide.

Find certified auto body shops near you that advocate for OEM parts and carry manufacturer-specific repair certifications at AutoBodyShopNear.com.

Insurance processes, state regulations, and consumer rights vary. Consult your specific policy and your state's Department of Insurance for details applicable to your situation. Last updated: June 2026.