After a collision, most car owners face the same immediate question: how does this actually work?

Filing an auto body insurance claim involves more steps, and more decisions, than most people expect. The insurer, the body shop, the repair estimate, and the choice of parts all intersect in ways that affect both repair quality and what you pay out of pocket.

This guide walks through the full collision repair insurance claim process, from deciding whether to file at all to reviewing the completed work. It also covers your rights as a car owner, including the right to choose your own shop, and how to handle the disputes that commonly come up.

For a broader overview of the collision repair process itself, see the complete collision repair guide.

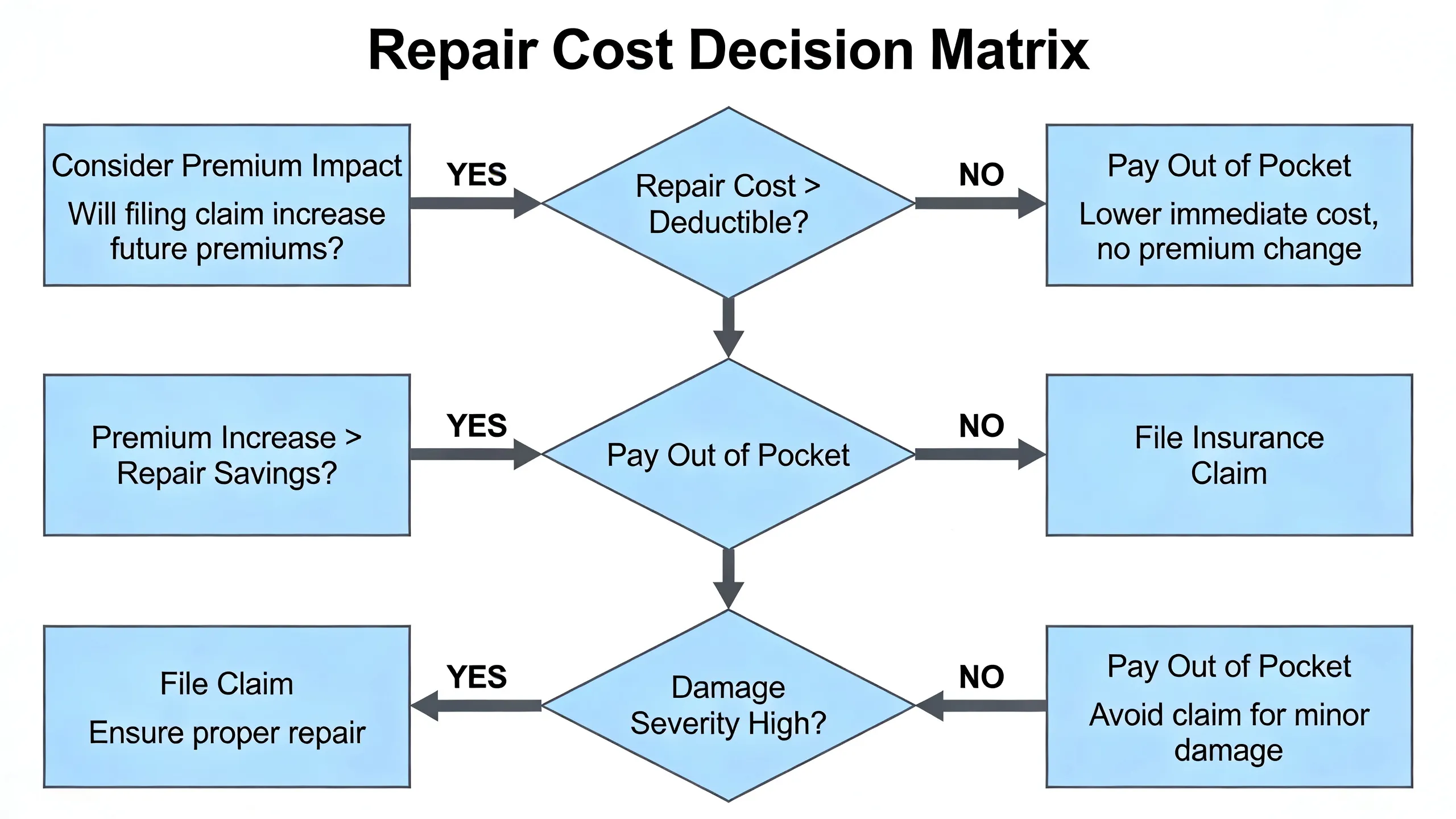

Should You File a Claim or Pay Out of Pocket?

