About 1 in 5 auto body claims ends in a payment dispute. If your insurer won't cover the full repair, here's exactly how to push back and get what you're owed.

Why Insurance Companies Deny or Underpay Repairs

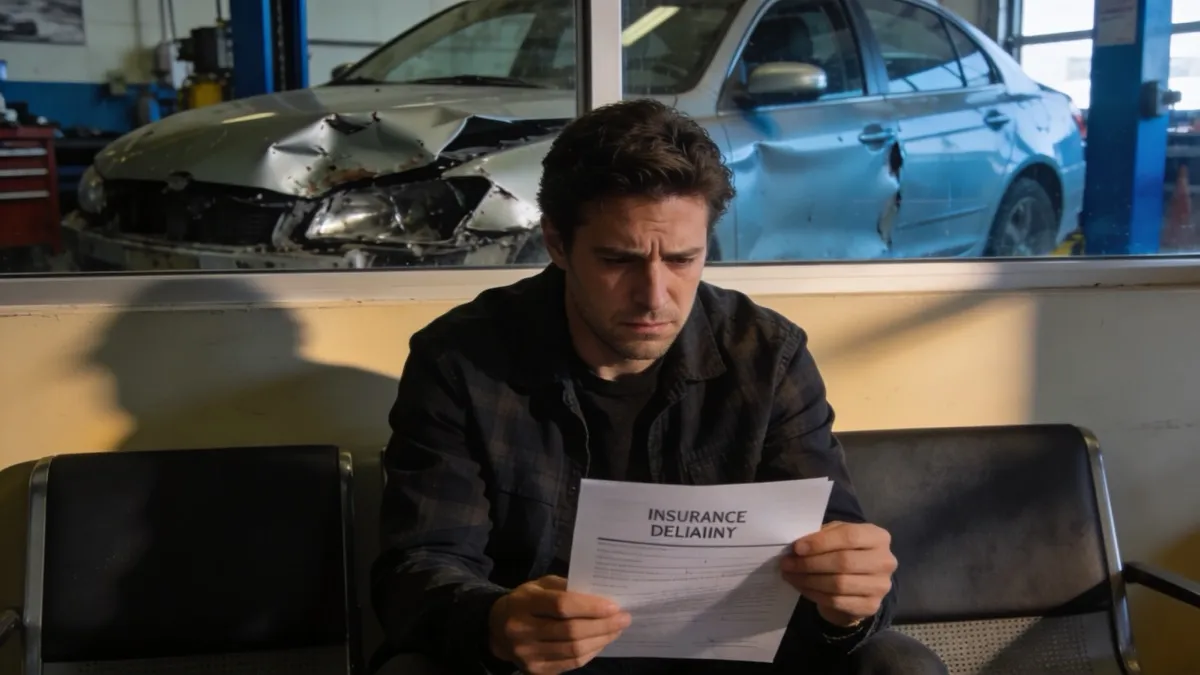

You filed your claim, got an estimate, and now the insurance company says they won't cover the full repair. This happens more often than most people realize, roughly 1 in 5 auto body claims ends in a dispute over repair costs.

Insurance adjusters work within strict cost guidelines. Their job is to settle claims for as little as possible while still meeting legal obligations. That doesn't mean they're right. It means you need to know how to push back.

Common Reasons for Denied or Reduced Payments

- Pre-existing damage. The adjuster says some of the damage was there before the accident. They'll point to rust, old scratches, or unrelated dents to cut the payout.

- Aftermarket parts substitution. Your estimate calls for OEM parts, but the insurer only approves cheaper aftermarket alternatives. The price gap on a single fender can be $200–400.

- Labor rate disputes. The insurer's "prevailing rate" for your area might be $52 per hour while local shops charge $65–75. That gap adds up fast on a 20-hour repair.

- Betterment charges. If worn tires or an old battery gets replaced during the repair, the insurer may deduct for the "improvement" to your vehicle.

- Total loss declaration. Instead of paying for repairs, the insurer declares your car a total loss when repair costs approach 70–80% of the vehicle's value.

What to Do When Your Claim Is Denied

Don't accept the first answer. Insurance denials are often a starting point for negotiation, not a final decision.

Get a Second Estimate

Take your car to an independent body shop, one that's not part of the insurer's direct repair program. Ask for a detailed, line-by-line estimate. Independent shops have no incentive to lowball the repair cost, and their estimate gives you real build on.

Request the Denial in Writing

Ask your adjuster to put the denial reason in writing. This forces them to commit to a specific justification you can then challenge with evidence. Verbal denials are easy for insurers to reframe later.

File a Supplement

Body shops find hidden damage once they start disassembling the vehicle. A supplement is an additional estimate for damage that wasn't visible during the initial inspection. Supplements are standard, about 60% of collision repairs need at least one.

How to Escalate When the Insurer Won't Budge

If your adjuster refuses to pay a fair amount, you've got options beyond just accepting their offer.

Invoke the Appraisal Clause

Most auto policies include an appraisal clause. Each side hires an independent appraiser, and if they can't agree, a neutral umpire decides. This process typically costs $200–500 but can recover thousands on an underpaid claim.

File a Complaint with Your State Insurance Department

Every state has a Department of Insurance that handles consumer complaints. Filing a complaint creates a formal record and triggers an investigation. Insurers take these seriously because repeated complaints can lead to regulatory action.

Consult an Attorney

For claims where the dispute is $3,000 or more, a consultation with an insurance bad faith attorney may be worth it. Many offer free initial consultations. If the insurer acted in bad faith, ignoring evidence, delaying unreasonably, or misrepresenting your policy, you may be entitled to additional damages.

"Document everything. Save every email, photograph every piece of damage, and keep a log of every phone call with your adjuster."

How to Prevent Payment Disputes Before They Start

The best time to protect yourself is before you file the claim.

- Photograph your car regularly. Take dated photos every few months. This kills the "pre-existing damage" argument before it starts.

- Know your policy. Read your declarations page. Know whether you've an OEM parts endorsement, rental car coverage, and what your deductible actually is.

- Choose your own shop. You've the legal right in all 50 states to pick your own body shop. A shop that works for you, not the insurance company, will advocate for proper repairs.

- Don't sign a direction to pay without reviewing the invoice. This sends the repair check directly to the shop. Keep control of the payment so you can confirm the final work before releasing funds.