Not every collision warrants a claim. Before calling the insurer, run the math. Filing when it doesn't make financial sense often costs more in the long run.

The deductible math

Your deductible is what you pay before insurance covers the rest. Common deductibles run $250 to $1,000 or more depending on the policy. The math is straightforward:

If repair cost is at or near your deductible, filing probably doesn't save you money.

Example: a $750 repair with a $500 deductible means the insurer pays only $250. That benefit likely doesn't justify the paperwork, the rate conversation, or the claims history entry.

The math shifts for larger repairs. A $5,000 repair with a $500 deductible means the insurer absorbs $4,500. That gap usually justifies filing.

When paying cash saves money

Several scenarios favor paying cash:

- Minor cosmetic damage: small dents, door dings, or paint scratches under $500

- Damage at or below the deductible: the math just doesn't work in your favor

- Recent claims on the policy: carriers track claims history, and another filing can push premiums up or trigger non-renewal

- Damage to another person's car: if the other driver is willing to settle privately in cash, some people go this route to avoid a claim record (though this carries risk if injuries appear later)

Worth thinking through before you dial. For repair cost context to inform the calculation, see the collision repair cost guide.

Impact on future premiums

Filing a collision claim typically raises premiums at renewal. The national average increase after a single at-fault claim is roughly 40-50%, though actual impact varies by insurer, state, and your driving history. Some carriers offer accident forgiveness that waives the first surcharge. Worth asking about if you haven't.

Not-at-fault claims generally hit premiums less hard, though some carriers still adjust rates based on overall claims frequency. Call your insurer before filing and ask what the likely rate impact looks like, most will give you an estimate on request.

How to File a Collision Repair Insurance Claim

The process follows six steps once you decide to file: document the scene, notify your insurer promptly, get a damage estimate, choose a body shop, approve the repair plan in writing, and inspect the completed work before signing off.

Understanding each step in advance cuts down on delays and helps you avoid the most common mistakes.

Step 1: Document everything at the scene

Before any vehicle moves, document everything. This is the foundation of your claim.

- Photos of all damage from multiple angles, close-up and wide-angle

- Photos of the full scene: vehicle positions, road conditions, traffic controls

- Contact information for every driver involved: name, phone, insurance carrier, policy number, license plate, driver's license number

- Witness information if anyone saw the crash

- A police report number: file a report even for minor collisions; many insurers require it and all benefit from the official record

Get the documentation before vehicles move, whenever it's safe. Scene evidence disappears the moment cars are moved and traffic resumes.

Step 2: Contact your insurance company

Notify your insurer promptly. Most policies require "prompt notice" of a loss, waiting too long can complicate or jeopardize the claim.

Have this ready when you call:

- Policy number

- Date, time, and location of the collision

- A factual description of what happened (stick to what you observed)

- Contact information for all parties

- Police report number, if available

- Photos, most carriers accept digital uploads

The insurer assigns a claim number and an adjuster. The adjuster is the insurance professional who assesses damage and determines the payout. Write down both their name and the claim number. Every communication after this should reference the claim number.

Step 3: Get a damage estimate

An estimate is a written assessment of required repairs and what they cost. The insurer may send an adjuster to inspect directly, ask you to bring the car to an approved facility, or accept an estimate from a shop you choose.

You're not required to accept the insurer's initial estimate as the final word. Shops regularly find additional damage once a vehicle is torn down, that triggers a "supplement," which is covered in detail later.

For significant damage, getting at least one independent estimate from a qualified shop before authorizing repairs gives you a realistic baseline. Find qualified collision repair shops to start the estimate process.

Step 4: Choose your body shop

This is one of the most consequential decisions in the claims process. It's also one where you have real legal rights, covered fully in the section below.

Short version: the insurer may suggest a shop, but you have the right to choose any licensed repair facility. In most states, the insurer cannot legally require a specific shop as a condition of claim payment.

Once you've selected a shop, give them the claim number and adjuster's contact info. From there, the shop communicates directly with the insurer on repair scope and estimate.

Step 5: Approve the repair plan

Before repairs start, the shop provides a written repair order detailing what will be done and what it costs. Read it. If the repair scope or parts choices (OEM vs. aftermarket, covered later) don't match what you expected, this is the moment to raise it.

The insurer approves the estimate or requests changes. If the shop's estimate exceeds the approved amount, the supplement process kicks in. Don't feel pressured to sign off until scope and coverage are clearly documented and agreed upon.

Step 6: Review completed work

Inspect the vehicle thoroughly before accepting delivery. A quality collision repair should be invisible, aligned panels, matched paint, all mechanical systems working normally.

Check these before signing:

- Panel gaps are even and consistent

- Paint color and texture match the surrounding panels

- No masking lines, overspray, or compound residue

- All trim, lights, and sensors reinstalled correctly

- Mechanical systems feel right (steering, braking, suspension)

- Repair documentation and warranty provided in writing

If anything looks off, note it on the delivery paperwork before you sign. Good shops address legitimate concerns without argument. If something shows up after you've left, your written warranty is the mechanism for recourse.

Your Right to Choose Your Own Body Shop

The right to choose your repair facility is one of the most valuable, and least understood, consumer protections in the insurance claim process. It's protected under state law in nearly every state, though the specifics vary.

What the law actually says

Most states explicitly prohibit insurers from requiring a specific repair shop as a condition of claim payment. The National Association of Insurance Commissioners (NAIC) maintains model regulations on this, and most state insurance codes include language that:

- Prohibits making the use of a specific shop a condition of payment

- Requires insurers to inform policyholders of their right to choose

- Prohibits steering practices that effectively force a particular shop without disclosure

In states with strong consumer protection enforcement, like California, where the Department of Insurance actively pursues anti-steering violations, insurers face real penalties. In no-fault states like Florida, similar protections apply alongside the state's unique insurance framework.

How to push back on insurer pressure

Insurers sometimes steer policyholders toward Direct Repair Program (DRP) shops with language like "our preferred shops" or "approved repair facilities." The implication is that using a different shop causes problems, delays, coverage disputes, denied supplements. That's often not accurate.

If you run into that pressure:

- State clearly: "I understand I have the right to choose my own repair facility."

- Ask the insurer to put any claim requirements in writing.

- If the steering is aggressive or misleading, file a complaint with your state insurance commissioner. The NAIC state insurance department directory links to every state's complaint resource.

DRP shops: pros and cons

Direct Repair Programs are networks of shops with agreements covering inspection processes, pricing, and turnaround standards. Using a DRP shop isn't automatically a bad choice, many are genuinely good operations. But the trade-offs are worth understanding.

| Factor | DRP Shop | Independent Shop |

|---|---|---|

| Claim processing speed | Often faster, direct insurer relationship | May involve more back-and-forth with insurer |

| Parts choices | DRP agreements may favor aftermarket parts | More flexibility to advocate for OEM parts |

| Warranty | Typically backed by insurer | Shop's own warranty applies |

| Shop selection | Limited to insurer's network | Car owner's choice |

| Quality | Varies, network membership is not a quality guarantee | Varies, certifications indicate training level |

For guidance on selecting a quality repair facility regardless of DRP status, see the guide to choosing a collision repair shop.

Understanding Insurance Repair Estimates

Estimate disputes are the most common friction point in the insurance auto body repair process. Knowing how estimates get written, and why they routinely differ, gives you the tools to handle these situations without panic.

How insurers write estimates

Insurance estimates are generated through estimating software. CCC, Mitchell, and Audatex are the three dominant platforms. These tools calculate repair costs using standardized labor times, parts prices, and paint procedures.

Initial estimates are often written from photos or a brief visual inspection. They're a calculation of visible damage, not a full repair assessment. That's why insurer estimates routinely need updating once a shop tears down the car and finds what was hidden underneath.

Why shop estimates differ from insurance estimates

A shop's estimate and the insurer's estimate almost always come in at different numbers. That's normal. Common reasons for the gap:

- Hidden damage: internal components, mounting brackets, and structural elements that weren't visible during initial inspection

- Labor rate differences: insurer rate schedules often don't match local market rates

- Parts choices: the insurer estimated aftermarket; the shop is quoting OEM

- Procedure gaps: shops following OEM repair procedures often include operations the insurer's initial estimate omitted entirely

- Blend operations: paint blending into adjacent panels is sometimes underpriced or left out of initial insurer estimates

Neither party is acting in bad faith. This is just how the process works.

The supplement process explained

A supplement is an update to the original repair estimate that adds operations or parts discovered during the repair. Shops submit them to the insurer as a routine part of the collision repair claim.

Here's how the process typically flows:

- Disassembly reveals damage not in the original estimate

- The shop documents it with photos and written notes

- A formal supplement request goes to the insurer with supporting documentation

- The insurer reviews and approves or disputes it

- Repair resumes once the supplement is resolved

Supplements can add time to the repair. They're not a sign the shop is padding the bill. They're the correct mechanism for handling incomplete initial assessments.

OEM vs. Aftermarket Parts in Insurance Repairs

Parts selection drives both repair quality and what you pay out of pocket. The insurance repair process almost always involves some negotiation on this point.

What insurers prefer, and why

Insurers prefer aftermarket parts because they cost less. A comparable aftermarket part typically runs 30-50% less than OEM, and insurers are managing claim costs.

"Like kind and quality" is a phrase that appears in many policies. From the insurer's perspective, that phrase can justify a functionally equivalent aftermarket part rather than an OEM one. If OEM matters to you, know this language and be ready to push back on it.

For a deeper look at this topic, see the guide to OEM vs. Aftermarket parts.

State laws on parts usage

Several states have enacted laws limiting aftermarket parts in insurance repairs. California requires insurers to disclose non-OEM parts usage and gives car owners the right to request OEM parts, with the insurer covering the cost difference in some situations. These protections vary a lot by state.

The California Department of Insurance consumer resources outline the state's specific protections in detail.

Car owners in states with stronger protections may have enforceable rights that others don't. When parts choice matters, check your state's insurance code or contact the state insurance department before the conversation with your adjuster.

How to request OEM parts

Car owners who want OEM parts used in their repair can:

- State the preference explicitly when selecting a repair shop, ask whether the shop will advocate for OEM parts with the insurer

- Reference the policy language: some policies include OEM parts guarantees for newer vehicles (typically under 3 years old)

- Cite state law if the state provides a statutory right to OEM parts disclosure or selection

- Negotiate the cost difference: in some cases, car owners pay the price difference between OEM and aftermarket, while insurance covers the aftermarket portion

- Document the request in writing to create a record if a dispute arises

Common Insurance Claim Disputes and How to Handle Them

Disputes happen. They're a regular part of the insurance auto body repair process, and most resolve through structured communication and documentation. Knowing the common types, and the steps to address them, keeps things from spiraling.

When the estimate comes in low

A low insurer estimate doesn't automatically mean a fight. Often it's just a supplement waiting to be submitted.

How to handle it:

- Ask the shop to document additional damage with photos and written notes

- Have the shop submit a formal supplement to the insurer

- If the supplement is disputed, request a written explanation of what was denied and why

- Ask for an adjuster re-inspection if the dispute involves physical damage that can be shown

- If it stays unresolved, consider engaging a licensed public adjuster or an attorney

Denied claim

A denial means the insurer has determined the loss isn't covered. Common denial reasons:

- Coverage exclusion: the specific damage type is excluded

- Lapsed policy: the policy wasn't active when the loss occurred

- Late reporting: the claim was filed outside the reporting window

- Fraud suspicion: the insurer questions whether the loss happened as described

When you receive a denial, request it in writing with the specific policy language cited. Compare that language to your actual policy. If the denial looks improper, start the appeal process with a written appeal to the insurer's claims department. If the appeal fails, a complaint with the state insurance commissioner is the next move.

Total loss disagreement

When repair cost approaches or exceeds the vehicle's actual cash value (ACV, what the car is worth at the time of loss), the insurer may declare a total loss. Car owners often disagree with either the total loss determination or the ACV number.

If the ACV seems low:

- Research comparable vehicles in your local market (same year, make, model, mileage, condition) to establish a realistic market value

- Provide the insurer with those comparable listings as documentation

- Request the insurer's valuation report to understand exactly how ACV was calculated

- Negotiate with supporting evidence, documented improvements, new tires, recent maintenance records

In borderline cases where you want to keep the vehicle, some states allow you to accept a reduced settlement and retain it. Expect a salvage title in those cases.

Rental car coverage issues

Many collision claims include rental car reimbursement while the vehicle is in the shop. Disputes come up when:

- Coverage is capped: policies typically limit both the daily rate and total rental duration

- Shop delays extend the rental period: if delays are the shop's fault, the insurer may stop paying after the originally estimated repair window

- Coverage simply doesn't exist: rental coverage is often an add-on purchased separately; not all policies include it

Confirm your rental coverage limits before repairs start. If the repair runs long for reasons outside your control, parts delays, supplement negotiations, document the reasons and request accommodation from the insurer in writing.

Key Takeaways

Filing an auto body insurance claim involves more decisions than most people expect. The process runs from the immediate moments after a collision through repair completion, and understanding each step produces better outcomes.

The most important things to carry forward:

- Run the math before filing: compare repair cost, deductible, and likely premium impact before committing

- Document the scene thoroughly: photos, contact information, and a police report build a strong claim foundation

- You get to choose your shop: any licensed repair facility, regardless of what the insurer suggests

- Supplements are normal: estimate gaps are standard; the supplement process is how they get resolved

- State your OEM preference in writing: state laws and policy language may back you up

- Disputes have a path: supplement, appeal, adjuster re-inspection, state commissioner complaint

You're not without recourse. Knowing the process, documenting thoroughly, and understanding your consumer rights are the three most effective tools you have.

For additional guidance, see the full collision repair guide or find collision repair shops in your area to compare estimates and talk through your claim.

Frequently Asked Questions

How do I file an insurance claim for auto body repair?

Contact your insurance company promptly after the collision with your policy number, date and location of loss, contact information for all parties, and damage photos. The insurer assigns a claim number and adjuster. Select a repair shop, get a written estimate, and work with the shop and insurer to approve the repair scope before work begins.

Can my insurance company force me to use a specific body shop?

No. In nearly every state, insurers are prohibited from requiring the use of a specific repair facility as a condition of claim payment. Car owners have the legal right to choose any licensed body shop. Insurers may suggest preferred shops, but that suggestion can't be made a requirement.

What if the insurance estimate is lower than the shop estimate?

This is common and expected. The shop documents the additional damage and submits a supplement to the insurer, a routine part of the auto body insurance claim process. If the insurer disputes the supplement, the shop provides photos, written documentation, and OEM procedure references to support the request.

Does filing a collision claim raise my insurance rates?

Filing an at-fault collision claim typically increases premiums at renewal, the national average increase is roughly 40 to 50%, though it varies by carrier and state. Not-at-fault claims have a smaller rate impact. Some insurers offer accident forgiveness. Ask the insurer to estimate the premium impact before filing.

Should I pay out of pocket instead of filing a claim?

Paying out of pocket makes sense when repair costs are close to or below the deductible, when recent claim history raises rate risk, or when the damage is minor and cosmetic. For larger repairs significantly above the deductible, filing is usually the right financial choice. Factor in potential premium increases before deciding.

What's a supplement in collision repair insurance?

A supplement is an updated estimate submitted by the repair shop when additional damage is discovered during teardown that was not visible in the original assessment. Supplements are a routine part of the insurance auto body repair process, they reflect hidden damage that only becomes visible once the vehicle is disassembled.

Insurance disclaimer: Insurance processes, coverage terms, consumer rights, and claim handling procedures vary by state, policy, and insurer. The information in this guide is for general educational purposes only and does not constitute legal or insurance advice. Car owners should review their specific policy documents and consult with their insurance carrier or a licensed insurance professional for guidance specific to their situation. State insurance department resources are available through the National Association of Insurance Commissioners.